- Trade-level BF rebar prices increase by INR 700/t ($8/t) w-o-w

- High inventories keep buyer interest limited in HRC market

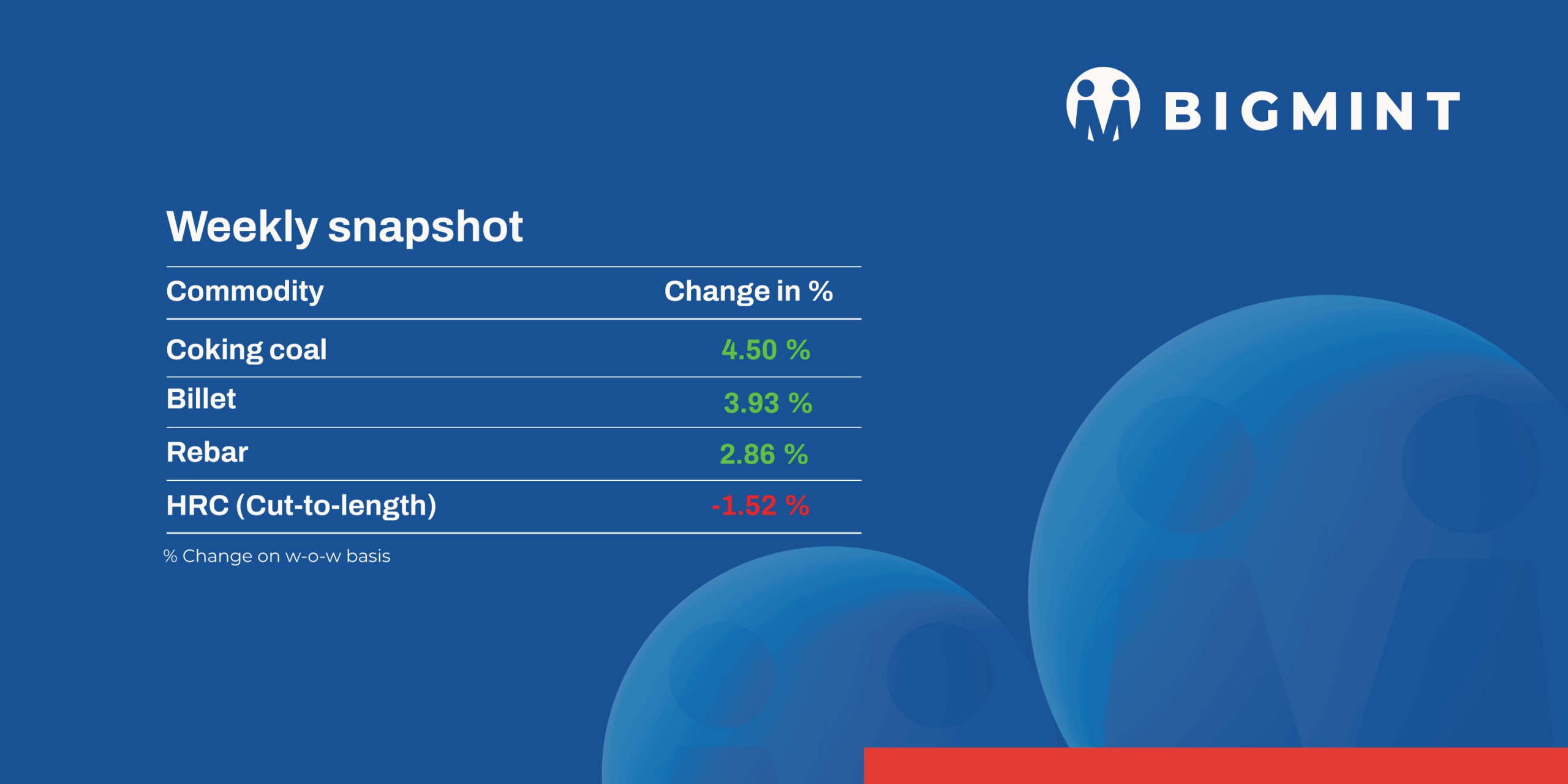

The domestic induction furnace (IF)–route steel market witnessed a positive price trend in week 49 (1–5 December 2025). Semi-finished steel prices edged up by INR 400–1,000 per tonne (t), while domestic finished long steel offers increased by INR 200–1,300/t. Trade-level reference prices for hot rolled coil (HRC) and cold rolled coil (CRC) remained range-bound across major markets this week.

