- Domestic zinc prices slide on weak spot demand; import premiums stable

- HZL hikes list prices, market sentiment remains soft

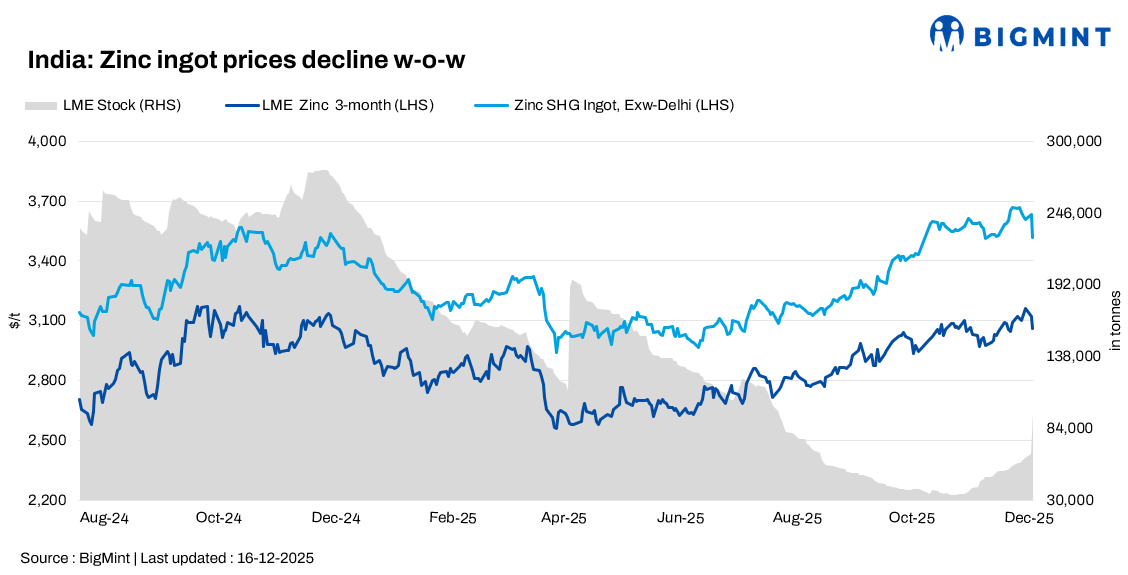

India’s zinc ingot (99.995%) prices declined by INR 10,000/t w-o-w to INR 320,000/t ex-Delhi, according to BigMint’s assessment. The fall was driven by subdued spot demand from downstream consumers and softer global benchmarks, which weighed on market sentiment despite limited availability of imported material.

On 15 December, Hindustan Zinc Limited (HZL) increased its zinc ingot prices by INR 3,400/t ($37/t) to INR 334,300/t ($3,685/t) ex-Chanderiya. However, the hike failed to lift spot prices, as buyers remained cautious and trade volumes stayed thin.

Traders indicated that Special High Grade (SHG) zinc ingots were offered at INR 312,000/t ex-Mumbai, down INR 10,000/t from the previous week, reflecting weak buying interest in western India. Australian-origin zinc continued to command a premium of $240/t over LME prices on a CFR Mundra Port basis, supported by limited import arrivals.

In north India, Australian-origin zinc ingots were offered at INR 327,000/t ex-Delhi, broadly stable week-on-week, as tight availability offset the broader bearish sentiment in the domestic market.

Global zinc futures snapshot

LME zinc futures weakened over the past week, pressured by easing risk appetite, softer base metal sentiment, and concerns over near-term demand. Market participants remained cautious amid mixed macroeconomic signals and steady warehouse stocks.

The LME 3-month zinc contract traded in the range of $3,060-3,160/t during the week, ending lower on a week-on-week basis. The cash-to-3M spread narrowed, indicating reduced tightness in the prompt market.

Indian coated steel prices edge up

As per latest assessment, GP coils (0.8 mm/CTL, 120 gsm, IS 277) were assessed at INR 60,600/t ex-Mumbai, up INR 900/t w-o-w, with offers at INR 60,000-61,000/t. Galvalume prices rose to INR 74,500/t, while PPGI increased to INR 69,300/t, supported by steady demand and firm input costs

Outlook

India’s zinc market is expected to remain under pressure in the near term due to weak spot demand and softer global cues, despite firm import premiums and constrained Australian-origin supplies. While HZL’s price hike may offer some downside protection, buyers are likely to stay on the sidelines, closely tracking LME movements, domestic offtake, and import arrivals before committing to fresh purchases

Leave a Reply