- South African exports rise 4% amid increasing sponge iron output

- US thermal coal deliveries surge amid domestic pet coke shortage

- Competitive pricing, blending preferences boost imports from Russia

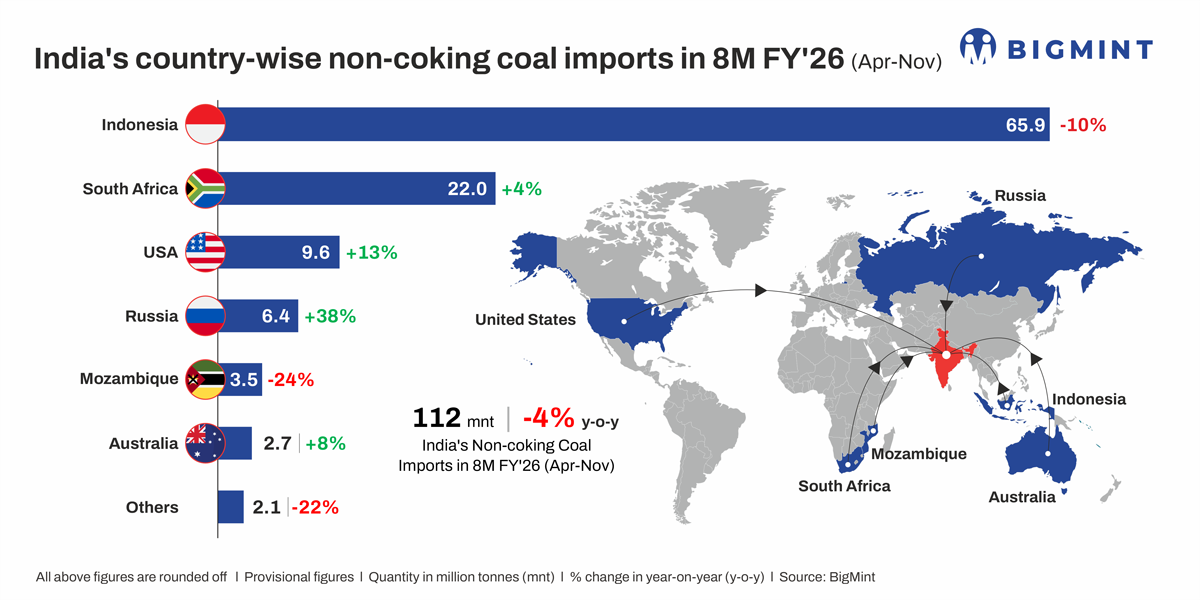

Morning Brief: India’s thermal coal imports fell by 4% y-o-y to 112 million tonnes (mnt) in April-November 2025 (8MFY’26) from 117 mnt in the year-ago period, as per data maintained by BigMint.

The decline can primarily be attributed to lower procurement of Indonesian non-coking coal (-10%), which is largely consumed by the power sector. The easy availability of domestic thermal coal at attractive prices has reduced the need for imports by power plants. The steady decline also aligns with the government’s drive to curtail India’s import dependency in the coal sector, as well as lift the usage of renewables.

Notably, the 4% decrease recorded in April-November is a slight moderation from the 6% drop in April-October. Non-coking coal imports climbed up by 12% m-o-m to 13.71 mnt in November, with a surge in inflows from Russia (+163% m-o-m at 1.10 mnt) and the US (+44% at 1.16 mnt).

Country-wise imports

Arrivals from Indonesia, the leading thermal coal exporter to India, fell by 9.6% y-o-y in April-November to 65.9 mnt.

South African exports, consumed primarily by sponge iron manufacturers, edged up by 4.1% y-o-y to 22 mnt.

Russian and US shipments to India surged by 37.8% y-o-y to 6.4 mnt and 13.1% to 9.7 mnt, respectively.

