- North America posts sharp 18% m-o-m production jump

- China’s output inches up as power-related disruptions ease

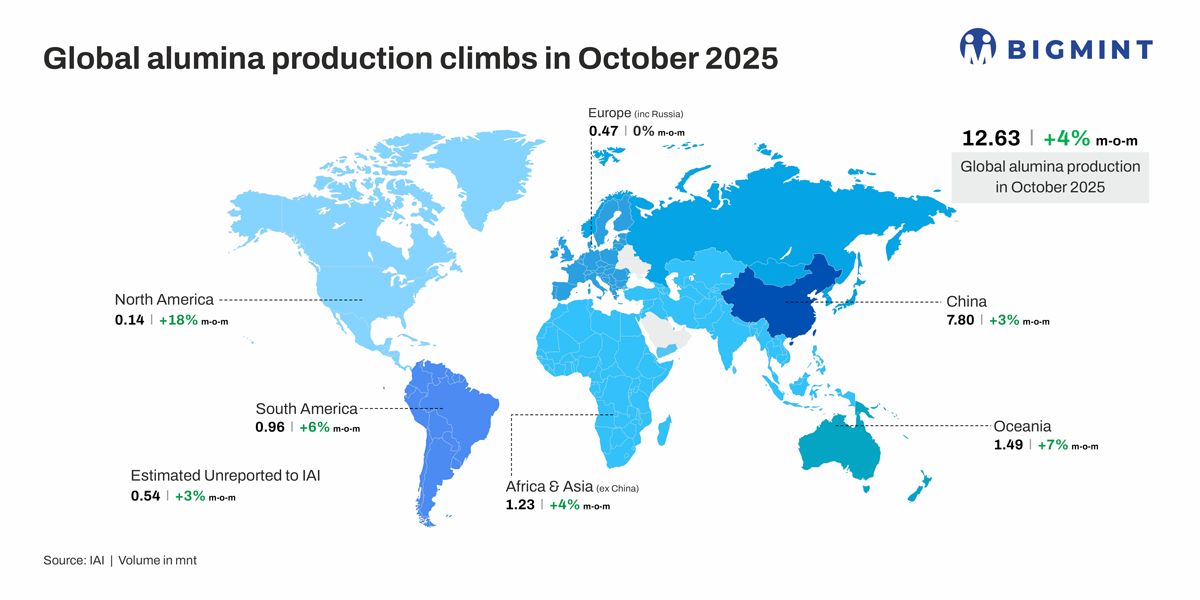

Global alumina production increased by 4% m-o-m to 12.63 million tonnes (mnt) in October 2025 from 12.14 mnt in September, according to the International Aluminium Institute (IAI). This growth reflects improved operating conditions, stabilised energy availability, and normalised refinery output across key producing regions.

Cumulative production in January-October reached 119.90 mnt, compared with 114.12 mnt during the same period last year, marking a steady 5% growth and underlining robust global demand and efficient refinery performance.

Regional performance highlights

China, the world’s largest alumina producer, posted a 3% m-o-m increase to 7.80 mnt in October, from 7.55 mnt in September. Improved refinery operations following earlier power-related disruptions supported this growth, with China continuing to account for more than 60% of global output.

Oceania’s production rose 7% to 1.49 mnt as Australian refineries completed scheduled maintenance and restored normal operations.

Output in Africa and Asia grew 4% m-o-m to 1.23 mnt, supported by smoother operations in India and the Middle East following September’s energy and logistical challenges.

South America rebounded strongly, posting a 6% increase to 0.96 mnt, aided by improved plant utilisation in Brazil after earlier refinery constraints.

North America recorded the strongest growth, with output rising 18% to 0.14 mnt, reflecting higher capacity utilisation at select refineries.

Europe (including Russia) remained stable at 0.47 mnt, though the region continues to face challenges from energy market restrictions and raw material supply issues.

Recovery after disruptions in Sep’25

The October increase largely reflects recovery from September’s operational interruptions, including power rationing in China, scheduled maintenance in Oceania and the Middle East, and reduced roasting loads due to local regulatory events. With these issues resolved, operating rates normalised across major producing regions.

Q3 performance also provided momentum, with metallurgical-grade alumina rising from 34.937 mnt to 37.002 mnt and chemical-grade increasing to 2.385 mnt. Consumption reached 109.7 mnt in January-September, closely matching production, and full-year consumption is projected at 142 mnt, closely aligned with forecast production of 145 mnt.

Outlook

Global alumina production is expected to remain steady in the near term, supported by stable refinery operations, better energy availability, and continued demand from the aluminium sector. While Europe may face some challenges due to energy and raw material constraints, overall production is likely to grow moderately and maintain a healthy balance with consumption.

Leave a Reply