- Weak domestic demand weighs on steel production

- Elevated supply and competitive pricing boost exports

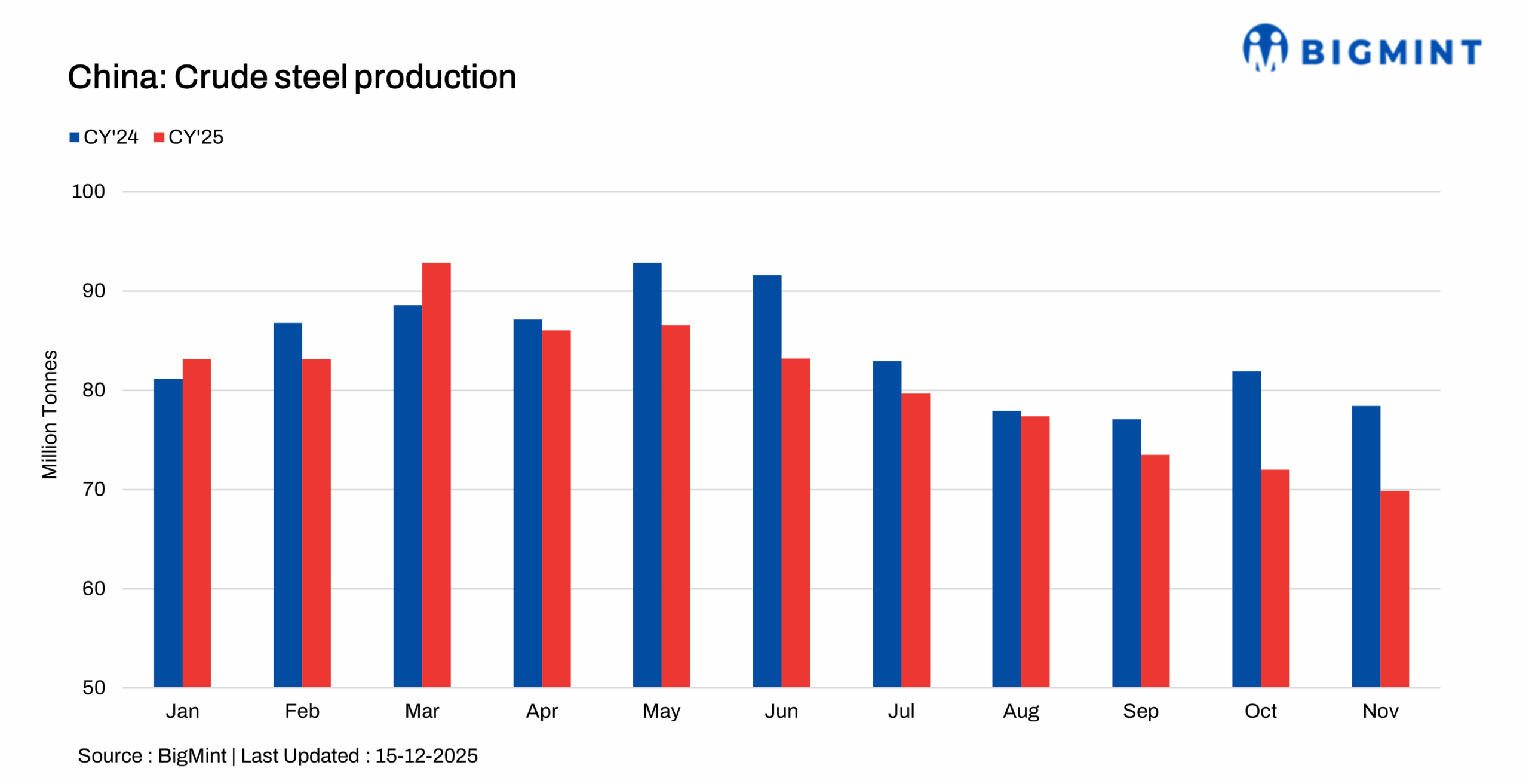

China’s crude steel production stood at 69.87 million tonnes (mnt) in November 2025, down by 10.9% y-o-y from 78.4 mnt in November 2024, according to data from the National Bureau of Statistics (NBS).

For the January-November period, total production reached 891.67 mnt, marking a decline of 4% decline from 926.35 mnt in the same period last year.

Factors affecting crude steel output:

Weak domestic demand: China’s domestic steel demand remained subdued, driven by prolonged weakness in the property sector, expectations of a seasonal slowdown, and limited policy support from the central government. Market sentiment remained cautious amid uncertainty over end-user demand, while high supply levels continued to weigh on prices.

Increase in steel exports: China’s steel exports rose 7.6% y-o-y in November to 9.98 mnt, up from 9.27 mnt a year earlier. Weak domestic demand prompted producers to divert more volumes overseas, to ease inventory pressure and sustain production rates.

This export push was further supported by China’s highly competitive pricing, with November HRC offers to the Middle East falling $19/t m-o-m to around $482/t CFR UAE, well below Indian offers of about $505/t CFR, thereby strengthening China’s export competitiveness and supporting higher shipment volumes.

Outlook

China’s crude steel production is expected to remain under pressure in December on persistently weak domestic demand which continues to weigh on apparent consumption and price sentiment. Elevated export volumes, supported by competitive pricing, may help ease inventory pressure and lend limited support to production levels. However, in the absence of a sustained recovery in domestic demand, overall crude steel output growth is likely to remain constrained.

Leave a Reply