- Weak Chinese demand caps upside momentum

- Japanese premiums signal tightening supply outlook

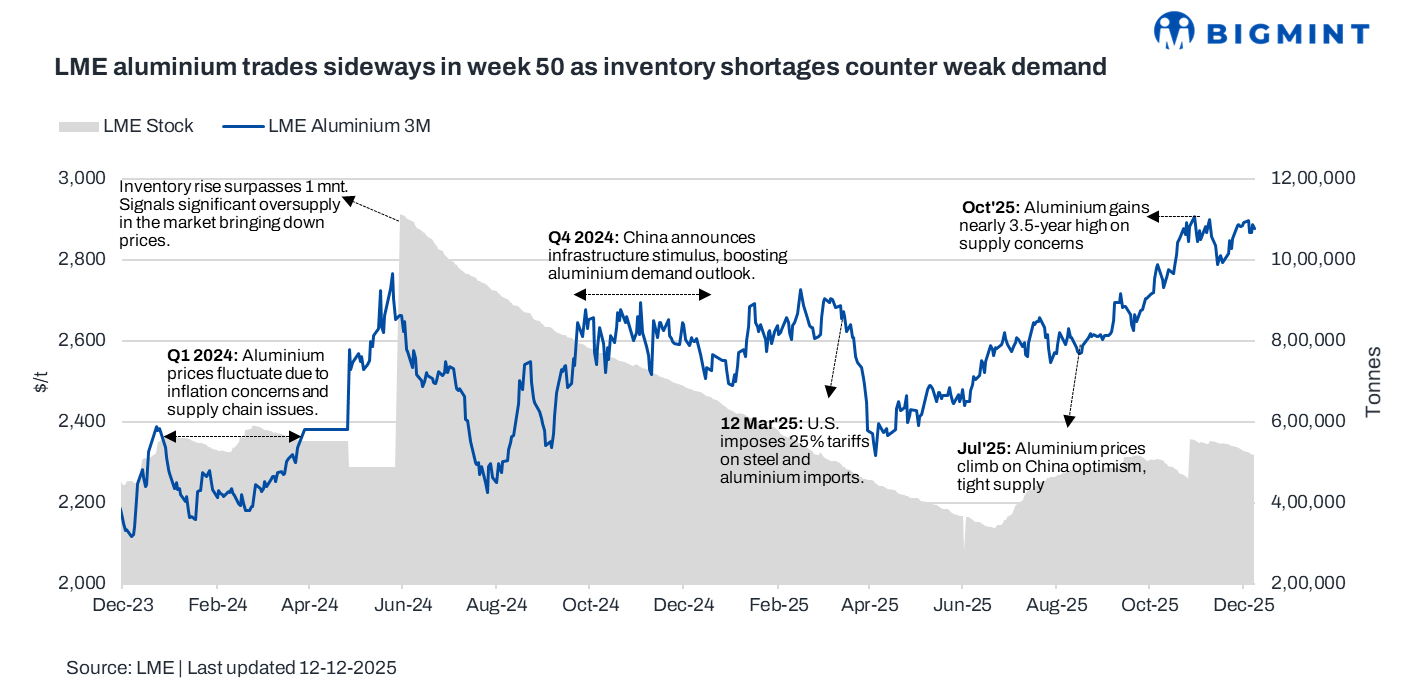

Aluminium prices on the London Metal Exchange (LME) remained largely rangebound week on week during the period ended 12 December. Prices were supported by declining exchange inventories and US Federal Reserve rate cuts, which improved overall market sentiment. However, persistent concerns over demand in China, the world’s largest metals consumer, continued to weigh on sentiment and capped further upside.

Pricing, inventory trends

LME aluminium prices averaged $2,880/tonne (t) in the week ended 12 December, marking a marginal $8/t or 0.3%% dip w-o-w from the previous week. The week began with higher prices at $2,897/t, which then fell to around $2,867/t mid-week. Prices closed at $2,876/t on 12 December.

Meanwhile, LME aluminium inventories witnessed outflows, with stocks down by 2.2% at 521,660 t against 533,280 t in the previous week.

Factors impacting prices

Aluminium prices remained rangebound during the week as supportive supply-side factors were largely offset by weak near-term demand signals. Prices did not see a sharp downside as supply concerns persisted, with LME warehouse inventories continuing to decline and recent US Federal Reserve rate cuts lending some macro support. Additional supply-side tightness was reflected in falling Japanese port stocks, operational disruptions at Iceland’s Grundartangi smelter, and output curtailments by Century Aluminium, while Japanese Q1 2026 import premiums are expected to surge sharply.

However, upside momentum remained capped by soft demand in several regions, particularly China, despite steady import growth. Market sentiment was further restrained by expectations of a seasonal slowdown in December due to year-end holidays, reduced trading activity, and planned smelter maintenance in Western regions. Mixed forecasts and cautious positioning kept prices confined to a narrow range.

Outlook

LME aluminium prices are likely to remain rangebound in the upcoming week beginning 15 December as supply-side support from declining inventories, firm import premiums, and ongoing smelter disruptions offsets weak seasonal demand. However, year-end holidays, thin trading volumes, and subdued demand in China are expected to cap upside. A clearer price direction may emerge early next year, driven by post-holiday demand recovery and policy signals from China.

Leave a Reply