- Higher Chinese ports inventory keeps buying interest low

- Discount are widen and hover at 20% for Fe57% fines

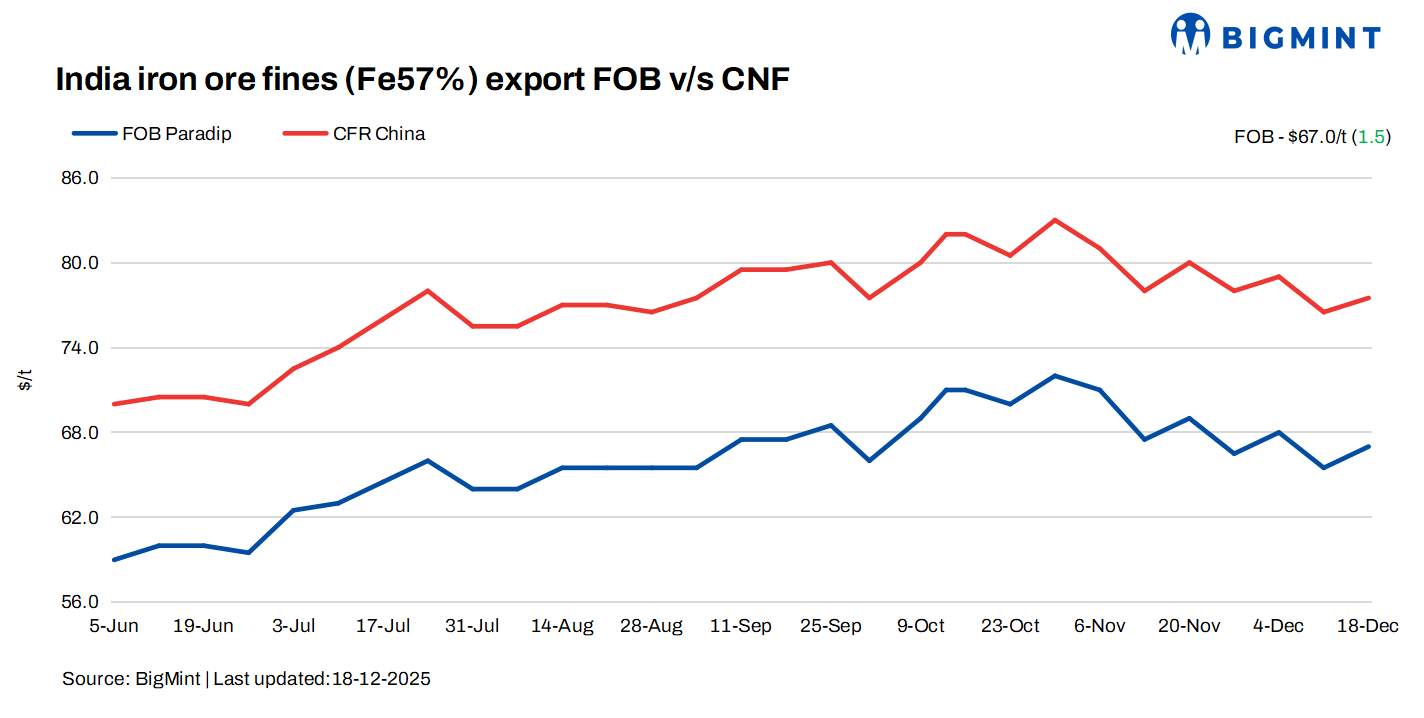

Indian iron ore fines export prices remained firm in the week ended 18 December, supported by stable to positive global iron ore prices in the seaborne market. Market participants noted that sellers continued to hold their offers, taking cues from the strength in international benchmarks and elevated domestic procurement costs.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices increased by $1.5/tonne (t) w-o-w to $67/t FOB east coast on Thursday. Meanwhile, the index stood at $77.5/t CFR China.

BigMint heard approximately 100,000 t of export deals during this publishing period, which were primarily concluded over the last weekend. The discount is now floating in the market at around 19-21% for the Fe 57% fines cargo, while exporters are still targeting 18%, which is not attracting buyers for fresh deals. While 56% Fe cargoes were reported to fetch discounts in the range of 22-23%.

Market scenario

However, despite firm pricing, export demand remained subdued. Sources informed that higher iron ore inventories at Chinese ports and the presence of some unsold low-grade Indian cargoes in China limited fresh buying interest. As a result, inquiries stayed tight, and no bulk export deals were concluded during the week, mainly due to a wide bid-offer gap in the seaborne market.

According to market participants, discounts for Indian low-grade fines were widened. “Buyers are bidding lower than our expectations, whereas our offers are firm as material sourcing from the domestic market is still costly,” a market participant told BigMint.

Some miners were even heard offering discounts of around 17% for single-mine cargoes in an attempt to attract buyers, but these offers also failed to translate into confirmed deals. An international trader said, “At these levels, sellers are not comfortable lowering prices further, while buyers are waiting for better discounts.”

On the demand side, a few international traders pointed out that January laycan demand from China remains weak. Pollution-related production restrictions on steel mills, coupled with comfortable portside inventories, have reduced immediate appetite for imported iron ore fines. As per reports, steel mills are largely relying on port stocks and their existing raw material inventories.

Market participants remain cautiously optimistic, expecting some improvement in sentiment in the near term. A few deals are reportedly under negotiation.

Chinese spot prices firm w-o-w: The benchmark iron ore fines index rose $1/t w-o-w to $107/t CFR China on 17 December. Pockets of restocking activity was recorded for February delivery cargoes, which helped support near-term fundamentals. Mid-grade fines remained in focus for buyers.

DCE iron ore futures rise w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the Jan 2026 contract closed at RMB 777/t ($110/t) on 18 December, rising by RMB 20/t ($3/t) w-o-w.

Rationale

- No (0) major deals for Fe 57% were recorded during this publishing window; not taken for price calculation. Therefore, T1 trade was given 50% weightage in the index calculation. A few deals were already factored into Monday’s assessment. For the detailed methodology, click here.

- BigMint received Twenty (20) indicative prices in the current publishing window, and sixteen (16) were considered for price calculation as T2 inputs and given 50% weightage.

Iron ore inventories at major Chinese ports were recorded at 145.5 mnt on 18 December, surging by 1.7 mnt w-o-w, as per data published by SteelHome.

Outlook

We expect raw material prices to fluctuate in a narrow band of $1-2/t over the course of this week.

Leave a Reply