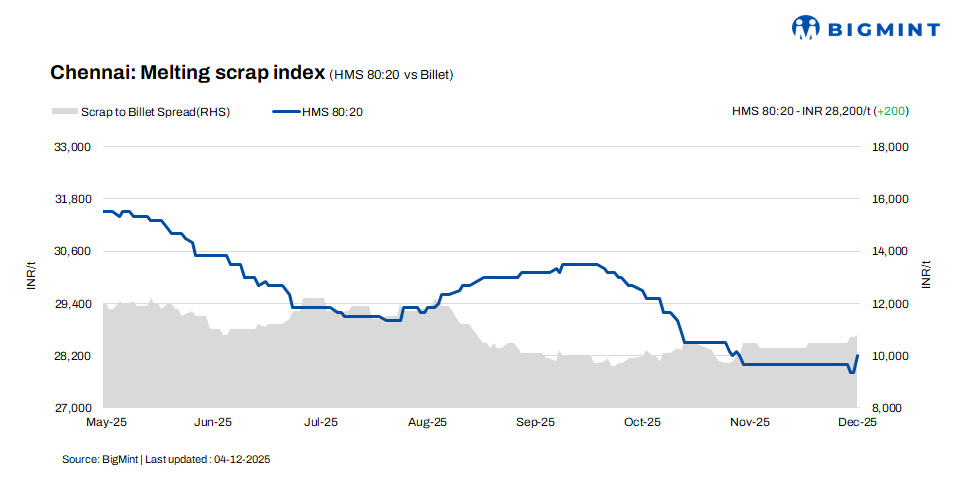

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai increased by 0.7% (INR 200/t) on a w-o-w basis to INR 28,200/t on 4 December, supported by a sharp d-o-d rise of INR 400/t. Billet prices saw an increase of INR 500/t w-o-w and d-o-d, now at INR 39,000/t. Rebar prices remained firm and assessed at INR 43,000/t, on both daily and weekly evaluations. Despite these improvements in scrap, limited movement in finished steel and tightening liquidity continue to influence trade behaviour, keeping overall sentiment cautious.

Imported, domestic market trends

According to a scrap trader, shredded scrap offers from Australia are currently priced at around $336-342/t, CFR Chennai, with bids coming in at $325-330/t. Meanwhile, offers for HMS 80:20 scrap are around $315-320/t. Buyers are not in urgent requirements so negotiating further for better prices.

In the Chennai market, domestic HMS (80:20) scrap is currently trading at INR 27,500-28,500/t for spot purchases with immediate payment. Transactions involving extended credit terms are commanding slightly higher prices of INR 28,000-29,000/t. Market participants indicated that most offers and finalized deals continue to cluster within the INR 28,000-29,000/t range, underscoring the impact of liquidity constraints and the increasing role of credit-based pricing in the scrap trade.

Buyer-supplier sentiments

According to a mill representative, “Trade in steel materials has been significantly impacted this week due to the Ditwah cyclone and persistent heavy rainfall. Although the flooding is gradually clearing, demand for finished steel remains muted. Scrap arrivals at mills are currently moderate, and in an effort to sustain inventory levels, mill operators have begun quoting marginally higher prices for raw materials, following several days of subdued scrap supply.”

According to a scrap supplier, “HMS (80:20) scrap prices are currently in the range of INR 28,000-29,000/t, depending on payment terms and mill-wise quantity requirements. Transportation has been disrupted for the last 4-5 days due to the cyclone and heavy rainfall, limiting suppliers’ ability to deliver material at normal capacities. Additionally, a prevailing liquidity crunch in the market has further slowed trade activity in recent weeks.”

Regional comparison

In the western India-based Jalna market, rebar and HMS (80:20) scrap prices remained stable at INR 43,200/t and INR 29,300/t, respectively, while billet prices increased by INR 200/t to INR 39,000/t. According to market sources, trade activity in finished steel has improved in recent sessions. Despite this, mills are not inclined to raise scrap purchase prices at the moment, as they are focused on stabilizing their conversion costs, which had narrowed earlier.

Outlook

As monsoon conditions ease, the finished steel market may experience a gradual pickup in trading activity. Scrap prices, however, are likely to remain range-bound with modest variations of nearly INR +/- 500/t in the coming days, influenced by the broader market environment.

Leave a Reply