- High port stocks keep prices under pressure

- Declining import prices keep sentiments bearish

Indian portside prices of Indonesian thermal coal registered a w-o-w decline as of 12 December 2025 primarily due to elevated inventories and restricted port handling capacity.

According to a market participant, nearly 1 million tonnes (mnt) of stock is currently accumulated at Navlakhi port, of which around 80% is MIFA-grade material. With no available space to manage new vessel arrivals, sellers are under pressure to liquidate existing stocks. Although traders are adjusting prices within a marginal range, these fluctuations have had limited impact on the broader market sentiment which remains largely stable but weak.

Portside assessments reflect broad-based softening

BigMint’s latest assessments showed a broad-based correction across Indonesian thermal coal grades, driven by muted buying interest and elevated portside inventories. The 5000 GAR grade remained unchanged at INR 7,200/t (Kandla) and INR 7,100/t (Vizag), reflecting limited market activity. Meanwhile, 4200 GAR prices fell by INR 50/t to INR 5,800/t (Kandla) and INR 5,700/t (Vizag), and 3400 GAR declined by INR 100/t to INR 4,500/t at Navlakhi. The overall softness highlights continued oversupply pressures and cautious procurement from buyers.

Freight rates firm amid tighter vessel availability

Supramax freight rates on the East Kalimantan-Navlakhi route increased by $0.70/dmt to $14/dmt, reflecting stronger vessel demand and tighter cargo schedules across the Indian Ocean. Higher freight adds mild upward cost pressure, but this has been outweighed by domestic portside oversupply.

Portside inventories increase, uneven stock movements

India’s portside thermal coal inventories rose marginally by 0.8% w-o-w, reaching 13.05 million tonnes (mnt) in week 49 compared with 12.94 mnt in week 48. However, the overall increase masked significant variations across individual ports. While certain terminals saw notable stock build due to low offtake, others reported declines amid improved dispatches. The uneven pattern of vessel arrivals and clearance rates shaped weekly stock dynamics.

Power plant inventories improve but supply chain gaps persist

Coal inventories at Indian power plants increased to 54.77 mnt as of 11 December, up from 53.89 mnt last week, providing approximately 18 days of consumption cover. Despite this improvement, 15 plants remain in the critical category, including units dependent on domestic coal, imported coal, and washery rejects. This highlights lingering logistical constraints and inconsistent coal movement in parts of the supply chain.

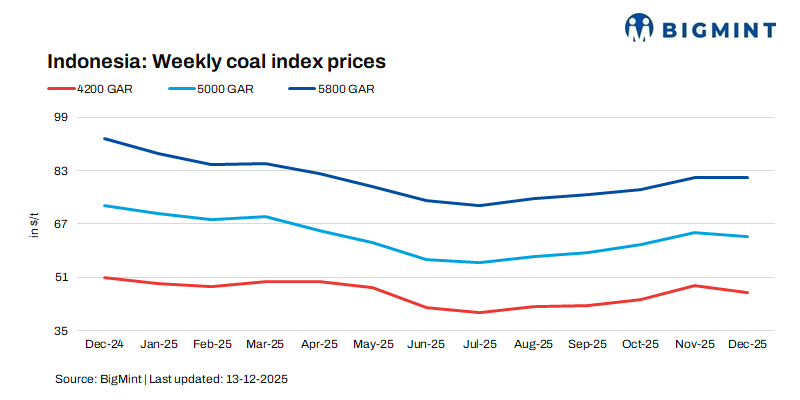

Indonesian seaborne prices ease as sellers prioritise clearance

Indonesian seaborne thermal coal prices declined week-on-week as exporters lowered offers to expedite stock liquidation amid weakening demand from key Asian buyers. Prices fell by $1.12/t for 5800 GAR, $1.6/t for 4200 GAR, and $0.77/t for 3400 GAR. This softening in export offers further reinforced bearish sentiment in the Indian portside market, where high inventories were already exerting downward pressure on prices.

Market outlook

Portside prices are likely to stay subdued in the near term, weighed down by persistent stock congestion, weak industrial offtake, and softer Indonesian seaborne offers. Adequate domestic supply to the power sector further limits upward support. Although faster stock clearance or a seasonal rise in industrial demand may offer temporary stability, the overall outlook remains mildly bearish unless demand strengthens.

Leave a Reply