- Refined lead production increased by 1.7%

- Refined zinc market in surplus of 76,000 t

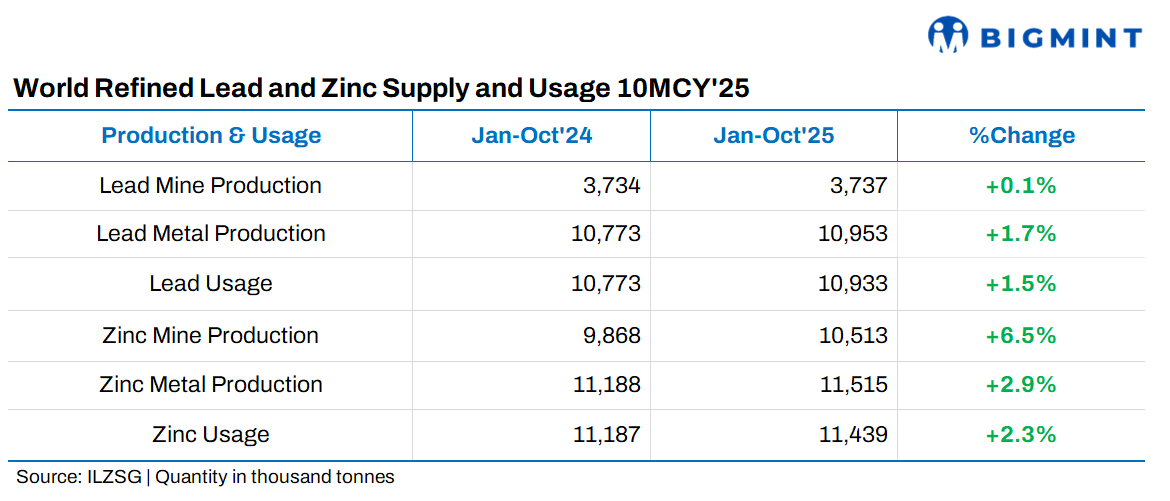

Preliminary data released by the International Lead and Zinc Study Group (ILZSG) for the first ten months of 2025 indicate that global lead and zinc markets remained in surplus, even as reported inventories declined, highlighting a relatively balanced but evolving supply-demand landscape.

Lead: Balanced market limits upside

According to provisional data, the global refined lead market recorded a modest surplus of 20,000 t during January-October 2025. Despite this surplus, reported inventories declined by 22,000 t, indicating relatively balanced underlying fundamentals.

Global lead mine production was broadly stable, registering a marginal increase of 0.1%. Higher output in China, India, Peru, Turkiye, and Europe was largely offset by declines in Australia, Kazakhstan, and the United States.

Refined lead metal production increased by 1.7%, supported by higher output in Canada, China, India, South Korea, Mexico, Sweden, and Brazil, where new secondary lead capacities have recently been commissioned. These gains were partially countered by reduced production in Japan, Kazakhstan, and the United Kingdom.

On the demand side, refined lead usage rose by 1.5%, driven primarily by increased consumption in Brazil, Taiwan (China), the United States, and Vietnam. European demand also strengthened, led by France, Germany, Poland, and the UK, although this was partly offset by lower usage in Italy and Spain. In contrast, lead consumption in India and Mexico declined compared to the same period in 2024.

China’s imports of lead contained in concentrates increased by 8.5% to 981,000 t, while net imports of refined lead metal fell sharply to 24,000 t, down 95,000 t year-on-year.

Zinc: strong mine growth, but inventory draw supports prices

The global refined zinc market was in a surplus of 76,000 t during the first ten months of 2025. Even so, reported zinc inventories decreased significantly by 129,000 t, reflecting strong offtake and supply chain adjustments.

World zinc mine production rose by a robust 6.5%, led by higher output in Australia, China, Iran, Mexico, Peru, South Africa, and the Democratic Republic of Congo, following the commissioning of the Kipushi mine. European production also increased, supported by the Vares operation in Bosnia and Herzegovina, the Ozernoye mine in Russia, and the restart of the Tara mine in Ireland.

Global refined zinc metal production increased by 2.9%, largely due to an 8.4% rise in Chinese output. However, production outside China declined by 2.2%, reflecting closures and disruptions in Brazil, Kazakhstan, Mexico, Japan, and South Korea.

Refined zinc usage grew by 2.2% globally, with notable increases in China, India, Saudi Arabia, Thailand, and Europe, partially offset by reduced demand in South Korea.

China’s imports of zinc contained in concentrates surged by 36.3% to 2,102,000 t, while net imports of refined zinc metal fell to 253,000 t, a decline of 113,000 t compared with the same period last year.

Leave a Reply