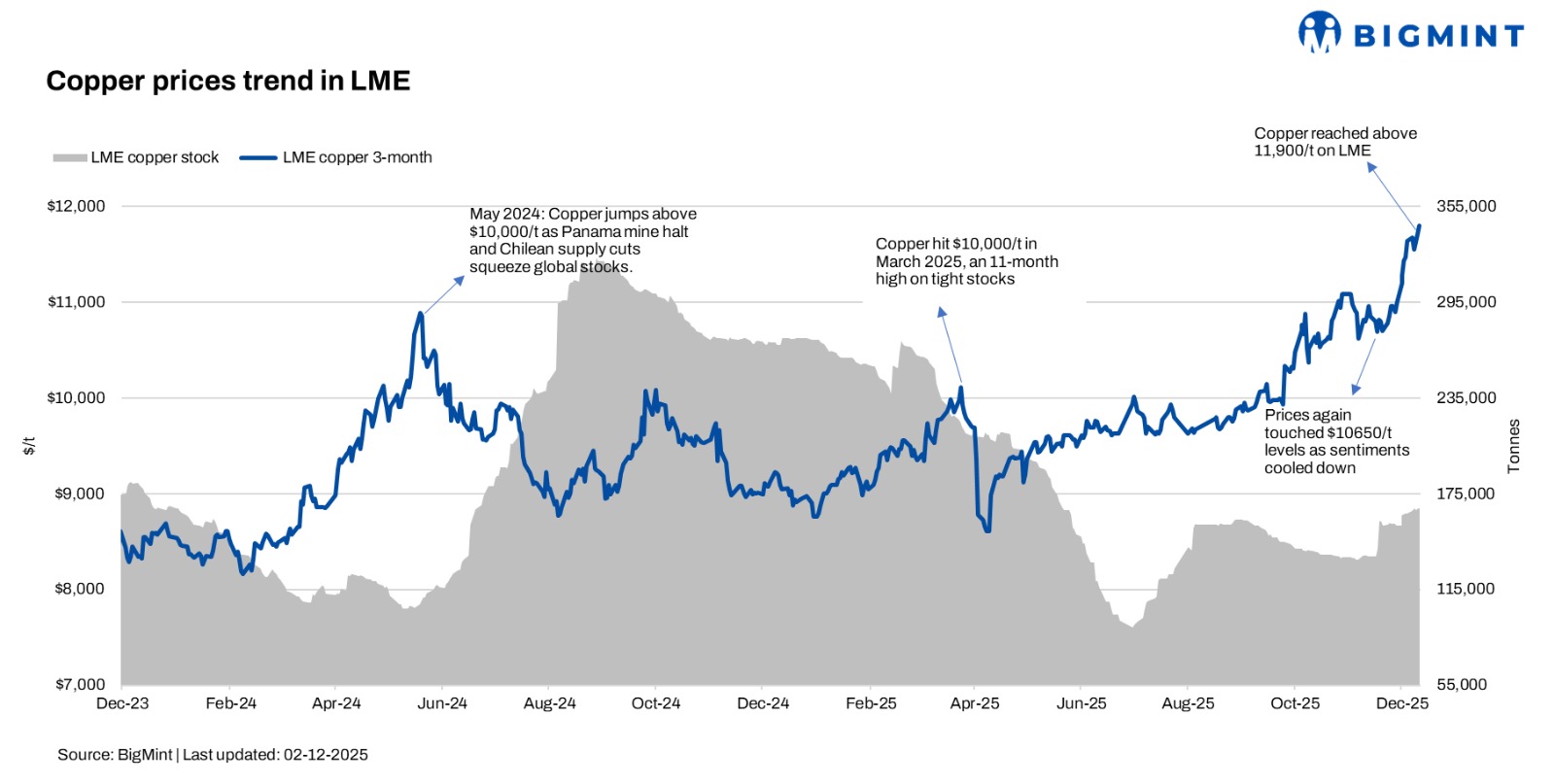

LME copper prices have remained broadly supported in the first half of December, slipping around 3% to $11,520/t on 12 December from the day before, much lower than the $11,850–11,900/t range seen earlier in the month, while still holding well above historical averages. Prices have inched closer to the psychologically important level of $12,000/t, touching a record high of $11,952/t during trading on Friday, a level that miners and procurement desks watch closely.

While the short-term correction appears notable, market participants view the move as a technical consolidation rather than a shift in fundamentals. The ability of copper prices to stabilise near elevated levels continues to reflect strong underlying support from tight supply conditions, low inventories and structurally robust demand expectations as the market heads into 2026.

Through 2025, copper prices climbed sharply on the back of persistent mine disruptions, tightening concentrate availability, and falling inventories across global exchanges. These factors continue to shape price direction, limiting downside risk even as physical trading activity slows due to holidays in the West. Traders note that selling pressure has remained muted, with participants increasingly reluctant to unwind long positions ahead of a potentially tighter year.

A key pillar of support remains the severely stressed concentrate market. Treatment and refining charges (TC/RCs) are hovering near multi-year lows, reflecting an acute shortage of mined feedstock. Several smelters are operating under margin pressure, while any further mine outages risk amplifying refined metal tightness. This structural squeeze has reinforced bullish sentiment in the futures market, keeping LME prices elevated.

Looking ahead, sentiment for 2026 remains broadly bullish. Major banks and trading houses forecast average LME copper prices in the $11,500–13,000/t range, with several projecting prices testing or sustaining levels above $12,000/t if supply challenges persist. Refined copper deficits of 250,000–330,000 t are widely expected next year, reflecting slow mine growth, delayed project ramp-ups, and limited scope for a recovery in concentrate availability.

In this context, the recent price move to $11,660/t is seen less as a short-term rally and more as confirmation of a structural repricing of copper. With TC/RCs unlikely to normalise in the near term, inventories at or near cycle lows, and demand from energy transition sectors accelerating, copper is increasingly viewed as entering a phase where elevated prices are necessary to balance the market.

As the year draws to a close, liquidity may thin due to holiday closures, but underlying fundamentals suggest that any price softness is likely to be temporary. The market appears set to enter 2026 with a tight supply backdrop, reinforcing expectations that copper will remain one of the strongest-performing base metals in the year ahead.

Leave a Reply