- Rising port stocks fail to pressure prices

- Traders hold cargoes amid futures arbitrage

Mysteel Global: Supply of imported iron ore cargoes to China has loosened further in recent months with growing carrier arrivals at Chinese ports, while market demand for the steelmaking ingredient is waning due to reduced hot metal production during the winter season by Chinese mills.

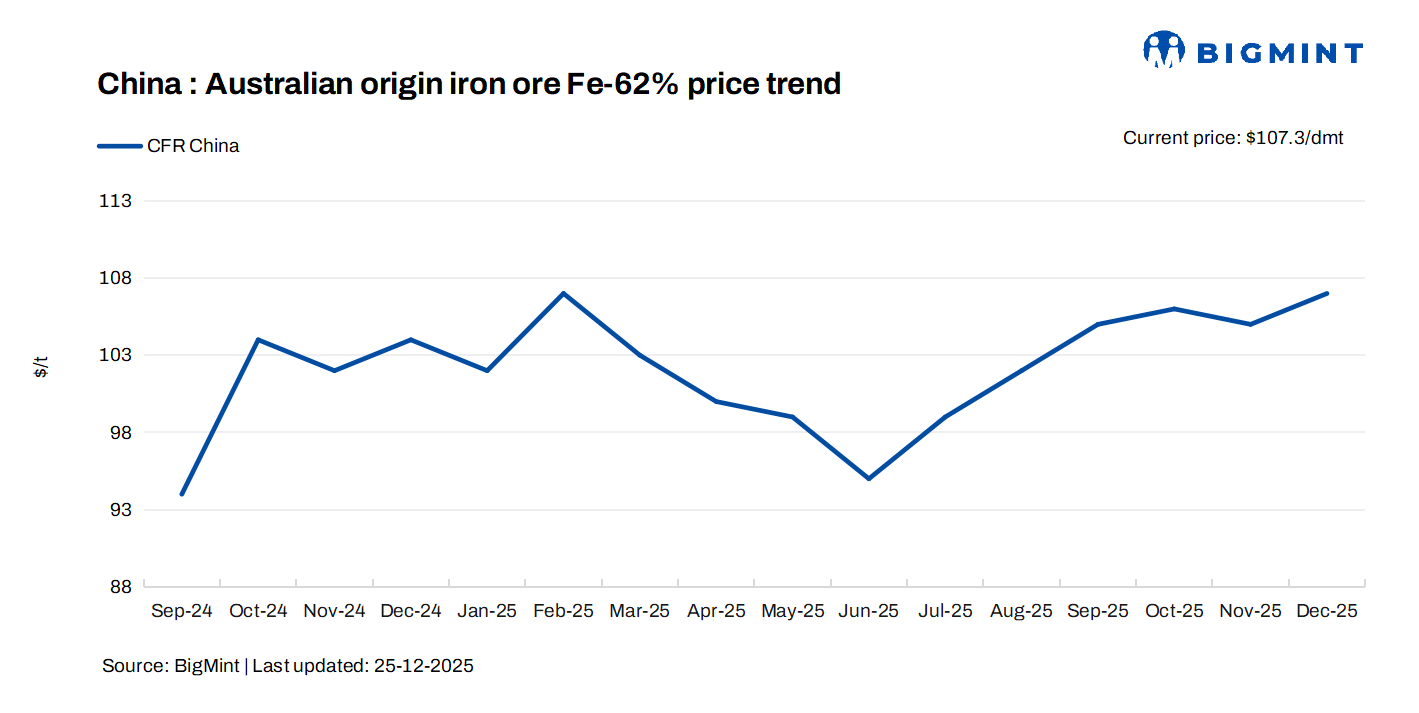

However, instead of tracking downward amid softening supply-demand fundamentals, imported iron ore prices in China have stayed surprisingly resilient recently. For example, Mysteel SEADEX 62% Australian Fines averaged $105.3/dmt so far in December, up from November’s average of $103.8/dmt. And the index has hovered above the $100/dmt threshold since late August.

The strength of imported iron ore prices has defied expectations of many market watchers, who had forecasted the prices to fall below $100/dmt in the second half of this year with a widening gap between underlying supply and demand.

They were right about the supply glut, though. China’s port stocks of iron ore have already risen to multi-year highs, with stockpiles at China’s 45 ports under Mysteel’s monitoring topping 155.1 million tonnes by December 18, the highest level since April 2022.

However, imported iron ore prices have held firm under the pressure of high port stocks, and this seemingly contradictory outcome mainly stems from the commodity’s strong financial attributes and a unified market expectation for seasonal inventory restocking by steel mills, according to Mysteel’s latest report.

First and foremost, iron ore is widely traded as a financial asset for arbitrage, as it is stable for long-term storage and it usually costs little for traders to hold at ports. Ports in North China typically offer free storage periods of as long as 90 days, Mysteel Global learns.

Consequently, when faced with temporary price drops, traders are in no rush to sell, as they also profit by selling near-month contracts and buying forward ones, taking advantage of a persistent “backwardation” in the futures market. This behavior prevents supply from flooding the spot market, underpinning prices of near-month iron ore contracts, the report argues.

Another critical support for iron ore prices, the report points out, is a wide market anticipation that domestic steel mills will build up their raw material inventories ahead of the Chinese New Year (CNY) holiday, which falls in late February next year. This pre-holiday restocking is a common practice of integrated steel mills to secure sufficient feedstocks for their smooth production during the long CNY holiday.

Notably, current inventories of imported iron ore held by Chinese steelmakers are significantly lower compared with previous years. For example, total stockpiles of the material held by the 247 blast-furnace mills under Mysteel’s tracking stood at 87.2 million tonnes as of December 18, lower by a marked 8.9% on year and marking the lowest level for this period during the past five years.

Although Chinese steel mills are increasingly inclined to maintain low inventory levels under financial strains, there is still considerable room for them to build up their ore stocks before the CNY holiday, the report said. Total inventories of imported iron ore held by the 247 mills sampled are expected to reach some 105 million tonnes by the start of the holiday, it estimates.

The anticipated demand boost from steel mills’ winter restocking has strengthened the bargaining power of traders, who now control sales volumes and wait for better prices. This has fortified a solid price floor for iron ore, the report notes.

In a nutshell, the recent strength of iron ore prices is a direct outcome of its dual identity as both a physical commodity and a financial instrument. Weak fundamentals have been offset by traders’ patience in holding stocks and positive prospects of demand recovery.

To realign iron ore prices with the underlying supply-demand balance, a sharp decline in real iron ore demand will be necessary, which means mills will have to cut their hot metal output more aggressively, the report suggests.

Also, if tougher port rules are rolled out to shorten free storage periods to 30 days for miners and traders, as the rumors have arisen recently, the costs of hoarding iron ore at ports will rise, which may dampen speculative interest for traders and weaken the support for iron ore prices, the report adds.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply