- Crude steel output falls to 2-year low

- Auto production rises but PV sales fall sharply

- Manufacturing PMI contracts for 8th straight month

Morning Brief: Chinese macroeconomic indicators continued to sound alarm bells for its steel industry in November 2025. Fixed asset investment growth fell by 2.6% in January-November, a sharper downtrend than the -1.7% recorded in January-October. November also marks the third consecutive month in which the growth rate remained negative, with pandemic-struck 2020 being the last year recording such a contraction.

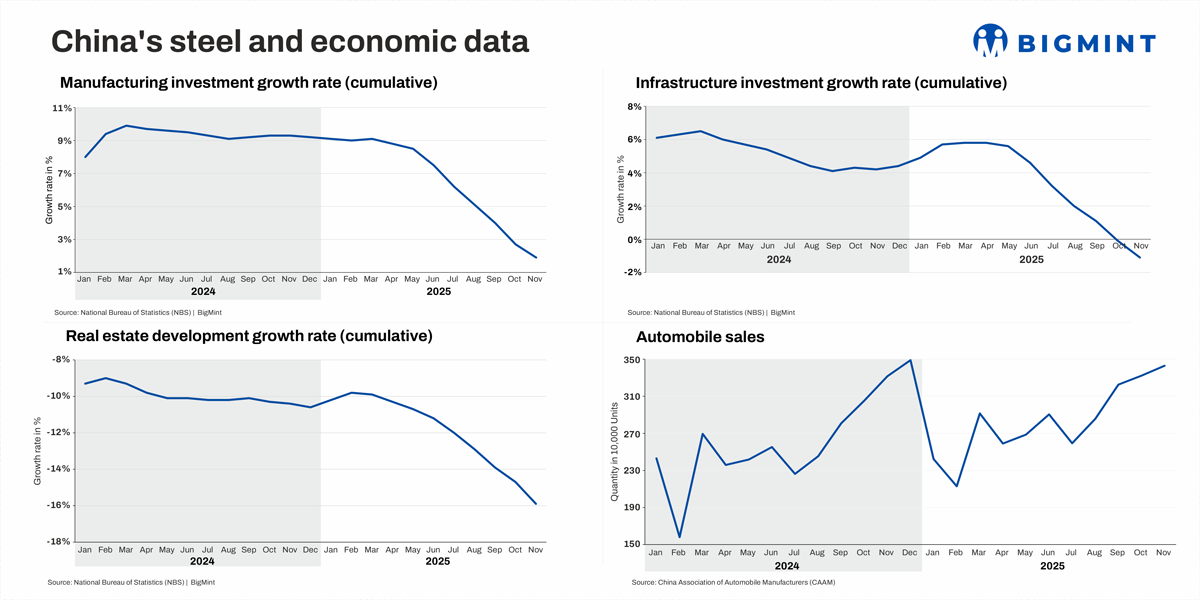

Parallelly, manufacturing investment growth shrank for the eighth month running. Meanwhile, infrastructure investment slid for the seventh month, with real estate development growth down for the ninth.

All these signal a persistent contraction in steel demand in CY’25, that is likely to extend into the next year as well. Worldsteel has already projected a 2% drop in Chinese steel demand in 2025, which is set to moderate to a 1% dip in 2026 on an expected recovery in the housing market.

Highlights of industry trends in Nov’25

Crude steel production drops on weak profitability

China’s crude steel output fell 10.9% y-o-y and 3% m-o-m to a 23-month low of 69.87 million tonnes (mnt) in November, with shrinking profitability, cost pressures from raw material prices, air pollution control measures, and lacklustre steel demand during winter prompting output cuts or maintenance shutdowns. According to Mysteel, only 35% of major mills made a profit during end-November compared to 45% a month ago.

Steel exports rise as domestic demand remains subdued

Chinese steel exports increased by 2% m-o-m and 7.5% y-o-y to 9.98 mnt, as steelmakers continued to direct shipments overseas due to weak domestic demand and elevated inventories. Exporters continued to offer material at aggressively low prices. For example, hot-rolled coil (HRC) export offers fell by $14/tonne (t, 3%) m-o-m to a monthly average of 464/t FOB Rizhao in October.

