- DGTR’s staggered proposal (12%-11%) awaits Finance Ministry nod

- 12% levy lapsed November 7, sparking fear of import surge

India’s steel sector stands at a decisive juncture. The industry enters a period of heightened uncertainty, with the 12% safeguard duty on select non-alloy and alloy flat steel imports having expired on November 7, 2025. The levy-activated when import prices fell below the $675-per-tonne CIF threshold for hot-rolled coil-had provided temporary insulation against aggressive overseas pricing.

Its expiry places the market at a crossroads, prompting close assessment within our organisation. The potential extension of a staggered, multi-year safeguard or a complete discontinuation of the measure would set markedly different trajectories for the sector. Two distinct scenarios now frame our evaluation of the post-duty landscape.

Scenario 1: provisional safeguard duty expired after 200 days period

If the provisional 12% duty lapses without renewal, low-cost HRC shipments from China and Japan could pour in unabated, bypassing the $675/t CIF threshold. This would erode domestic producers’ market share, intensifying pressure amid weak demand.

Price gap analysis when provisional duty expired

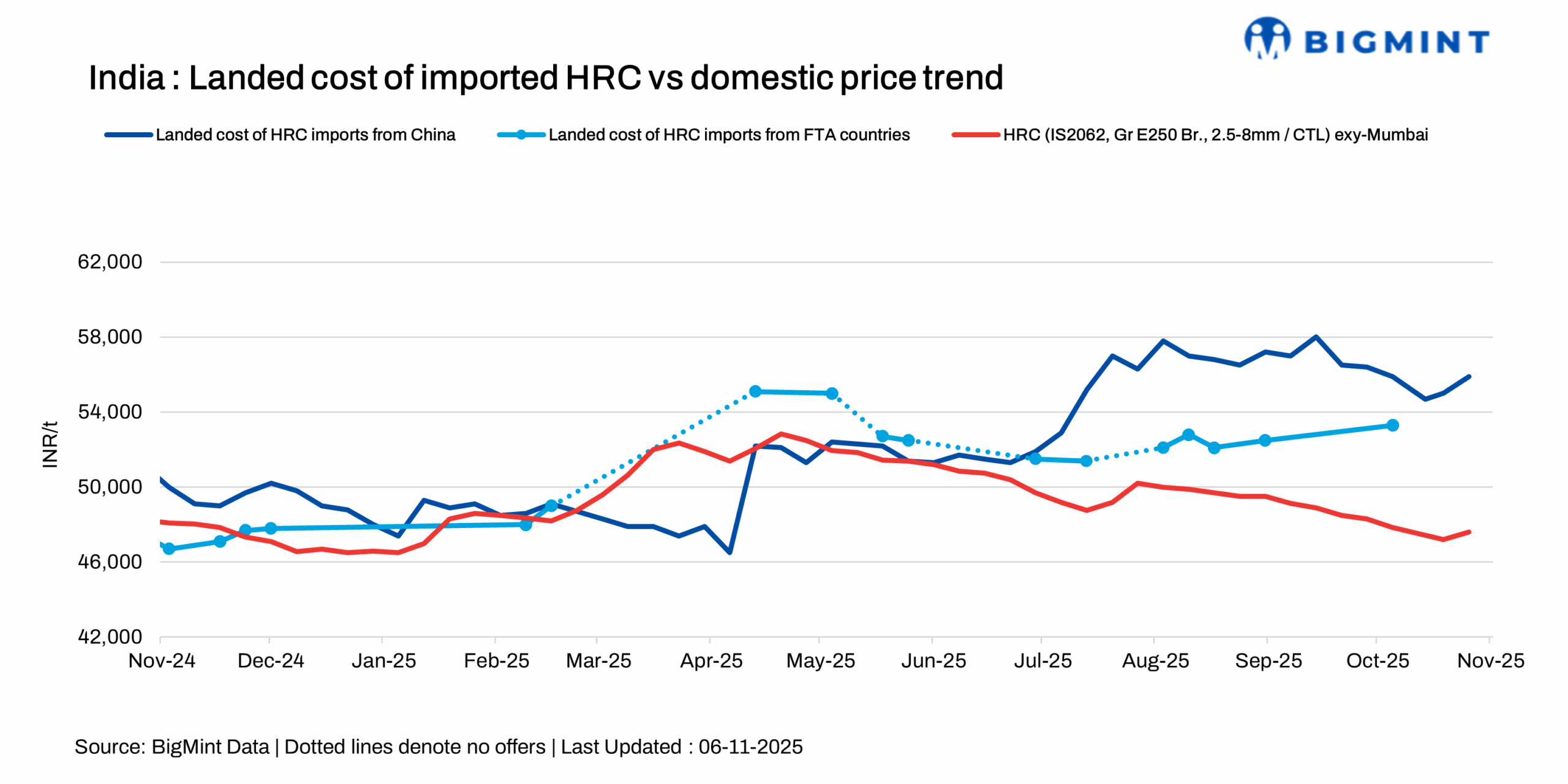

The import price scenario for HRC into India from China and Japan involves several cost components. The base prices are $505/t CFR for China, $535/t CFR for Japan.

