- Coke market shows mixed trends, prices stable in the west

- Supplies tight while buyer interest stays moderately strong

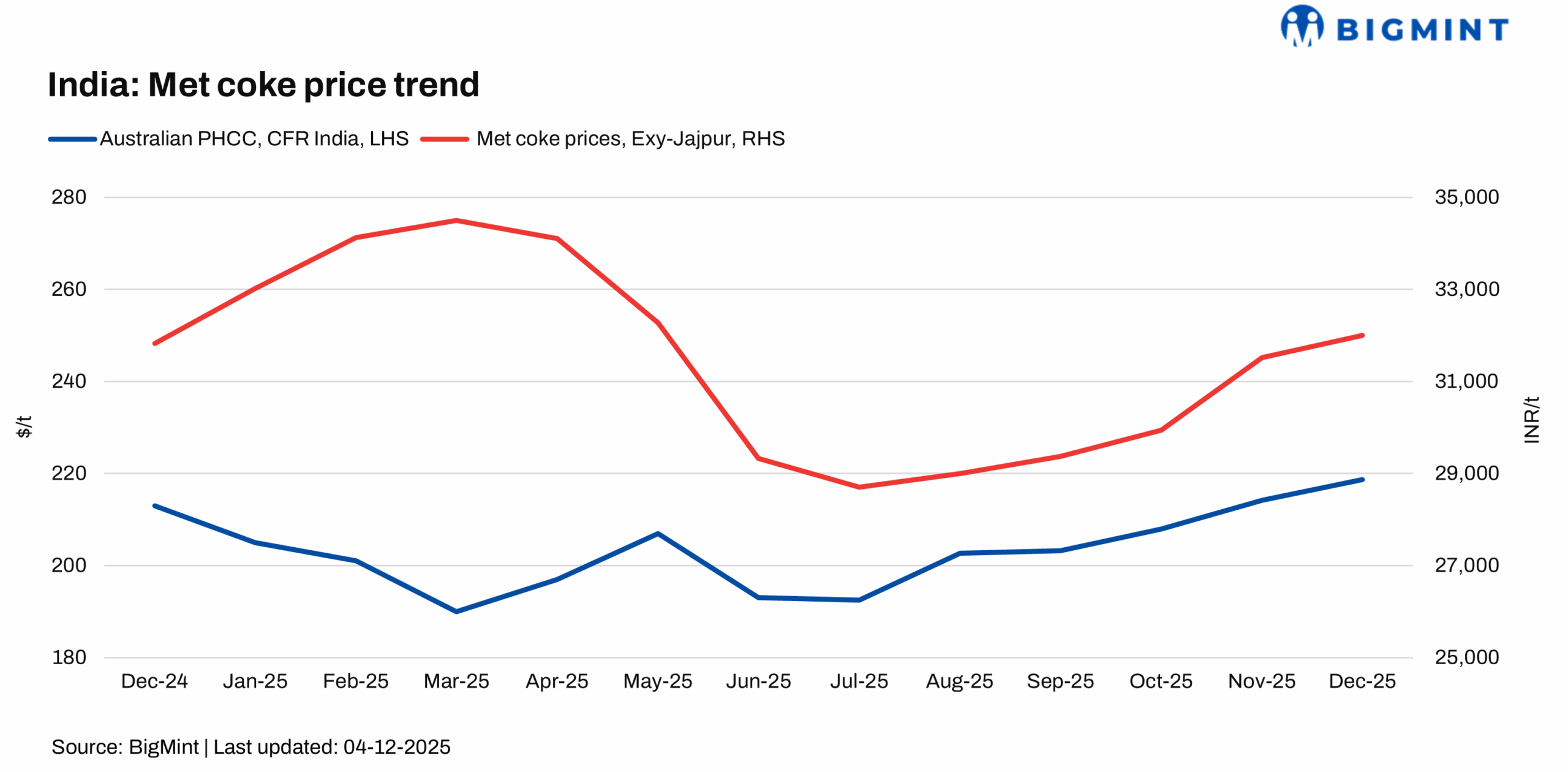

The Indian metallurgical coke market displayed a mixed picture during the week ending 4 December 2025, with prices firming up in east India while they were stable in the west. In the east, BF-grade (25-90 mm) met coke rose to INR 32,000/t ex-Jajpur, up INR 200/t w-o-w, supported by higher offers.

Meanwhile, in western India prices stayed unchanged at INR 30,200/t ex-Gandhidham, reflecting steady buyer interest. Foundry-grade met coke remained at INR 36,000/t ex-Rajkot, indicating shifts in niche demand.

Firm interest but supply stays thin

Eastern India saw a noticeable w-o-w uptick in BF-grade met coke prices, driven primarily by tighter supply conditions and a confirmed 27,500 t deal at INR 32,000/t exw. Market participants highlighted healthy demand, while supply constraints supported the uptrend. In addition, increased coking coal cost along with currency depreciation supported coke prices.

Western India maintained stability this week after last week’s increase. Offers held firm as procurement remained consistent but not aggressive. In the seaborne raw material space, Australian premium hard coking coal (PHCC) prices moved up by $3 w-o-w to $202/t FOB, offering cost-side support to domestic coke values.

China: Coke market extends weakness

China’s coke market continued to feel the pressure of weak sentiment, as raw coal supply increased and procurement remained cautious. Trading activity stayed sluggish, with online bids slipping further, underscoring expectations of prolonged softness.

Even though coking coal margins improved, coke offtake weakened as steel mills battled poor profitability, subdued steel demand, and more frequent maintenance shutdowns. Rising inventories and lower molten iron output deepened pessimism, signaling that near-term improvement in fundamentals remains unlikely.

Pig iron market: Sentiment mildly weak

Steel-grade pig iron ex-Durgapur slipped slightly to INR 32,300/t, down INR 50/t w-o-w.

NMDC auctioned 5,000 t of pig iron on 28 November which was fully booked at an average of INR 31,100/t, though management approval is still pending. Bids were INR 250/t higher than the 7 November auction.

SAIL-RSP sold 7,000 t on 29 November at INR 31,950/t exw, down INR 200/t from mid-November levels.

Outlook

Met coke prices in India are expected to remain firm, especially in the east, on increasing coking coal prices. Weakness in China may cap any major upside, while pig iron prices may stabilise as auction demand stays active but cautious.

Leave a Reply