- Flooding and storms keep Vietnam’s scrap demand low

- Deep-sea prices unworkable, limiting Vietnam scrap trades

Vietnam’s imported scrap market stayed largely stable but sluggish, with firm offers yet weak demand due to severe weather, low mill inventories, and unworkable deep-sea pricing, while domestic HMS scrap prices held within a steady bid range.

Weekly assessments

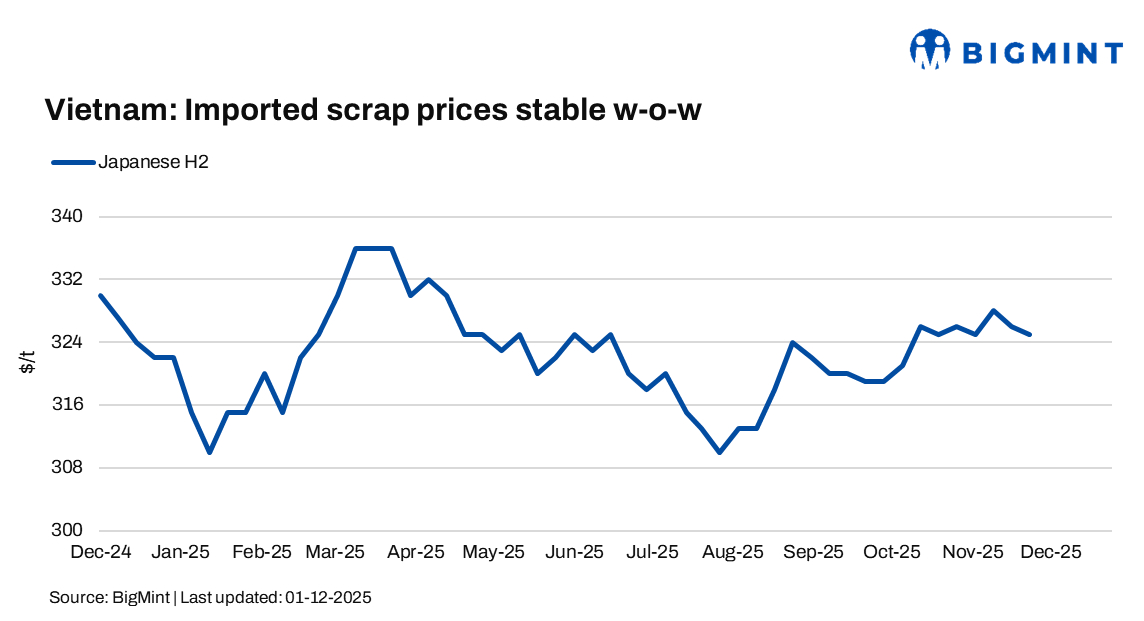

- Japanese H2 scrap was at $325/t CFR, down by $1/t w-o-w.

- US-origin HMS 80:20 bulk stood at $345/t CFR Vietnam, down by $1/t w-o-w.

Market updates

H2 offers remained steady at $325-327/t CFR, while bids hovered around $320/t CFR, placing the tradable level near $323/t CFR and US-origin HMS 80:20 bulk offers were reported at $350/t CFR, while deep-sea HMS 80:20 offers held firm around $355/t CFR. Indicative bids remained stable in the $340-342/t CFR range.

Vietnamese buyers postponed scrap bookings as persistent weather disruptions, including heavy rains, flooding, and an approaching tropical storm, combined with weak steel demand. Mills kept inventories low, showing little urgency to purchase new cargoes, keeping market activity subdued.

Although year-end typically stimulates restocking, market participants noted that this season’s unusually severe weather has prevented the usual improvement in buying momentum.

Rising Turkish scrap prices made deep-sea offers into Southeast Asia less workable, keeping suppliers firm. Vietnam’s imported scrap market stayed stable but sluggish, with steady offers and persistently weak demand through the week.

Domestic updates

Domestic HMS (3-6 mm) scrap prices in Vietnam remained rangebound, with bids in the South reported at VND 77,00-88,00/kg ($292-334/t) delivered, excluding VAT. In the North, bids were slightly higher at VND 83,50-92,00/kg delivered, excluding VAT.

Outlook

Vietnam’s scrap market is likely to stay weak in the near term as severe weather and soft steel demand curb buying. Firm deep-sea offer levels will limit negotiations, and demand may only improve once weather conditions stabilize and steel consumption picks up.

Leave a Reply