- Production growth outpaces sales on capacity ramp-up

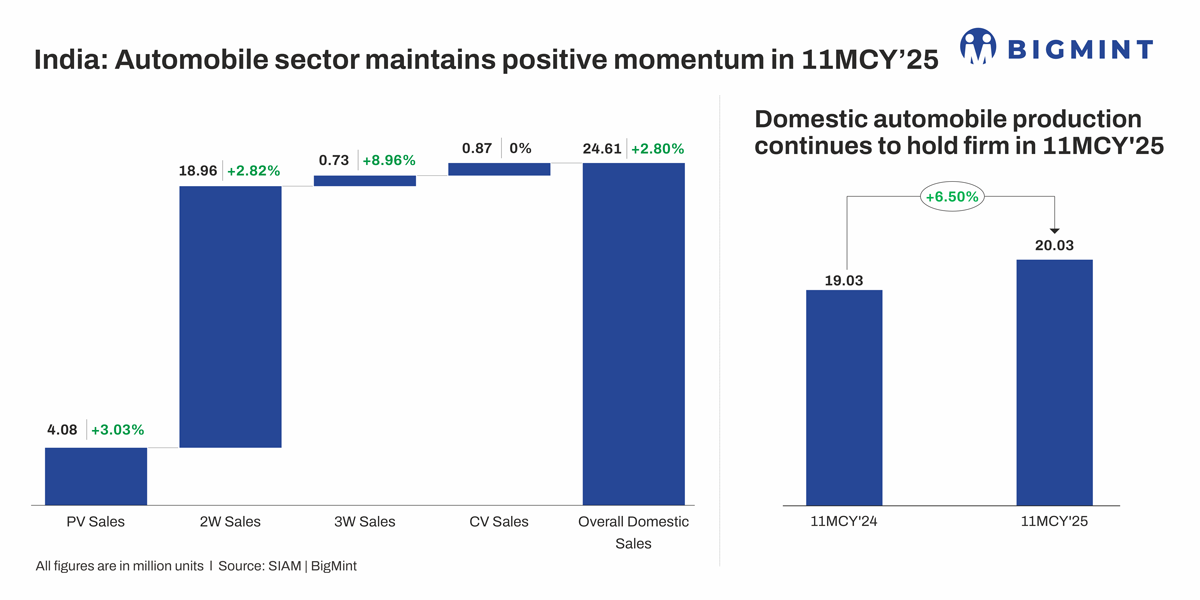

- Total production rises 6.5% y-o-y to 28.85 million units

India’s automobile sector recorded steady y-o-y growth in 11MCY’25 (January-November 2025) reaching 24.61 million units, reflecting an increase of 2.8% y-o-y from the previous year’s 23.94 million units, supported by higher OEM sales, rising production and resilient domestic demand, according to data from SIAM.

Passenger vehicle (PV) sales increased 3.03% y-o-y to 4.08 million units, while two-wheeler sales rose 2.82% to 18.96 million units. Three-wheeler volumes grew a robust 8.96% to 0.73 million units, though commercial vehicle (CV) sales remained flat at 0.87 million units. Meanwhile, total production climbed by 6.5% to 28.85 million units, highlighting healthy manufacturing activity.

Exports, domestic demand and policy support drive growth

The sector’s performance was underpinned by a mix of structural and cyclical drivers. Vehicle exports recorded double-digit growth, particularly in two-wheelers and passenger vehicles, as global OEMs increasingly leveraged India as a manufacturing hub. Domestically, demand remained resilient on the back of steady GDP growth, easing supply-chain constraints and sustained preference for utility vehicles, which now account for more than half of PV sales.

Rural demand recovery and stable financing conditions supported two-wheeler and three-wheeler volumes, while ongoing infrastructure spending helped stabilise CV demand despite flat y-o-y sales. On the supply side, OEMs ramped up output faster than sales, aided by capacity expansion under the government’s INR 25,938-crore Production-Linked Incentive (PLI) scheme and cumulative FDI inflows of nearly $29 billion into the auto sector.

Retail sales reinforce demand momentum

Retail trends further confirmed demand strength. As per FADA, passenger vehicle retail sales rose 7.88% y-o-y to 3.97 million units, while two-wheeler sales increased 7.03% to 18.89 million units in 11MCY’25. Three-wheelers and CVs posted growth of 5.36% and 6.52%, respectively, while tractor sales surged 11.39% to 0.88 million units, supported by favourable monsoon conditions and improved farm incomes. Overall retail vehicle sales expanded 7.16% y-o-y to 25.9 million units, reflecting sustained consumer demand.

Strong Nov dispatches lift near-term confidence

Momentum extended into November, with OEM dispatches to dealerships registering double-digit growth across key segments. Passenger vehicle wholesale dispatches rose by around 19% y-o-y to nearly 0.41 million units, while two-wheeler dispatches increased about 21% to 1.94 million units. Leading manufacturers, including Maruti Suzuki, reported record November volumes, driven by strong domestic demand, export growth and dealer inventory replenishment, reinforcing confidence in the sector’s near-term outlook.

Impact on aluminium ADC12 alloy market

The healthy performance of the automobile sector has continued to support India’s aluminium ADC12 alloy market, given its extensive use in automotive die-casting applications. Rising production across passenger vehicles, two-wheelers and commercial vehicles has sustained demand for lightweight aluminium components.

Despite typical year-end seasonality, ADC12 demand has remained resilient, keeping prices largely stable m-o-m. As per BigMint’s assessment, OEM-grade ADC12 ingot prices stood at INR 232,000/t in Delhi, INR 231,000/t in Pune and INR 230,000/t in Chennai (30-day payment terms). Softer domestic scrap prices have widened the scrap-to-alloy spread, improving margins for secondary alloy producers, particularly in southern India.

Outlook

India’s automobile sector is expected to maintain steady growth momentum, supported by strong export demand, improving rural consumption and continued policy-backed manufacturing expansion. While year-end maintenance shutdowns may lead to short-term moderation, demand is likely to rebound in early 2026. This outlook should keep automotive-linked aluminium demand, including ADC12 alloy consumption, firm, with prices expected to remain stable and gradually trend higher as production normalises.

Leave a Reply