- Average UK shredded prices drop $41/t y-o-y in 10MCY’25

- Imported shredded scrap priced lower than local material

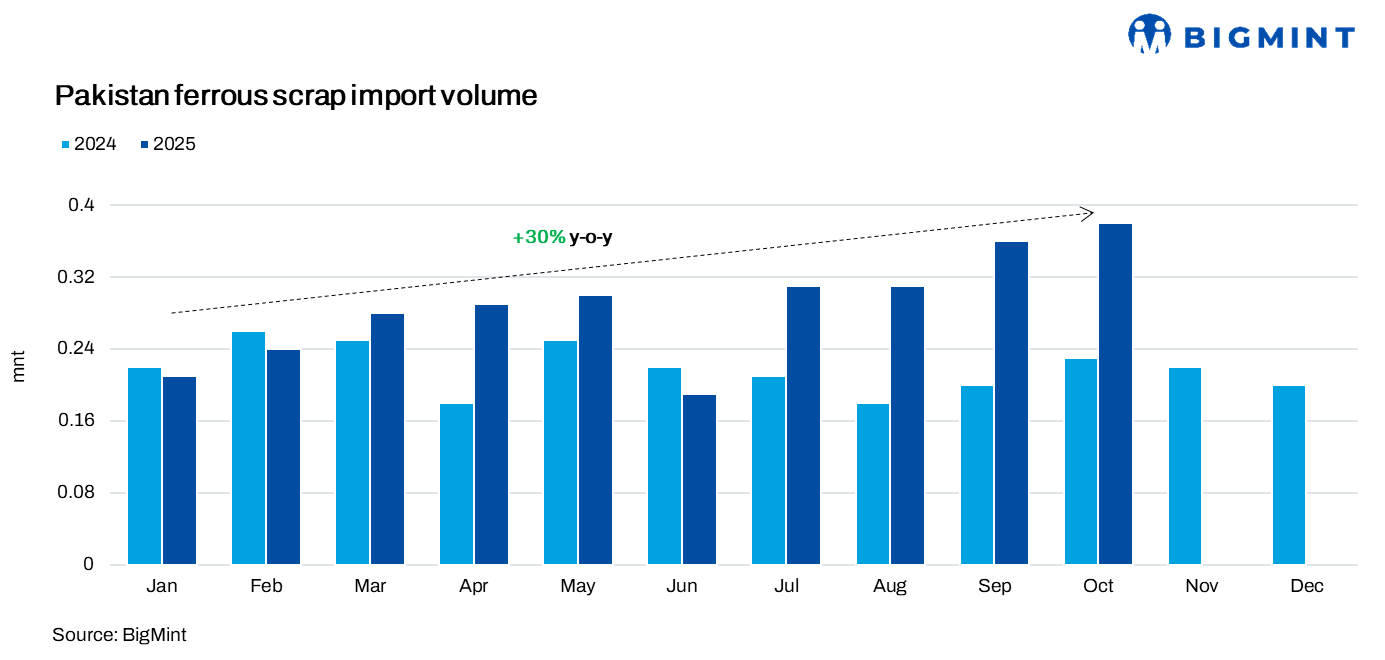

Pakistan’s ferrous scrap imports rose by 30% to 2.87 million tonnes (mnt) during the first ten months of CY’25 (10MCY’25) compared to 2.20 mnt in the same period of CY’24. Pakistan’s ferrous scrap imports rose sharply despite weak domestic steel demand due to a combination of policy relief, lower prices, supply diversion, and industry reliance on imports.

In October alone, imports reached 381,991 tonnes (t), reflecting a 6% increase from 359,759 t in September. On a y-o-y basis, imports were up 67% from 228,217 t recorded in October 2024.

Factors supporting imports

Duty, policy relief: Pakistan’s scrap imports rose after the FY’26 budget’s duty exemptions on HMS, shredded, and bundled scrap reduced landed costs. The removal of the 3% customs duty on HMS and the 2% additional customs duty (ACD) significantly reduced raw material costs for steelmakers.

Weak demand and liquidity issues in India, Bangladesh, and the Middle East led exporters to divert cargoes to Pakistan, where mills paid slightly better prices. Stable short-sea freight and steady EU/UK shredded offers further supported consistent import bookings.

Price competitiveness: Global shredded scrap prices were much lower in 2025 than in 2024, making imports more cost-effective. In contrast, domestic scrap remained costly due to weak collection rates, encouraging mills to rely more on imported material.

Average scrap prices

Pakistan: The average price of UK-origin shredded scrap in 10MCY’25 stood at $378/t, down $41/t from $419/t in 10MCY’24.

India: The average price of UK-origin shredded scrap was at $369/t in 10MCY’25, reflecting a drop of $38/t compared to $407/t in 10MCY’24.

Domestic market

Domestic scrap was expensive at PKR 135,000-140,000/t ($482-500/t), while imported shredded at $356-366/t CFR offered better value. With liquidity constraints, mills preferred small yet consistent containerised imports over costlier local scrap, keeping import demand steady.

Crude steel production: Pakistan’s crude steel production declined by 17% to 3.05 mnt in 10MCY’25 from 3.69 mnt in the same period of CY’24.

Outlook

Pakistan’s ferrous scrap imports are expected to continue at a stable pace in the near term. Duty relief supports continued buying by rebar mills, but weak demand, liquidity constraints, and cautious mill activity limit upside.

Leave a Reply