- Wire demand remained resilient, keeping import volumes steadily higher.

- Vietnam tube exports shrank sharply under stricter Indian scrutiny.

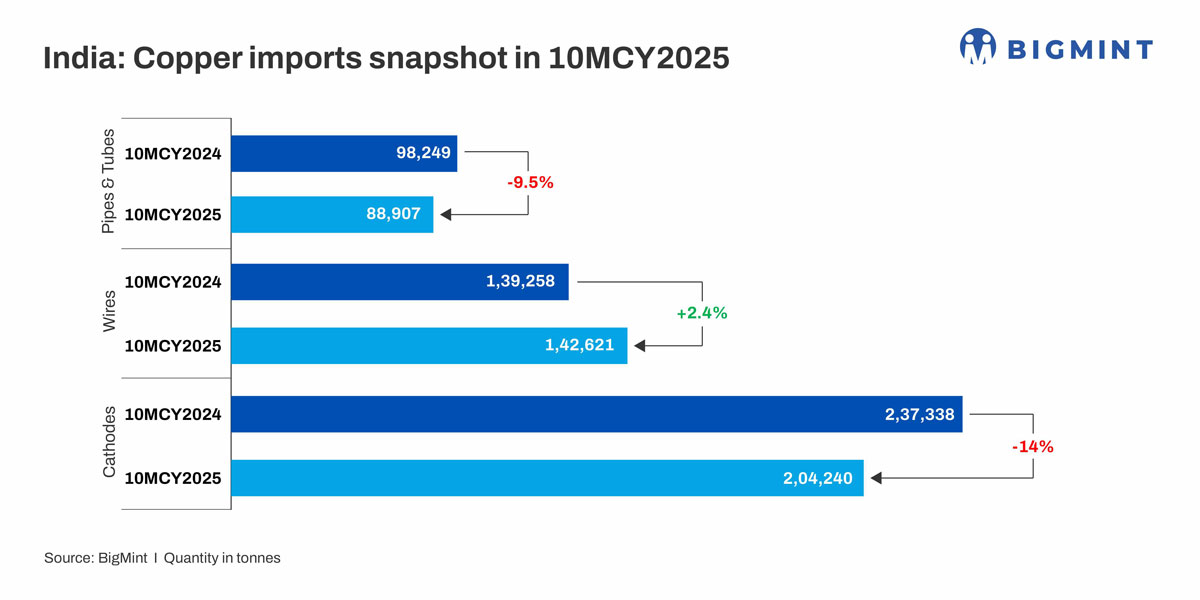

India’s copper downstream imports showed strong momentum in the first ten months of CY2025, led by higher inflows of wires and blister, even as pipe and tube shipments softened.

Copper wire imports rise 2.4% y-o-y in 10MCY2025

Copper wire imports increased 2.4% to 142,621 t in 10M CY2025, compared with 139,258 t in the same period last year. The gains were driven by higher orders from electrical and cable manufacturers, supported by robust construction and infrastructure activity.

Strong demand from leading cable-makers such as R R Kabel and Polycab India supported higher wire imports in 10M CY2025. R R Kabel reported a solid performance in Q2 2025, with its wires-and-cables segment — forming about 91% of its revenue — growing by roughly 22%, indicating a strong uptick in downstream wiring demand. Similarly, major players in the cable industry expanded capacity and increased output during 2025, reflecting robust order books across infrastructure, building construction, and consumer electrical markets.

This broad-based growth in electrical applications directly translated into increased requirement for high-quality copper wires from overseas markets. Stable demand from motor, transformer, and appliance manufacturers, particularly during April–August, also contributed. Additionally, copper wire imports in FY’25 hit a five-year high, though still remained below the over 200,000 t imported in FY’19 and FY’20. With several cable makers planning capacity expansions in FY26, wire imports are expected to sustain upward momentum.

As per data, India’s copper blister imports witnessed a sharp jump in 10M CY2025, reaching 171,605 t compared with just 35,307 t in the same period last year, marking a staggering 386% y-o-y increase.

Pipes & tubes imports decline 9.5% y-o-y in 10MCY2025

Copper pipes and tubes imports fell 9.5% to 88,907 t, down from 98,249 t in 10M CY2024. Vietnam’s copper pipe and tube exports to India fell sharply, dropping 27% y-o-y in 10M CY2025 to 44,833 t from 61,540 t in the same period last year. Vietnam has traditionally been India’s largest supplier of ACR and plumbing-grade copper tubes, but shipments weakened significantly through mid-2025.

The decline is partly linked to tighter customs scrutiny and documentation checks on ASEAN-origin consignments, which slowed clearances and reduced monthly inflows. Trade participants also indicate that some Indian buyers shifted to alternative suppliers amid longer lead times and uncertainty around compliance, contributing to the steep reduction in Vietnam’s share of India’s copper tube import basket. This may accelerate sourcing from domestic tube manufacturers, who are reportedly investing in higher-grade plumbing and ACR tube capacities.

Domestic cathode output rises

Cathode inflows, however, remained uneven, especially during early 2025, when the market faced certification delays, tighter compliance windows, and disrupted shipment schedules. Consequently, imports fell by 14% y-o-y to 204,240 t in 10MCY’25. Although imports increased by 7% m-o-m in October, this was largely due to the clearance of delayed shipments rather than a shift in fundamentals.

Higher domestic copper cathode production in the first half of the year has directly contributed to the decline in imports in 10M CY2025. Output rose to 303,000 t in Jan–June 2025, up 20% from 253,000 t in the same period of 2024, effectively adding 50,000 t of local supply into the system. This incremental production allowed smelters and downstream manufacturers to replace a meaningful portion of imported cathodes with domestic material, easing dependence on overseas suppliers at precisely the time when QCO ‑related frictions, longer lead times, and higher landed costs were discouraging fresh import bookings. Several domestic smelters are also reportedly planning debottlenecking and capacity utilization improvements in H2 CY25, which could further strengthen local supply.

Outlook

With the removal of QCO-related restrictions on copper cathodes, imports may witness a rebound in the coming months. While domestic production has been strong—rising 20% in H1 2025 to 303,000 t, which temporarily reduced reliance on imports—smelters and downstream manufacturers could turn to overseas supplies again once certification and compliance bottlenecks are cleared. A relaxation of QCO compliance is likely to shorten lead times and reduce landed costs, making imported cathodes more attractive and potentially reversing the 14% y-o-y decline seen in 10MCY’25. This is also likely to encourage downstream players to replenish inventories ahead of peak demand seasons, supporting cable, wire, and tubing manufacturers who are gearing up for FY26 growth.

Leave a Reply