- Unseasonal rains damage 2025 colour-grade crop

- Prices remain range-bound on soft global demand

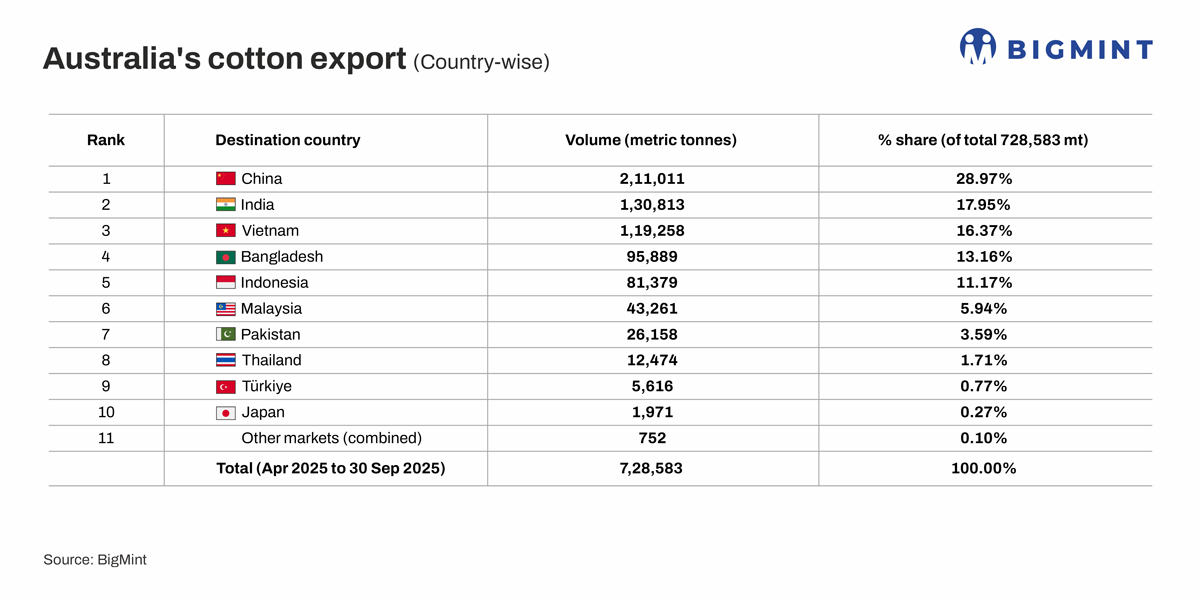

Australia’s cotton industry closed the 2024-25 crop cycle, with a modest decline in exports: volumes fell nearly 10% y-o-y to 728,583 tonnes (t) of cotton bales from 790,000 t, as per data maintained by BigMint. Demand for Australian cotton weakened, as unseasonal rains in March-April 2025 led to a deterioration in harvest quality and dampened importers’ interest in sourcing material.

Region-wise break-up

In terms of regions, exports were led by China (211,011 t, 28.97% of total exports), India (130,813 t, 17.95%), Vietnam (119,258 t, 16.37%), Bangladesh (95,889 t, 13.16%), and Indonesia (81,379 t, 11.17%).

Quality downgrade slows export momentum

Despite a promising start to the 2025 harvest season, late-season rains in March-April 2025 once again damaged colour grades, marking the second consecutive year in which weather in just 1-2 weeks altered quality expectations. This led to slower exports from Australia during April-September 2025, though other fibre parameters held firm against last year.

As per a report from Textile Value Chain, in terms of fibre strength, about 90% of the crop recorded 29 grams per tex (GPT) or better, 87.82% fell within the G5 micronaire range (3.5-4.9), and more than 50% achieved 38-staple (i.e., an upper half mean length of approximately 30-31.5 mm) or higher. Leaf performance remained strong despite the higher share of lower colour grades.

Prices remain range-bound

Australian export prices remained stuck in the 65-69 cents/lb range through most of Q3 and Q4 in CY’25, as global demand was soft and mills continued hand-to-mouth buying.

Macroeconomic pressure in major consuming economies (the US, the EU, and China), slow apparel sales in key retail markets such as the US and Europe, and cautious Chinese import behaviour limit the chance of a near-term upside breakout.

Implications for global market

Australia has already begun planting its 2026 crop, with strong early progress. Forward sales near AUD 575/bale indicate cautious optimism, though cotton cultivators still aim for AUD 600/bale, suggests Textile Value Chain.

For ginners, spinning millers, and brokers worldwide, the clear takeaway is that high supply in the Southern Hemisphere — particularly from Australia and Brazil — will continue to influence pricing, quality spreads, and trade flows well into early 2026. High-strength lots will remain in demand, while lower colour grades could attract mills seeking cost-effective blending options. Australian cotton’s reliability in micronaire, length, and leaf grade provides relative stability compared to several Asian and African origins, even though Australia has faced colour-grade deterioration in the past two seasons.

Role of Australian exports in Indian cotton industry

With India now the second-largest buyer of Australian cotton (accounting for 17.95% of exports in April-September 2025), spinning millers increasingly rely on Australian fibre for fine-count and high-value yarns. Consistent strength and micronaire — relative to domestic Indian cotton, which faces moisture, contamination, and variability during arrivals — make Australian cotton attractive during India’s peak-arrival months of November to February, when moisture and grade variability rise domestically. Increased Australian inflows may put pressure on Indian lint prices by reducing mill dependence on local fibre, widening the gap between MSP and mandi rates and increasing CCI’s procurement load. Ginners could face tighter margins, while spinning millers and yarn exporters may benefit from more predictable fibre behaviour and improved blending options.

Looking ahead, India’s import decisions will depend on the quality of domestic arrivals, the price direction on the Intercontinental Exchange (ICE), freight stability, and whether Australian 2026 production returns to higher colour grades. If global demand for cotton, yarn, and apparel recovers even marginally, Australia and Brazil will capture early buying from international mills and traders, while India will balance between domestic fibre and well-priced imports to protect yarn competitiveness.

Leave a Reply