- Inventory caution limits fresh scrap bookings

- Currency weakness adds pressure on imports

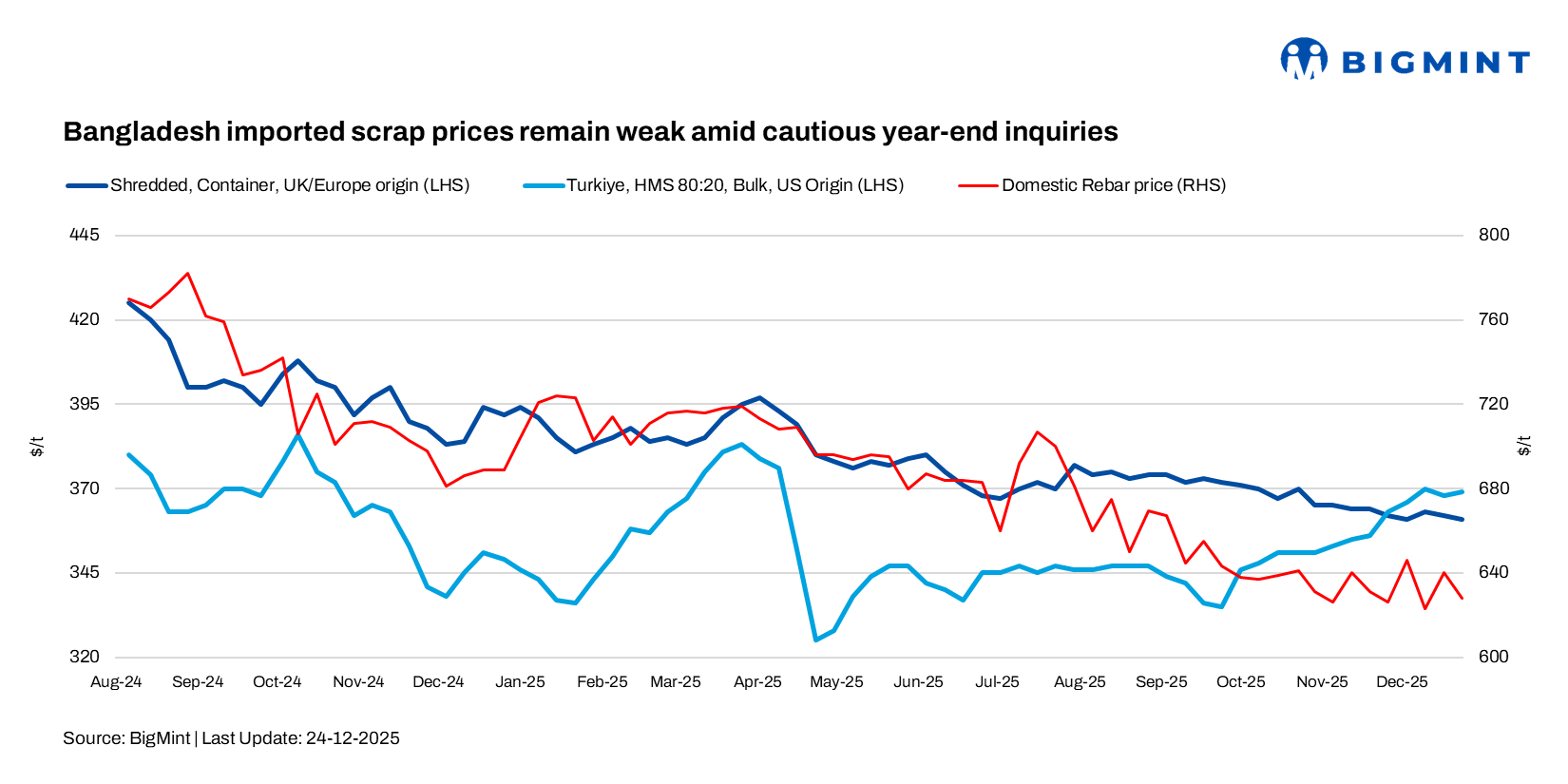

Bangladesh’s imported scrap market remained sluggish in the week ended 24 December, weighed down by year-end seasonality and weak mill buying. Market conditions were further strained by political uncertainty ahead of elections and local unrest, which led to the temporary shutdown of several Dhaka-based mills, dampening overall steel and scrap demand.

As per market participants, steel scrap sentiment remains weak amid falling rebar prices and subdued local demand. An Australian-origin HMS 80:20 cargo was concluded at $335/t CFR Chattogram for 1,000 t. Meanwhile, offers for shredded scrap stood at $360-362/t CFR from Australia, while PNS offers from Singapore and Hong Kong were quoted at $360-366/t CFR.

BigMint’s weekly assessments

- European-origin HMS (80:20) held at $341/t inched down by $1/t w-o-w

- European-origin containerised shredded inching down by $1/t w-o-w to $361/t.

- Japanese-origin H2 bulk dropped by $2/t w-o-w to $340/t.

- US-origin HMS (80:20) bulk increased by $4/t w-o-w to $356/t.

As per a bulk scrap trader, bulk offers from the US remain rare, with last heard levels at $365-370/t CFR, though without bids. Meanwhile, Japanese H2 scrap was quoted at $342-345/t CFR, with workable levels indicated closer to $335-340/t CFR.

Domestic market

Bangladesh’s steel industry faced one of its most challenging years in CY25, hit by weak construction activity, high energy costs, elevated interest rates, currency depreciation, and tight banking liquidity. While these pressures affected the sector broadly, outcomes diverged sharply.

One of the major Chattogram-based mills, however, stayed profitable on the back of scale, cost efficiency, and a stronger balance sheet, whereas another mill from the same region slipped into losses for the first time since listing, underscoring structural differences in business models.

Billet prices were assessed at BDT 63,000-64,000/t ($515-523/t), while rebar traded at BDT 72,000-77,000/t ($589-630/t). Local melting and ship scrap prices softened to BDT 45,000-48,000/t ($368-393/t) amid cautious furnace operations.

Ship recycling market

Recyclers in Chattogram remained under pressure this week as market conditions deteriorated sharply. The taka weakened to around BDT 122.30 following a firmer US dollar, while local steel plate prices fell by about $12/t in five days to nearly $485/t, down from over $600/t less than 45 days ago.

Higher US tariffs, currency weakness, falling plate prices, and limited availability of suitable vessels have disrupted trading activity. Additional pressure came from yard upgrades, infrastructure work, and firm freight rates. Despite progress on HKC compliance, the sector has contracted quietly this year, with active yards declining from around 35 to 22.

Outlook

Bangladesh’s scrap and steel markets are expected to stay weak in the near term as political uncertainty, mill shutdowns, and tight liquidity continue to weigh on demand. Buying interest is unlikely to improve meaningfully until election-related disruptions subside and construction activity and mill operations begin to normalise after year-end.

Leave a Reply