- QCO-driven disruptions lead to 14% drop in cathode imports

- US exports to India surge y-o-y amid tepid domestic demand

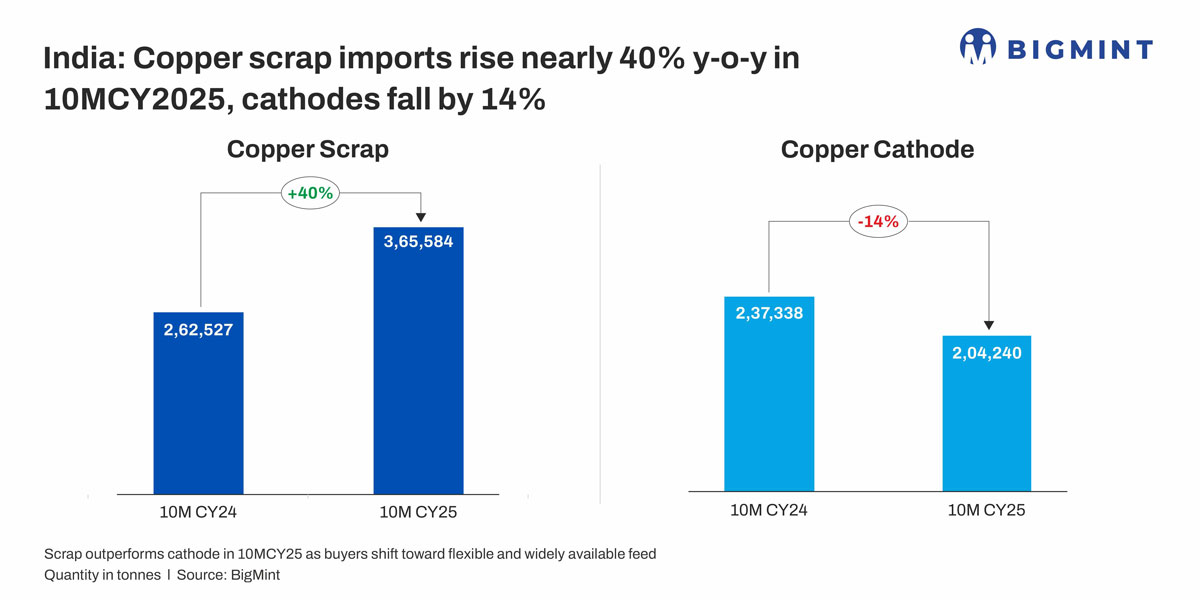

India’s copper scrap imports increased by 39% to 365,600 tonnes (t) in January-October 2025 (10MCY’25) compared to 262,500 t, supported by competitive global pricing, persistent domestic supply gaps, and robust downstream demand. The increase in scrap imports was also driven by a decline in cathode imports, stemming from regulatory bottlenecks.

Notably, monthly arrivals of copper scrap averaged nearly 36,600 t in 2025, compared with 26,300 t last year, reflecting strong buying interest despite periodic price volatility on the London Metal Exchange (LME). Monthly arrivals also steadily climbed up from 24,600 t in January to nearly 48,000 t in October, reflecting aggressive procurement as scrap remained more accessible from the US, EU, and Middle East. This was also supported by improved logistics, favourable arbitrage, and stronger availability.

Copper cathode imports fall 14% y-o-y

Cathode inflows, however, remained uneven, especially during early 2025, when the market faced certification delays, tighter compliance windows, and disrupted shipment schedules. Consequently, imports fell by 14% y-o-y to 204,240 t in 10MCY’25. Although imports increased by 7% m-o-m in October, this was largely due to the clearance of delayed shipments rather than a shift in fundamentals.

Several buyers continued to defer cathode bookings through the year due to certification bottlenecks, uneven shipment cycles, and softer domestic offtake. This created a clear market divide, where scrap maintained strong momentum, while cathode demand remained cautious and reactive. Notably, many mid‑sized CCR and brass units now indicate that scrap has shifted from being a “supplementary” feed to a “base” feed, with cathode used tactically only for quality‑critical orders or when discounts briefly improve.

Factors influencing India’s scrap imports in 10MCY’25

QCO/BIS-induced disruptions in cathode supply: The Quality Control Order (QCO) on copper cathodes — requiring BIS certification — altered India’s import landscape significantly. Several overseas smelters faced delays, scaled back offers, or temporarily exited the Indian market, creating multi-month gaps in primary metal availability during Q1 and Q2 of CY’25.

This pushed downstream units towards more flexible alternatives such as scrap, as shipments remained predictable, with comparatively stable availability from major supplying regions, including the US, EU, and Middle East.

Preference for flexible blending options: Berry (+75% to 21,200 t), Druid (+74% to 50,400 t), and Birch (+36% to 38,800 t) feature among the grades recording the highest percentage increase in imports in 10MCY’25.

Copper recyclers find the ability to blend Druid, Berry, and Birch with internally generated scrap and still meet customer specifications as a strategic advantage, which has encouraged mills to invest more in sorting, shredding, and refining rather than paying a premium for cathode.

Grades such as Berry, Candy, Birch/Cliff, Cliff, Dream, Druid/Droid, and Honey are commonly blended because they have predictable copper content, low impurities, and stable melting behaviour. This is important because secondary copper producers need to mix scrap grades to achieve exact Cu% requirements, control furnace chemistry, reduce melting losses, and optimise production costs, making consistent, blend-friendly grades essential for efficient and reliable copper recycling.

Improved scrap refining, sorting capacities: Processors increasingly treated scrap as a strategic feedstock, supported by upgraded refining and sorting capacities across key clusters, which strengthened operational confidence and made scrap-based production planning the default approach for many CCR, brass, and alloy manufacturers.

Ample supply from US: US copper scrap exports to India surged sharply in 10MCY’25, by 169% y-o-y to 84,000 t from 31,300 t, as American suppliers released large volumes of accumulated post-industrial scrap amid subdued domestic consumption. At the same time, India’s lower import duties and stronger demand from wire rod, cable, and electrical manufacturers increased the pull for cleaner, high-grade imported scrap. Tight availability of refined copper in the Indian market further accelerated the shift towards US-origin secondary material.

Outlook

Industry sentiment suggests scrap will continue to dominate India’s copper import basket through early 2026. Even though the QCO/BIS requirement on cathodes was withdrawn in October, market participants do not expect an immediate improvement in cathode inflows.

Overseas smelters will require time to re-align supply chains, re-establish booking cycles, and reconfigure logistics after months of disrupted shipments. With this delayed reaction expected to stretch into early 2026, buyers foresee a continued reliance on scrap in the near term, supported by favourable economics, reliable availability, and a more flexible procurement environment compared to cathode.

Higher reliance on imported scrap will also be sustained by limited capacity expansions at domestic smelters. Market participants also expect continued investment in sorting, refining, and grade optimisation to enhance feedstock flexibility and manage cost volatility.

Additionally, even if cathode availability normalises, scrap will likely retain a structurally higher share of India’s copper balance — driven by cost advantages, fewer compliance hurdles, and the growing circularity ecosystem.

Leave a Reply