Iron ore and pellet

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, remained stable at INR 9,650/t ($108/t) DAP on 5 December compared to the previous assessment on 2 December. Demand was limited in the last couple of days, however, around 15,000 t pellet (Fe 62.5-63%) was concluded by local sellers at INR 9,500-9,900/t exw Raipur.

- In NMDC Kumaraswamy (3 Dec) auction 96,000-t lumps (10-40 mm, Fe 59.63-61.21%) booked at INR 4,145-4,415/t against base price of INR 3,695-4,082/t; 116,000-t fines (Fe 56.17-61.29%) booked at INR 2,453-3,804/t. Meanwhile in Donimalai (2 December) auctions 28,000-t lumps (10-40 mm, Fe 55%) booked at base price of INR 2,850/t.

- BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index increased by $2/t w-o-w to $105.5/t FOB east coast on 5 December. Pellet demand was weak in the seaborne market, as Chinese steelmakers showed caution. Meanwhile, an export deal for around 75,000 t of Fe 64% pellets was recently closed at $125/t CFR China for end-of-December loading.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices increased by $1.5/t w-o-w to $68/t FOB east coast on 4 December. Meanwhile, the index stood at $79.5/t CFR China. BigMint heard approximately 450,000 t of export deals during this publishing period, primarily concluded by the east coast-based miners and traders.

Coal

- India’s thermal coal market showed a clear divergence as South African offers continued to rise while domestic buyers remained highly selective. Imported RB2/RB3 prices moved higher across ports, with RB2 reaching INR 8,800/t at Paradip, INR 8,700/t at Gangavaram and INR 8,650/t at Vizag. RB3 also increased to INR 7,300–7,400/t. Despite these gains, Indian buyers preferred to wait, resisting firm seaborne offers and focusing on domestic coal instead.

- Domestic coal prices fell by INR 100-150/t w-o-w, with 5,000 GCV dropping to INR 6,150/t and 4,500 GCV slipping to INR 5,050/t ex-Bilaspur. Buyers refrained from lifting coal purchased in earlier SECL auctions after observing sharply lower bid levels in the latest auctions as material bought earlier at higher prices would now incur losses.

- India’s met coke market showed a mixed trend in early December. Prices in east India firmed, with BF-grade material rising to INR 32,000/t ex-Jajpur as tighter supply and a 27,500 t deal supported sentiment. Western prices stayed unchanged at INR 30,200/t ex-Gandhidham, while foundry-grade coke in Rajkot held steady at INR 36,000/t amid selective demand. Higher seaborne coking coal costs and a weaker rupee added upward pressure, as Australian PHCC moved up to $202/t FOB. Overall, Indian met coke prices remained firm but upside stayed limited by soft regional fundamentals.

Ferrous scrap

- India’s imported scrap market remained selective, with stable cargo movement at Nhava Sheva, Mundra, and Chennai. Brazil HMS was $325-340/t CFR, turnings $300-305/t, and PNS $340-345/t, about $10-15/t below offer levels.

- Demand showed slight improvement but remained cautious due to tight Australian supply from winter yard closures, higher Turkish prices diverting exports, and a weak INR near 90/USD. Offers were stable at $350–352/t CFR EU shredded, $360-365/t Hong Kong PNS, $362-366/t Malaysian busheling, and $348-352/t Australian shredded, while HMS bids held around $324-325/t CFR Chennai, keeping trade selective.

