- Australia, US lead recovery; Indonesian and Atlantic cargoes slip

- Weak Pacific and Atlantic freight slows fixing

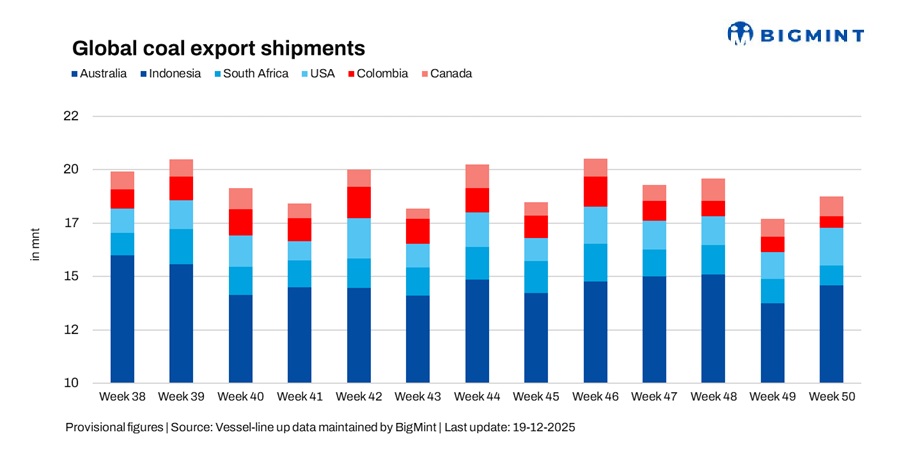

Global seaborne coal exports increased 5.6% w-o-w to 18.36 million tonnes (mnt) in the week ended 12 December, up from 17.39 mnt in the previous week, according to BigMint’s vessel line-up data. The recovery was primarily driven by a sharp rebound in Australian shipments and stronger US exports, which more than offset continued declines from Indonesia, South Africa, and Colombia. While overall volumes improved, weaker freight sentiment and cautious buying behaviour limited broader export momentum, keeping the market uneven across regions.

The w-o-w rise reflected improved cargo availability and higher loadings from Australia, alongside a notable pickup in US shipments, while softer demand and operational disruptions pressured exports from several Atlantic suppliers. Indonesia also saw a meaningful pullback as Pacific demand weakened, highlighting the growing influence of freight and buyer sentiment on weekly trade flows.

Country-wise trends

Australia’s coal exports rebound sharply

Australia’s coal exports rose sharply by 32.9% w-o-w to 7.85 mnt in the week ended 12 December, rebounding from 5.91 mnt in the previous week. The recovery was driven by higher loadings across major east coast ports, with Newcastle shipping 3.33 mnt, followed by Gladstone at 1.49 mnt and DBCT at 1.43 mnt, supported by smooth port operations and improved cargo availability after a quieter prior week.

On the demand side, shipment momentum remained measured as Indian and Northeast Asian buyers continued to procure selectively amid weak downstream demand and softer freight sentiment. Japan and China were the key importers, taking 2.69 mnt and 2.15 mnt, respectively, while Glencore led shipments with 1.03 mnt, followed by BHP at 0.55 mnt and Yancoal at 0.51 mnt. Looking ahead, better weather and fewer rail shutdowns in early 2026 should support smoother coal flows to Newcastle and help exports recover from past disruptions, though seasonally weaker Northeast Asian demand and softer prices may limit the upside.

Indonesian shipments ease on weaker Pacific demand

Indonesia’s coal exports declined 13.6% w-o-w to 6.61 mnt from 7.65 mnt in the previous week, driven by weaker enquiries from key buyers, particularly India and China, alongside fewer prompt fixtures in a softer Pacific freight environment. Tabneo led loadings with 1.29 mnt, followed by Bunati at 0.88 mnt and Samarinda at 0.80 mnt.

China and India remained the main destinations, importing 2.48 mnt and 1.44 mnt, respectively. Despite smooth port operations and adequate cargo availability, subdued downstream demand capped export volumes, highlighting how softer Pacific buying interest and weaker freight sentiment can quickly weigh on shipments even when operational conditions are supportive. Looking ahead, Indonesia is still expected to see strong growth in coal use this decade, as rising power demand and energy security needs outweigh near-term transition efforts, with coal remaining a key baseload fuel while renewable capacity scales up gradually.

