- Mid-CV coal grades fetch moderate premiums

- Mid-CV grades account for over 90% of allocations

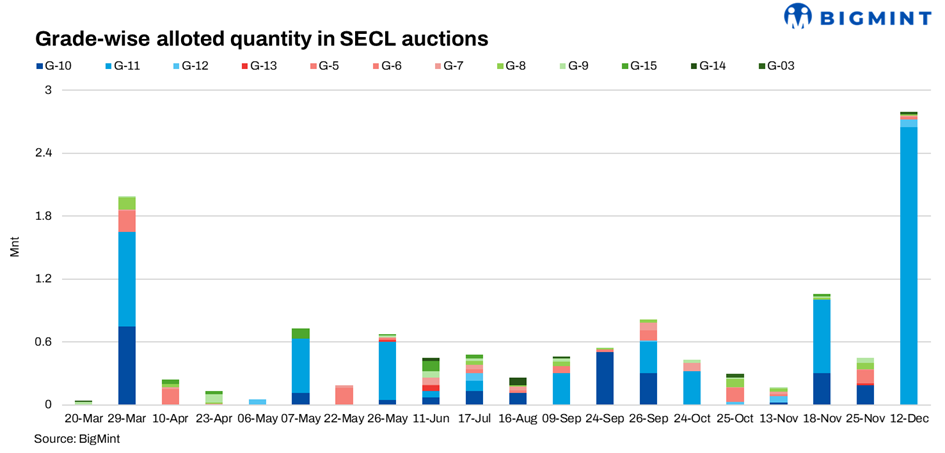

SECL’s auction on 12 December 2025 saw strong participation, with 2.80 mnt allocated out of 3.22 mnt offered across G5-G9 and G11-G12 grades, reflecting broad-based demand despite recent price corrections. Reinforcing the ongoing shift among Indian consumers toward domestic coal amid elevated imported coal prices and freight constraints. While final bid prices moderated compared with earlier auctions, premium percentages remained healthy, indicating that demand for reliable domestic supply stayed intact despite broader price corrections.

Over the past two weeks, market sentiment has turned increasingly supportive of domestic coal. End-users that traditionally relied on imported South African and Indonesian coal have begun actively evaluating domestic alternatives, driven by better availability, predictable logistics, and a widening landed-cost gap versus imports.

Grade-wise outcome show clear demand skew

G11 dominated volumes, with 2.65 mnt clearing at an average INR 1,570/t, comfortably above the reserve of INR 1,418/t. Major open-cast sources–Gevra OC (1.0 mnt at INR 1,601/t), Dipka OC (0.60 mnt at INR 1,709/t) and Kusmunda OC (0.60 mnt at INR 1,472/t)–anchored supply, ensuring liquidity in the mid-CV segment. G12 saw 71,000 t cleared at INR 1,318/t, in line with reserve levels, suggesting balanced but non-aggressive bidding.

G6 cleared 25,000 t at INR 3,653/t, above the reserve of INR 3,305/t, while G4 achieved INR 4,119/t for 24,000 t, supported by underground-origin parcels such as Rani Atari UG (20,000 t at INR 4,145/t). G8 recorded a notable premium, with 15,000 t clearing at INR 3,030/t versus a reserve of INR 2,312/t, reflecting selective competition for quality parcels. G7 and G5 cleared smaller quantities largely at reserve-linked levels, indicating cautious participation in thinner segments.

Mid-CV G11 alone accounted for nearly 95% of total allocations, underlining its role as the backbone grade for power, aluminium, and large industrial consumers. Premiums in G11 stayed close to double digits despite falling spot prices elsewhere, signalling that buyers prioritised supply security over chasing lower bids. The standout was G8, which recorded the highest premium at over 30%, reflecting tight availability and selective competition for quality parcels. Higher-CV grades such as G6 and G4 continued to fetch stable premiums, though well below the extreme volatility seen in smaller-volume auctions earlier this month.

The dominance of Gevra, Dipka and Kusmunda ensured ample mid-CV supply, preventing runaway premiums even as demand stayed firm.

Buyer behaviour reflects cautious confidence

Large industrial consumers led procurement, with Bharat Aluminium Co. Ltd. emerging as the top buyer at 320,000 t (INR 1,418/t). Other active participants included Vedanta Limited (150,000 t at INR 1,478/t), ALPS Mining Services (150,000 t at INR 1,628/t), Rama Coal Washeries (100,000 t at INR 1,568/t) and Phil Steel & Power (96,000 t at INR 1,563/t). The spread of buyers and pricing suggests disciplined buying rather than aggressive chasing.

Buying patterns suggested measured restocking rather than aggressive inventory build-up, consistent with the cautious sentiment seen in the spot market over the last fortnight. Importantly, market participants noted that several end-users previously dependent on imported coal actively participated or tracked this auction, as imported alternatives remained uneconomical due to high seaborne prices, freight tightness, and recent supply disruptions at origins such as Richards Bay Coal Terminal.

Leave a Reply