- Price gains driven by strong LME copper futures

- North India sentiment weak due to environmental restrictions

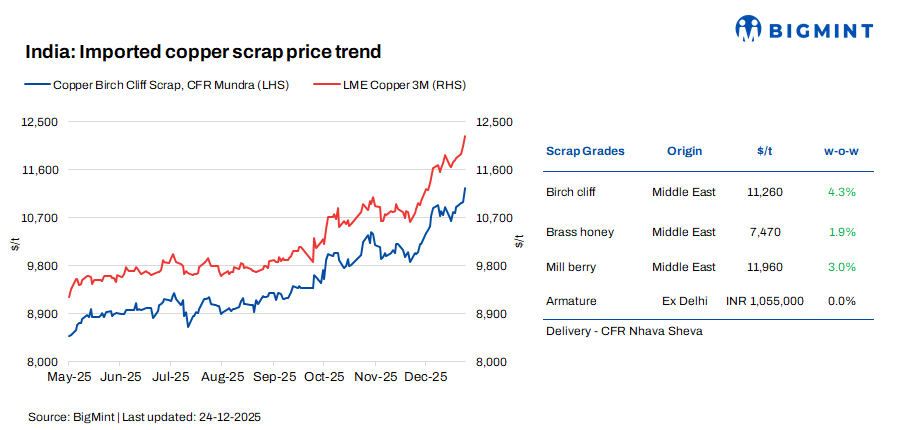

Imported copper scrap prices in India moved higher w-o-w on 24 December, supported by a strong rise in benchmark copper prices on the London Metal Exchange (LME) futures. Domestic copper scrap prices firmed in line with the strong LME uptrend, but restocking appetite stayed muted, with buyers limiting purchases to immediate requirements during the year-end holiday period.

LME price trend

LME copper prices crossed the $12,000/t recently, touching a fresh record in the final trading days of 2025. The three-month LME copper contract rose 1% to trade at $12,055/t, compared with $11,925/t in the previous session. Prices are now up around 36% so far this year, extending a strong upward trend.

Price assessments

According to BigMint’s assessment, Birch/Cliff was assessed at $11,260/tonne (t), up by $470/t w-o-w, while US motors mix stood at $1,370/t, up by $30/t w-o-w (both CFR Mundra).

Market scenario

In the domestic scrap market, prices were supported by surging copper prices on the LME, which are up over 35% YTD and which held above the crucial threshold of $12,000/t on Wednesday, with domestic copper scrap prices rising by up to 4% w-o-w. However, trading activity largely remained confined to immediate requirements, with many participants operating in holiday mode during the Christmas and New Year week.

A trader said, “Market sentiment in north India remains cautious, with trading and processing activity in Delhi still impacted by ongoing environmental restrictions. Several aluminium and copper plants are running at low utilisation levels, while some units remain temporarily shut as regulatory checks continue. Capacity is gradually shifting away from Delhi, with new copper CCR units reportedly being set up in Rajasthan.”

Another seller noted, “Buyers continue to restrict procurement to need-based volumes. Inventory levels remain tight, spot buying dominates, and any meaningful improvement in activity is expected to be gradual rather than immediate.”

In the domestic market, payment delays of around 10-12 days kept sellers cautious, further limiting traded volumes.

Imported copper scrap prices remained firm, tracking elevated LME levels, but higher overseas offers were largely unworkable for Indian buyers due to wide bid-offer gaps. Downstream demand, particularly from cable, wire rod and smaller fabricators, has yet to fully adjust to these higher benchmarks, resulting in selective buying and deferred procurement. Market participants added that any correction on the LME would quickly translate into softer domestic bids, highlighting that current price support is externally driven and vulnerable to shifts in global sentiment rather than underpinned by local consumption strength.

Additional updates

As per market reports, China’s copper scrap imports rose to around 2.1 mnt during Jan-Nov 2025, up by about 4-5% y-o-y, supported by tight copper concentrate availability and a growing reliance on secondary raw materials.

Import volumes remained firm despite elevated prices, with Europe and the US continuing as key supplying regions. However, availability from these origins has tightened, as copper scrap increasingly assumes strategic importance globally amid constrained primary feedstock supply.

Outlook

Market activity is expected to slow further in the near term as western suppliers enter the holiday period from the second half of today, curbing fresh offers from the US and Europe. This is likely to keep overall trade volumes thin.

In contrast, offers from the Middle East and Far East are expected to remain relatively more workable, which could support selective buying interest from Indian consumers, even as broader market sentiment stays cautious.

Leave a Reply