Iron ore imports climb up y-o-y despite drop in crude steel output

China’s iron ore imports climbed up by 8.5% y-o-y while declining by 0.7% m-o-m to 110.54 mnt. The slight m-o-m fall could be attributed to thinning steel mill margins, which also prompted output cuts. However, the y-o-y increase marks a divergence from the sustained decline in crude steel production, caused most likely as mills restocked material ahead of winter. Benchmark prices have moved in a narrow range since September, with the monthly averages remaining in the 104-106/t range.

Coal production, imports fall y-o-y

China’s coal production edged down by 0.5% y-o-y but increased by 5% m-o-m to 426.79 mnt in November, with the latter trend possibly due to easing production restrictions.

Moreover, coal imports stood at 44.05 mnt, down 19.9% y-o-y while rising by 5.6% m-o-m. The y-o-y decline in imports likely stems from a narrowing price gap between domestic and imported material. Additionally, thermal electricity output fell 4.2% y-o-y in November, even as hydroelectric generation increased 17.1%.

Automobile production continues to grow but passenger car sales tumble

Automobile production edged higher by 5.1% m-o-m and 2.8% y-o-y to 3.532 million units, according to data from the China Association of Automobile Manufacturers (CAAM). This is the first time monthly volumes have crossed the 3.5 million mark. However, the pace of growth seems to have slowed, given that January-November recorded an uptick of 11.9% compared to a softer 13.2% in January-October.

However, while automobile manufacturers’ sales increased by 3.2% m-o-m and 3.4% y-o-y to 3.429 million units across categories, according to the China Passenger Car Association (CPCA), sales of passenger vehicles fell 8.5% y-o-y to 2.24 million units, the sharpest decline in 10 months.

This has caused concern, given that China’s vehicle sales generally remain strong during the last two months of the year. The CPCA also likened the slide to conditions seen in 2008, during the US economic recession.

It is assumed that consumer demand may have cooled in November, especially with the phasing out of trade-in subsidies and cautious sentiment ahead of the new year.

Meanwhile, new energy vehicles (NEV) remained automakers’ key growth engine in November. Both production and sales surged by around 20% y-o-y to 1.88 million units and 1.823 million units, respectively. The market penetration of NEVs has deepened significantly, evidenced by NEV sales accounting for 53.2% of new automobile sales, according to an SMM report.

Manufacturing investment slides, PMI contracts for 8th month

Manufacturing investment growth slowed to 1.9% in January-November from 2.7% in January-October. Compared to the 9.1% logged in January-March, November’s growth rate marks a steep fall.

It seems that China has been banking on exports this year to meet growth targets, with domestic demand remaining subdued. The government’s anti-involution policy is also expected to capped production in certain segments, while trade tensions and geopolitical conflicts added further pressure.

China’s retail sales growth fell to 1.3% y-o-y from 2.9% in October, the weakest since December 2022.

Rail, ships, and aerospace; auto manufacturing sectors; industrial robots; and semiconductors feature among the industries witnessing strong growth.

Meanwhile, China’s manufacturing purchasing managers’ index (PMI) remained in contraction territory for the eighth consecutive month, though it inched up to 49.2.

Construction activity remains in slow lane

Infrastructure investment growth declined by 1.1% y-o-y in January-November, while real estate development contracted by a sharp 15.9%. Both remained at multi-year lows, suggesting sluggish construction momentum and offering little support to steel consumption. New home prices also fell by 0.39% m-o-m, indicating weak consumer interest.

Outlook

China’s property crisis, in its fifth year now, remains a drag on overall consumption and economic strength. At the Central Economic Work Conference, the government revealed its 2026 strategy for stabilising the property sector, emphasising efforts to limit new supply, reduce inventories, and shift to more high-quality projects. This may bring about an improvement in steel consumption, but a definite timeline has not been specified, so uncertainty remains.

Additionally , steel export controls by China, seen as a way to rein in outflows and block tax evasion, are likely to have limited impact, given that domestic demand remains weak and supply is excessive.

Moreover, while crude steel output is expected to continue declining in December, it is likely to continue outpacing the decline in demand, leading to weak market conditions continuing.

Leave a Reply