- G6 grade coal records highest premium

- UltraTech, Mangalam Cement among top bidders

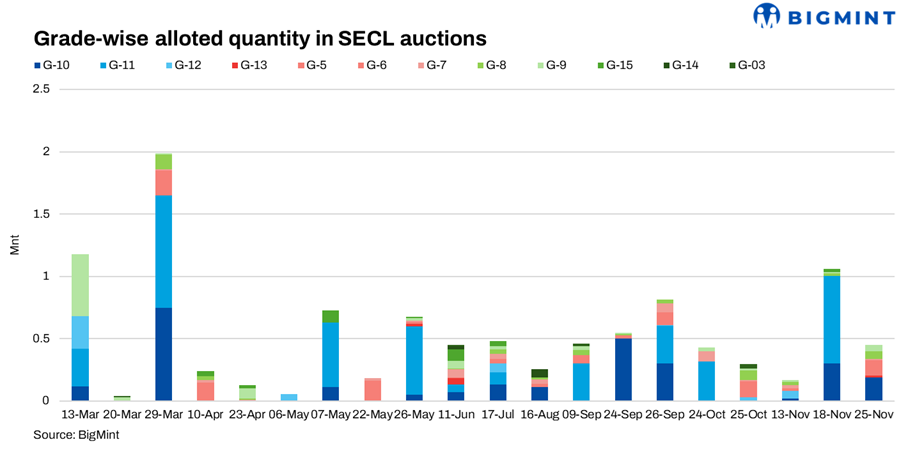

South Eastern Coalfields Ltd (SECL) sold 446,750 t of non-coking coal in its auction held on 25 November 2025, marking yet another strong performance with almost the entire quantity getting booked. The auction reflected firm industrial procurement across aluminium, cement, sponge iron and trading segments, with buyers showing clear preference for mid- to high-CV domestic coal as imported alternatives remained costlier due to higher freight and INR depreciation.

Grade performance remained distinctly firm, with G10 registering the highest allocation at 189,200 t, clearing at INR 1,630/t, which represented a 20.2% premium over the notified price of INR 1,356/t. The grade maintained its position as the most widely traded supported by consistent demand from captive power and metallurgical units. G6, with a calorific value range of 5,200-5,500 kcal/kg (NAR), emerged as the most aggressively bid grade, where 125,000 t cleared at INR 3,701/t, reflecting a significant 34.4% premium above its base price of INR 2,754/t, signalling strong interest from cement manufacturers preparing for winter requirements.

Higher mid-CV grades also saw notable premiums. G9, with a CV of 4,300-4,600 kcal/kg (NAR), witnessed 50,000 t being booked at INR 3,025/t, more than doubling its floor level, resulting in a 101.3% premium, which was one of the highest across the auction. Grade G8 performed steadily across both size categories, with the 100 mm segment clearing at INR 2,543/t and the 250 mm segment at INR 2,457/t, translating into premiums of 32.1% and 27.6%, respectively. Even the smaller-volume G7 grade, clearing at INR 3,356/t, reflected a 32.5% premium, while low-CV G14 secured 16,000 t at INR 1,113/t, about 20% above its floor price.

Supply distribution across mines added depth to the auction. Chhal contributed a major share with 176,000 t of G10 clearing at INR 1,628/t, demonstrating stable interest for mid-CV blends. Rampur Batura supplied 125,000 t of G6, which registered one of the highest clearing prices of the auction. Premium performance was also evident at various underground mines, such as Haldibari, where G7 cleared at INR 3,356/t, and Bangwar, where G8 commanded INR 2,543/t. Mines such as Rajnagar, Jagannathpur and Baroud contributed meaningfully, collectively ensuring balanced availability across CV ranges.

On the buyer side, aluminium, cement and large trading companies dominated procurement. BALCO led the list with 40,000 t booked at INR 1,628/t, focusing largely on G10 volumes. UltraTech Cement purchased 29,600 t at INR 3,054/t, securing substantial G6 and G8 parcels to strengthen their fuel requirement for clinker operations. Mangalam Cement paid among the highest average prices at INR 3,785/t for its 25,000 t, reinforcing strong procurement interest for higher-CV grades. Aggregated purchases from Agarwal Coal Corporation, Mohit Minerals, and RR Business further reflected the broad-based market participation typical of late-November auction cycles.

Rising demand for domestic coal

High premiums on G6-G9 signalled tightening supply of mid-to-high CV domestic coal. Cement companies aggressively secured G6 and G8 parcels, reflecting winter demand preparation. The near-complete sell-through demonstrated renewed restocking after weak procurement in early November. Overall, the auction highlighted firm demand recovery, especially from cement, aluminium, and sponge iron sectors.

Outlook

SECL auctions are expected to continue seeing strong premiums through early December, supported by tight availability of mid- and high-CV grades and strong cement sector procurement. Competition is likely to remain elevated, especially for G6-G9 grades, until arrivals improve or imported prices correct meaningfully.

Leave a Reply