For Chinese imports, a 7.5% Basic Customs Duty (BCD) and a 0.75% cess (10% of BCD) are applied, taking the effective cost to $547/t, while Japanese imports attract no BCD under FTA, so the cost remains $535/t.

If the safeguard duty lapses, no 12% levy applies, leaving only BCD and port handling charges. Including INR 2,000/t towards port handling and other miscellaneous charges, the landed cost is estimated at INR 51,400/t for Chinese HRC, INR 50,300/t for Japanese HRC.

When compared to the domestic HRC at INR 45,800/t (ex-Mumbai, ex-GST), Japanese imports are marginally costlier, while Chinese imports are notably more expensive.

Without safeguard duty, imports remain moderately more expensive than domestic HRC, offering only limited relief to Indian mills. Price competition from imports may persists, keeping domestic pricing under pressure.

Scenario 2: Three-Year staggered duty if imposed

Approval of the DGTR’s proposed staggered safeguard, 12% in the first year, 11.5% in the second and tapering to 11% in the third. This would limit cheaper imports, providing sustained relief to Indian mills. The domestic market would likely strengthen, supporting greater pricing stability.

Price gap analysis if duty gets imposed

For Chinese imports, a 7.5% Basic Customs Duty (BCD) and a 0.75% cess (10% of BCD) are applied, taking the effective cost to $547/t, while Japanese imports attract no BCD under FTA, so the cost remains $535/t as earlier.

However, as both these figures are below the threshold import price of $675/t, a safeguard duty of 12% and an additional cess of 1.2% (10% of safeguard duty) are levied, amounting to an additional duty of $72/t for China (i.e., 13.2% of the respective import value).

This brings the post-duty cost to $619/t for China or INR 55,900/t, $606/t for Japan or INR 54,700/t respectively. Adding INR 2,000/t for port handling and miscellaneous charges, the final landed cost comes to INR 57,900/t for Chinese HRC, INR 56,700/t for Japanese HRC.

Compared to domestic HRC at INR 45,800/t (ex-Mumbai, ex-GST), Japanese and Chinese imports remain significantly costlier.

The safeguard duty significantly widens the price gap, curbing cheap imports and strengthening domestic market demand. This creates long-term pricing stability for Indian mills and reduces vulnerability to external market fluctuations.

Domestic HRC prices

BigMint’s bi-weekly benchmark for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) saw a slight adjustment of INR 100/t ($1/t) w-o-w, settling at INR 45,700/t ($509/t) on 9 December 2025, compared to INR 45,800/t ($510/t) the previous week. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Leading Indian steelmakers have rolled over hot-rolled coil (HRC) and cold-rolled coil (CRC) prices for December 2025 sales compared with late-November list levels.

On a m-o-m basis, trade-level HRC prices declined by INR 1,200/t ($13/t) to INR 46,750/t ($520/t) in November 2025 compared with INR 47,900/t ($532/t) in October 2025.

Market Updates

Export channels offer limited support

Mills have maintained December list prices unchanged, reflecting constrained upside from both export and domestic markets. CBAM uncertainties and export allocations to the EU for Q4CY’25 have been fully exhausted keeping Indian HRC export indices flat. Additionally, muted Middle East buying amid regional holidays, alongside persistent weak demand and further dampens competitive dynamics despite reduced import arrivals.

Rupee depreciation

With the rupee weakening, imported steel becomes costlier, creating a natural price floor for domestic producers. Rupee depreciation amplifies safeguard duty effects, elevating landed costs for HRC imports by 4-5% amid recent INR 90+/$ levels. This curbs low-cost inflows from China, Japan, bolstering domestic pricing power.

Domestic Conditions stay subdued

Trade demand remains tepid, hampered by liquidity pressures that limit buyers to essential volumes only. With export avenues capped, overseas activity lackluster, and domestic sentiment soft, mills have held November list prices steady, forgoing any hikes.

Bulk HRC imports

India’s bulk hot-rolled coil (HRC) imports in November 2025 totalled 260,212 t, marking a sharp decline of 54% from an estimated 571,656 t in November 2024. Moreover, imports dropped by 34% compared to 391,856 t recorded in October which saw elevated shipments ahead of expected implementation of a key trade measure.

In November, South Korea, China, and Japan emerged as India’s top three bulk HRC exporters shipping 119,701 t, 491,85 t and 43,138 t, respectively. Additionally, imports from South Korea fell by 49% y-o-y and shipments from China decreased by 70.71%, while those from Japan dropped by 56.12% over the same period.

The m-o-m drop in HRC imports underscores market caution post the provisional 200-day safeguard duty’s expiry on November 7 for flat steel products.

Outlook

The Indian steel sector remains cautious following the expiry of the 12% provisional safeguard duty. With weak domestic demand, slow exports and subdued import flows are likely to keep prices range-bound in December and competitive dynamics under pressure.

Leave a Reply