- Approximately 450,000 t of export deals concluded

- Discount for Fe 57% fines hovering in the range of 16-17%

India’s iron ore export market remained firm this week, supported by a series of deals that helped lift market sentiment after a period of cautious buying. Market participants noted that while overall activity was moderate, the stability in prices has encouraged sellers to maintain offers, especially for low-grade material.

Prices, deals

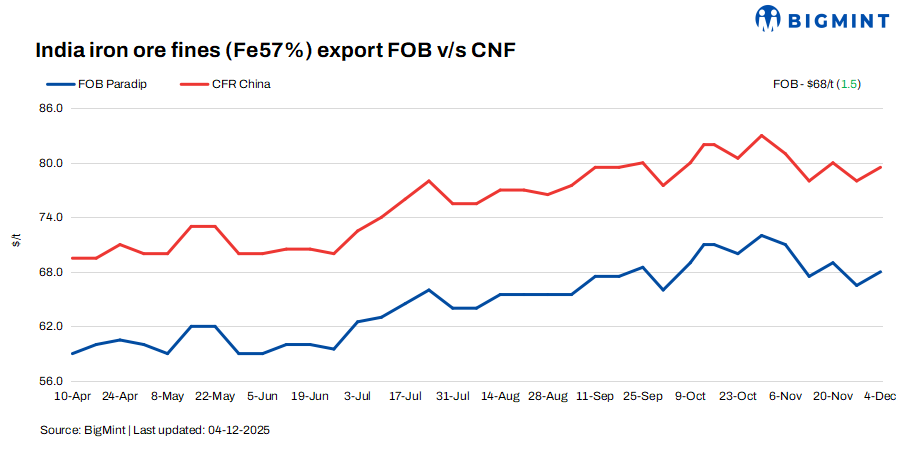

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices increased by $1.5/tonne (t) w-o-w to $68/t FOB east coast on 4 December. Meanwhile, the index stood at $79.5/t CFR China.

BigMint heard approximately 450,000 t of export deals during this publishing period, primarily concluded by the east coast-based miners and traders.

Market scenario

Exporters reported that the discount for Fe 57% fines continued to hover in the range of 16-17%, although a few negotiations were heard below this level as traders attempted to secure competitive cargoes. A trader commented, “The discount levels are stable, but buyers are still trying to negotiate due to uncertainty in China.”

The market is currently waiting for signals from the upcoming Chinese Politburo meetings, which many believe will provide direction for near-term demand. An international trader said, “The market is stable now. Everyone is waiting for the policy cues from China before committing to bigger bookings.”

Meanwhile, Odisha-based miners have continued to keep offers elevated for low-grade fines, citing higher sourcing costs and steady demand. This has led exporters to anticipate firmer bids from buyers seeking fresh cargoes. One exporter said, “Sourcing costs remain high, so we expect buyers to factor in these costs and submit slightly firmer bids for new deals. Our current ready-to-load cargo deals are under discussion with buyers.”

In the seaborne market, single-mine cargoes have gained preference among buyers compared to traders’ cargoes, resulting in a noticeable premium in recent transactions. According to a market participant, “Single-mines cargoes are fetching a premium with the buyers preferring with around $2-3/t premium.”

Chinese mills are anticipating the upcoming Politburo meeting scheduled for next week, hoping for a clearer market direction. As mill margins tighten, currently, mills are utilising available stocks and inventory stored at the ports.

There are market discussions regarding potential production cuts in mills located in North China driven by narrowing margins and weak demand from steel mills, which are exerting pressure on downstream products.

Chinese spot prices firm w-o-w: The benchmark iron ore fines index inched up $1/t w-o-w to $108/t CFR China on 3 December. The Asian seaborne iron ore market firmed up on improved macro sentiment, with a rebound driven by expectations of US Fed rate cuts and support from the upcoming year-end Politburo meeting. The domestic Chinese market saw the first coke price cuts, with trades focused on mid-grade fines.

DCE iron ore futures stable w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the Jan 2026 contract closed at RMB 794.5/t ($114/t) on 4 December, remaining largely stable w-o-w.

Rationale

- Four (4) major deals for Fe 57% were recorded during this publishing window, two (2) were taken for price calculation. Therefore, T1 trade was given 50% weightage in the index calculation. A few deals were already factored into Monday’s assessment. For the detailed methodology, click here.

- BigMint received eighteen (18) indicative prices in the current publishing window, and fourteen (14) were considered for price calculation as T2 inputs and given 50% weightage.

Iron ore inventories at major Chinese ports were recorded at 142.4 mnt on 4 December, surging by 3.36 mnt w-o-w, as per data published by SteelHome.

Outlook

Market participants expect Indian iron ore export prices to remain rangebound in the near term, with potential fluctuations in the coming week as buyers and sellers align with evolving global cues.

Leave a Reply