South Africa exports decline amid demand softness and RBCT disruption

South Africa’s coal exports dropped 23.5% w-o-w to 0.87 mnt in the week ended 12 December, down from 1.14 mnt in the previous week, pressured by subdued buying interest from India and other destinations, alongside operational disruptions at Richards Bay Coal Terminal following wind-related damage and a force majeure declaration.

While the outage is expected to be temporary, the combination of weaker demand and uncertainty around loadings constrained export activity during the week, highlighting the market’s low tolerance for disruptions. At the same time, South Africa has recently increased coal exports to Israel after Colombia imposed a ban in August, making it Israel’s top coal supplier, although Israel’s plan to phase out coal by 2027 may limit the longer-term impact of this shift.

US coal shipments rise on improved cargo flow

US coal exports surged 41.8% w-o-w to 1.66 mnt from 1.17 mnt in the previous week, marking one of the strongest weekly performances among major exporters. The rebound was driven by improved cargo flows and stronger winter-related demand, supporting higher shipments to Europe and India. Baltimore led loadings with 0.56 mnt, followed by Norfolk at 0.39 mnt and Mobile at 0.35 mnt.

Despite the sharp rise, buying interest remained selective, and US exporters continued to face stiff competition from alternative suppliers. The increase appears largely seasonal and demand-led rather than structural, with future volumes still dependent on the durability of winter demand across key importing regions.

Colombia loadings weaken further

Colombia’s coal exports fell sharply by 35.2% w-o-w to 0.46 mnt from 0.71 mnt in the previous week, reflecting a combination of lower cargo availability and subdued demand from Europe, where buyers continued to draw down inventories cautiously. Loadings were concentrated at Barranquilla with 0.15 mnt and Puerto Nuevo at 0.13 mnt, while Prodeco Group and Cesar Coal emerged as the main shippers, exporting 0.19 mnt and 0.15 mnt, respectively.

The decline highlights persistent weakness in Atlantic basin demand and Colombia’s limited ability to offset softer European buying with alternative markets in the near term. Export flexibility has also been reduced following Colombia’s ban on coal shipments to Israel, which removed a key destination and has further constrained overall shipment volumes, adding to the downside pressure on weekly exports.

Canada exports edge higher

Canada’s coal exports saw a 12.3% week-on-week increase, rising to 0.91 million tonnes (mnt) from 0.81 mnt in the previous week. Roberts Bank handled the bulk of the shipments at 0.53 mnt, followed by Prince Rupert at 0.22 mnt, while Elk Valley Resources contributed 0.16 mnt. The modest uptick was supported by steady port operations and slightly improved demand from Northeast Asian buyers.

Despite the increase, overall shipment volumes remained below recent highs, indicating that Asian importers continue to exercise caution amid ample global coal supply and volatile coal prices. Japan emerged as the top importer, taking in 0.32 mnt during the week, highlighting the country’s continued reliance on Canadian thermal coal for its energy needs. Meanwhile, Canadian authorities approved the merger of Anglo American and Teck Resources to form Anglo Teck, a move expected to create a top global producer of copper, zinc, iron ore, and coking coal.

Dry bulk coal freights to India softens

Coal freight rates to India softened across both the Pacific and Atlantic basins during the week, reflecting weaker cargo demand and rising vessel availability. Earlier support from prompt tonnage tightness faded as coal enquiries slowed and open vessel lists lengthened, prompting owners to lower rate ideas in order to secure employment.

In the Atlantic, subdued export activity and a lack of fresh fixtures reinforced the downtrend, while the RBCT disruption had limited immediate impact due to already muted demand. Softer bunker prices provided little cost support, further adding downward pressure on rates. These conditions encouraged cautious fixing behaviour, particularly on Indonesian and South African routes, and tempered shipment growth despite higher Australian exports.

Outlook

Global coal exports are expected to remain mixed through the remainder of December, with regional variations influencing trade flows. Australia is likely to sustain relatively higher shipments if cargo availability remains strong, while Indonesian and Atlantic exports may stay under pressure amid weak demand and soft freight sentiment. Temporary disruptions, such as the RBCT outage, could tighten supply briefly, but meaningful upside in exports will depend on a pickup in buying interest from India and Northeast Asia.

Overall, trade flows are expected to remain sensitive to freight dynamics, vessel availability, and short-term shifts in regional demand. With global coal demand peaking this year and declining toward 2030, shipments and rates will be shaped by market fundamentals, seasonal buying, and competition from alternative energy.

Leave a Reply