- Higher output revisions in China, Brazil and the US widen surplus

- Weak mill consumption in India, Turkiye deepens pressure on prices

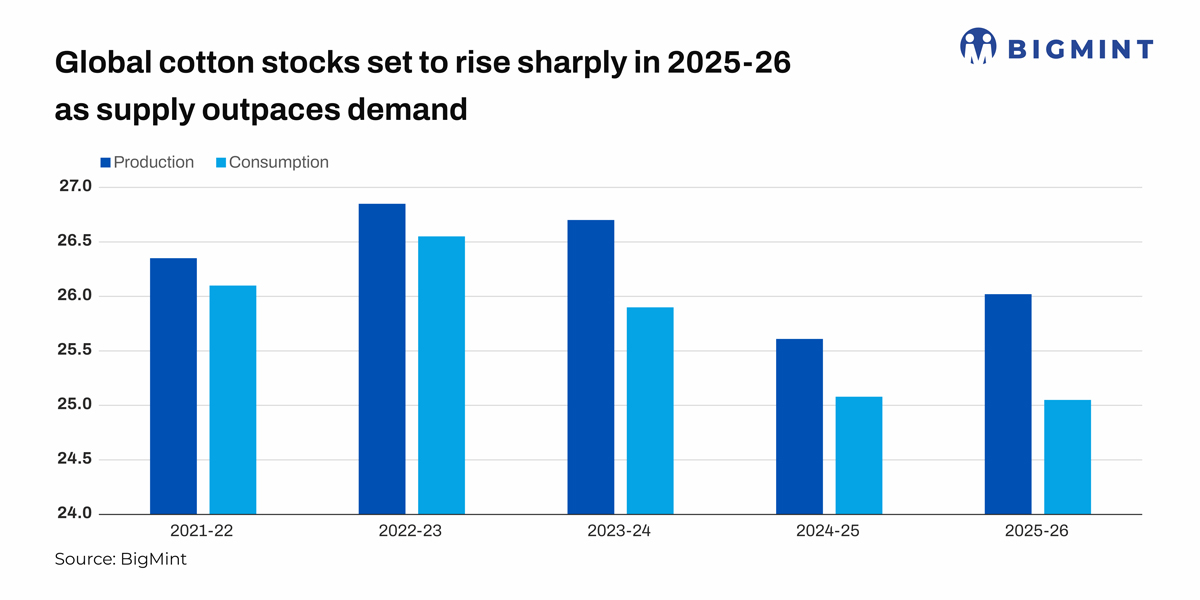

Cotlook’s latest December update signals a clear deterioration in the global cotton balance for the 2025-26 season, with world production revised sharply higher and consumption trimmed, resulting in a much larger addition to ending stocks. According to Cotlook, global raw cotton output for 2025-26 has been raised by 410,000 tonnes (t) m-o-m, while world consumption has been reduced by 34,000 t. As a result, the projected production-consumption surplus has widened to 970,000 t, almost double the 526,000-t surplus estimated in late November.

The upward revision on the supply side is driven mainly by higher crop estimates in China (+280,000 t), Brazil (+117,000 t), and the United States (+43,000 t). These gains more than offset a downward revision for Turkiye, where production has been cut by 30,000 t. World cotton production for 2025-26 is now pegged at 26.02 million tonnes (mnt), compared with 25.61 mnt estimated earlier. On the demand side, Cotlook has lowered global mill use to 25.05 mnt, reflecting weaker spinning activity in key consuming countries despite a modest upward revision for China.

For ginners, the data confirms that supply pressure is intensifying at a global level. Higher output from Brazil and the US adds to exportable availability, while China’s larger crop reduces its near-term import requirement. India’s production estimate remains unchanged at 5.10 mnt, but consumption has been cut sharply by 127,000 t to 5.23 mnt highlighting subdued yarn demand and cautious buying by spinning millers. Turkiye’s mill use has also been revised down by 67,000 t, reinforcing signs of stress in higher-cost textile hubs.

From a spinning millers’ perspective, the widening global surplus suggests continued ease in raw cotton availability through the 2025-26 season. Lower consumption growth relative to supply implies limited upside for international benchmarks such as the Cotlook A Index, particularly in the absence of a strong recovery in downstream textile demand. For Indian spinning millers, this global softness may continue to justify higher reliance on imports if domestic prices remain elevated due to MSP dynamics and procurement policies.

Outlook

Looking ahead, the sharp increase in projected ending stocks points to a demand-constrained market rather than a supply shock. Unless there is a sustained revival in global yarn and fabric demand—especially from apparel markets in the US and Europe—cotton prices are likely to remain range-bound with a bearish bias. Brokers should expect export competition to intensify among major origins, while ginners may face slower liquidation and tighter margins as buyers remain price-sensitive. Overall, Cotlook’s December numbers reinforce the narrative of structural oversupply and weak consumption defining the global cotton market.

Leave a Reply