- Some expect India’s imported scrap prices to rise on bullish domestic sentiment following GST action against scrap smuggling. Induction furnace producers continue receiving GST notices despite paying tax-inclusive prices, adding supply uncertainty.

- Approximately 8,000 t of imported scrap has arrived in India, including about 6,300 t of HMS at $323-335/t and rest remaining shredded, busheling and turning & boring.

Ferro alloys

Semi-finished

- India’s semi-finished steel market recorded a notable uptrend this week, as per BigMint’s assessment. Domestic billet prices across markets increased by INR 400-1,000/t ($4-11/t) w-o-w supported by moderate buying and improved outstation enquiries. Mumbai, Ahmedabad, and Raigarh registered sharp increases of INR 1,000/t ($11/t), leading the gains among major regional markets.

- The sponge iron market witnessed only marginal improvement, reflecting continued caution among buyers. Prices across key regions rose by INR 50-300/t ($0.5-3/t) w-o-w, but overall buying activity remained weak. Limited support from the finished steel segment and subdued offtake at elevated offer levels kept the market largely range-bound.

- Indian DRI (Direct Reduced Iron) export offers eased slightly by $2-5/t, assessed at $306/t CPT Raxaul and $315/t CPT Benapole. Despite the correction bookings from Bangladesh and Nepal surged during the week as buyers procured material on lower offer levels.

Finished Long Steel

- IF-rebar: India’s Induction Furnace (IF) route rebar prices recorded an upward movement on a w-o-w basis. Trading activity remained moderate, with manufacturers quoting higher offers over the past few weeks. Buyers continued to procure actively supported by steady demand from both the project segment and retail markets. Dispatches of previously booked material have also been smooth, which has limited the scope for additional discounts from manufacturers. Mill inventories have declined and are currently estimated at around 8-12 days across regions. As per current scenario, Market participants are expecting market to remain supportive in the near term also.

- On a weekly basis, prices of rebar increased in the range of INR 200-1,300/t across regions.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 39,300-39,700/t exw Raipur, INR 43,300-43,700/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 41,800-42,200/t exw Raipur.

- Trade reference prices of wire rod are hovering at INR 40,500-41,000/t ex Raipur.

- BF-rebar: India’s blast furnace (BF) rebar market witnessed mixed pricing signals in the week ended 5 December. Some leading primary mills increased rebar prices by up to INR 1,000/t ($11/t) for early-December, sources informed BigMint. Meanwhile, others rolled over their prices against levels seen last month.

- Trade-level BF rebar prices increased by INR 700/t ($8/t) w-o-w to INR 47,000/t ($522/t) exy-Mumbai, as per BigMint’s assessment on 5 December. Prices are exclusive of GST at 18%.

- In the projects segment, prices opened at INR 45,500-46,500/t ($506-517/t) FOR Mumbai basis.

Flate Steel

- Trade-level prices of hot-rolled coils (HRCs) in India showed mixed trends in the week ended 2 December. Prices declined in some markets, while other regions witnessed range-bound trends. HRC prices stood at INR 45,500-47,600/t ($506-529/t) across regions. Cold-rolled coil (CRC) prices ranged between INR 51,000-55,300/t ($567-615/t).

- The domestic HRC market remained sluggish this week, with prices maintaining a downward trend on muted demand. Market participants noted that elevated inventories kept buying interest limited. Mills rolled over prices for the current cycle as market conditions remain subdued.

- India’s bulk imports of HRCs touched 260,212 t in November, based on vessel line-up data. Around 113,056 t of additional cargoes are expected by early December.

- India’s bulk exports of HRCs touched 373,986 t in November, and around 41,715 t of additional cargo are in transit.

- BigMint’s Indian hot-rolled coil (HRC, S275) export index for the European Union (EU) region remained unchanged w-o-w to $520/t FOB main port on 2 December. The HRC (SAE 1006) export index for the Middle East also remained stable w-o-w at $475/t FOB.

Leave a Reply