- Imported diecast scrap rises $30/t w-o-w on tight supply

- Slower offtake drags down zinc oxide prices in north India

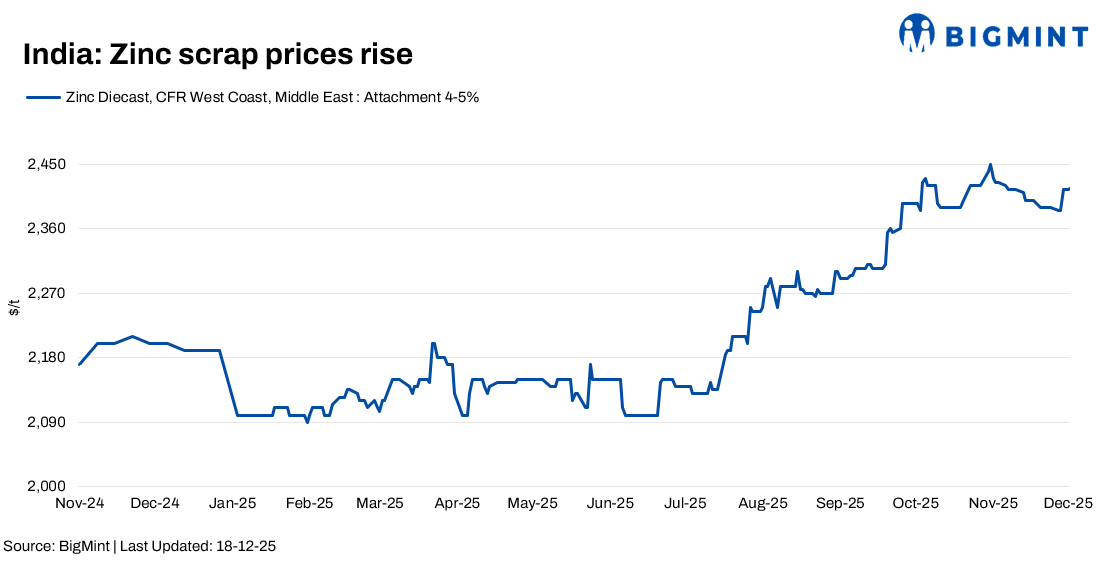

The Indian zinc scrap market recorded mixed trends during the week ending 18 November. Tight spot supply led to a slight uptick in prices of imported diecast scrap, though gains in other grades were limited by softer global zinc prices and subdued domestic demand.

BigMint assessed zinc diecast scrap (Middle East origin) at $2,450/t CFR west coast India, up $30/t w-o-w, supported by limited spot availability despite a correction in London Metal Exchange (LME) futures. Three-month LME zinc was at $3,050/t, down $82/t from last week’s $3,132/t, prompting cautious sentiment among importers and alloy makers.

Zinc oxide (99% Zn) prices declined by INR 4,000/t w-o-w to INR 239,000/t ex-Delhi due to slower offtake from the ceramics, rubber, and fertiliser sectors, according to market participants.

In the domestic market, zinc dross prices softened amid sluggish buying interest. Dross was assessed at INR 249,100/t ex-Delhi, down INR 7,900/t w-o-w, while Mumbai prices stood at INR 246,000/t ex-works. Alloy producers cited adequate inventories and weak downstream demand.

Additionally, big-sized zinc scrap (Tukdi, 97% Zn) was offered at INR 258,000/t ex-Delhi, down by a minor INR 1,000/t w-o-w, while mid-sized Tukdi (97-98% Zn) similarly edged down to INR 248,000/t. Largely, prices remained stable.

Global zinc industry update

Globally, sentiment was influenced by major strategic developments in the US zinc industry. Korea Zinc announced a $6.6 billion investment to establish its first US operations in Tennessee, highlighting a growing focus on critical minerals and supply chain diversification. Additionally, Nyrstar USA, a Tennessee-based zinc mining and smelting operation, is in discussions to sell its assets to Korea Zinc, potentially giving it control of the only primary zinc smelter in the US, subject to regulatory approvals.

Outlook

Zinc scrap prices are expected to remain at these levels for the rest of the month and in the first half of January, with downside risks linked to softer LME zinc prices and weak domestic offtake. However, import scrap values may find support from limited availability and steady replacement costs. Market participants will monitor LME price movements, currency trends, and post-year-end demand recovery, while global consolidation developments may shape medium-term sentiment.

Leave a Reply