- G5 premiums surge sharply as mid-CV availability tightened

- G3 premiums eased due to scarce UG supply

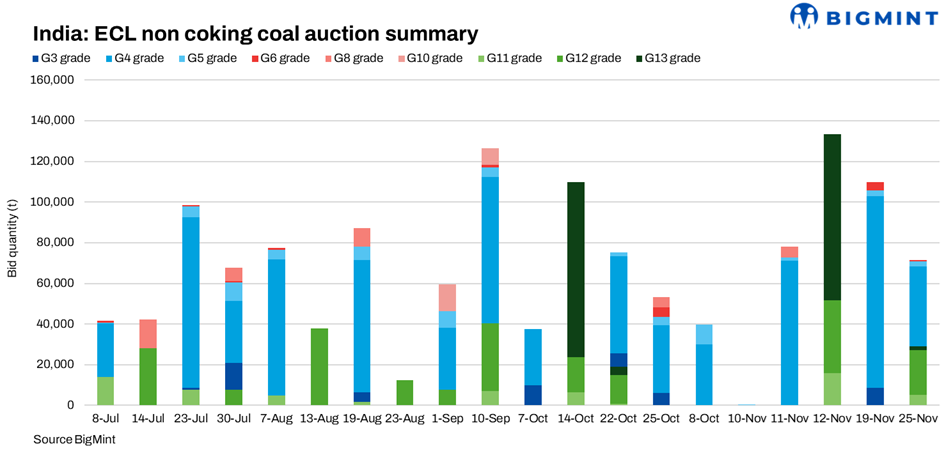

Eastern Coalfields Ltd (ECL) sold 78,800 t of non-coking coal in its auction on 29 November, reflecting steady demand for mid-CV grades despite a smaller offering compared with 100,450 t sold on 25 November. G4 again dominated allocations, while G5 recorded notable premiums, outperforming last week’s levels. High-CV supply remained extremely limited, with only 900 t of G3 available this round, significantly lower than the 6,000 t offered on 25 November.

Grade-wise performance: G4 leads; G5 premiums rise sharply

G4 (6,100-6,400 GAR) continued to anchor the auction with 72,400 t at INR 4,510/t, broadly stable compared with INR 4,667/t achieved on 25 November. Demand stayed firm across sponge iron and industrial buyers.

G5 (5,800-6,100 GAR) saw 5,200 t clearing at INR 5,213/t, significantly higher than the previous auction’s INR 4,101/t, signalling tightening regional availability.

G3 (6,400-6,700 GAR) remained scarce at 900 t, clearing at INR 4,674/t, much lower than the exceptional INR 6,891/t fetched on 25 November due to UG-origin constraints.

G6 (5,500-5,800 GAR) saw 300 t sold at INR 3,024/t, similar to last auction levels.

Mine-wise allocations: Sonepur Bazari anchors supply

Sonepur Bazari OC supplied the lion’s share with 60,000 t of G4 at INR 4,486/t, ensuring liquidity in the mid-CV segment. Premium G5 parcels from Amkola OC cleared at INR 5,289/t, the highest among OC mines. UG mines such as Kumardihi B, Shankarpur, and Pandaveswar recorded bids in the INR 4,440-4,650/t range, underscoring sustained interest in UG-origin G4 due to favourable ash quality.

G3 supply came solely from Central Kajora UG, explaining the lower premium compared with 25 November’s high-demand Jambad UG parcels.

Buyer-wise allocations: SS Enterprises leads procurement

SS Enterprises emerged as the largest buyer with 11,100 t at INR 4,511/t, followed by Janakpur Tradelink (6,100 t) and Mark Trading Company (5,350 t). Khatua Shyam Steels and Reet Sales procured moderate parcels in the INR 4,437-4,587/t range. Buyer behaviour remained cautious but consistent, with a clear tilt toward G4 and premium G5 lots.

Market scenario

The 29 November auction maintained firm sentiment despite a reduced offer size. G4 continued to clear at realistic, stable price points, while significant premium growth in G5 suggested tightening mid-CV availability. Lower G3 premiums reflected constrained UG supply rather than softening demand. Compared with 25 November, overall bid dispersion narrowed but remained quality-sensitive, particularly across UG-origin parcels. Price discovery stayed aligned with CV advantage, mine origin, and short-term industrial restocking needs.

Leave a Reply