Factors influencing India’s thermal coal imports in Apr-Nov’25

Demand from thermal power sector moderates: India’s coal-fired power generation continued its downtrend in April-November. Output fell 5.5% y-o-y to 829 billion units, attributed to surging growth in alternative sources.

Hydropower generation increased by 13.3% to 147 billion units on the back of an above-normal monsoon, while renewable energy production jumped by 22.2% to 189 billion units, with the government fast-tracking capacity additions in the past years in alignment with decarbonisation goals.

India’s energy consumption also inched down by 0 .1% y-o-y to 1.147 trillion units due to an extended monsoon and cooler temperatures.

Additionally, elevated coal stocks at power plants kept import demand muted. Coal stocks at thermal coal plants were at 54 mnt on 30 November, up 34% y-o-y according to a report from Financial Express. Non-pithead power plants dependent on imported coal had 3.1 mnt of coal, 74% of the normative requirement of 4.2 mnt.

Sponge iron production rises 9%: India’s sponge iron production increased by 9% y-o-y to 39.23 mnt in April-November 2025, leading to steady demand for South African thermal coal, a key feedstock. Notably, CIL’s coal dispatches to sponge iron units fell by 51% during April-November 2025 to 4.92 mnt compared to 10.07 in the year-ago period.

This fall was caused by logistical constraints earlier in the year, including limited rake availability at SECL, and CIL’s policy obligation to prioritise power utilities during peak demand months. Consequently, South African thermal coal exports to India increased during the same period, though by a mild 4.1%.

Domestic pet coke supply tightens: US thermal coal imports in India increased 13.1% y-o-y due to a shortage of petroleum coke in the domestic market. Leading manufacturer Reliance Industries Limited has refrained from offering material to the merchant market since April 2025 due to internal consumption in its gasification units. Additionally, US thermal coal stands as a more cost-effective alternative to imported pet coke.

In November, imported pet coke offers averaged around $120/t CNF India, while Indian bids were at $110-111/t, leading to a persistent bid-offer gap of nearly $10/t. Meanwhile, portside US NAPP coal was available at Kandla/Tuna at INR 9,875/t, excluding GST, equivalent to about $102-103/t CFR in the week ending 28 November. Fresh offers of US NAPP coal were at $112-113/t CFR India, with bids at $108-109/t CFR.

Competitive pricing lures importers to Russian coal: In April-November, Russia overtook Mozambique to become the fourth-largest coal supplier to India. The significant rise in imports is attributed to aggressive pricing strategies, with Russian coal reportedly available at a significant discount due to sanctions by traditional importers. Russian coal’s higher calorific value and lower ash content also makes it a preferred option for blending in thermal power plants.

According to the International Energy Agency, the average discount on Russian high-CV coal at Vostochny was $21/t in 2025 against benchmark Australian high-CV prices. Newcastle FOB (6 000 kcal/kg) averaged $104/t in 2025, down 22% from 2024.

Outlook

Overall, India’s thermal coal imports are expected to continue declining in FY’26 despite brief spikes in certain months and for specific purposes. To illustrate, sponge iron units may continue sourcing imported coal due to specific quality requirements, as well as limited availability from CIL. Meanwhile, pet coke supply constraints may sustain US thermal coal demand.

However, rising coal production during the winter months is expected to curb imports from Indonesia and, thus, keep overall volumes in check.

In fact, considering ample domestic supply and robust production, the Indian government has given power plants the greenlight to export surplus thermal coal. Coal linkage holders, that is entities with long-term supply contracts, will be eligible to export up to 50% of their coal linkage quantity.

Additionally, with the approval of the CoalSETU policy, the government has permitted allocation of long-term coal linkages through auctions for any industrial purpose. Meanwhile, CIL opened the ninth tranche of its coal linkage auctions in December, and by 8 December, bidders had taken up about 40% of the offered volume, with premiums around 14% above notified prices.

Both are signals that coal supply will remain strong in the coming years and India’s import dependency is set to further decline.

Leave a Reply