- Govt battles overcapacity with ‘anti-involution campaign’

- Mills limit operations amid shrinking profits, pollution control measures

- Steel demand projected to fall by 2% in 2025, 1% in CY’26

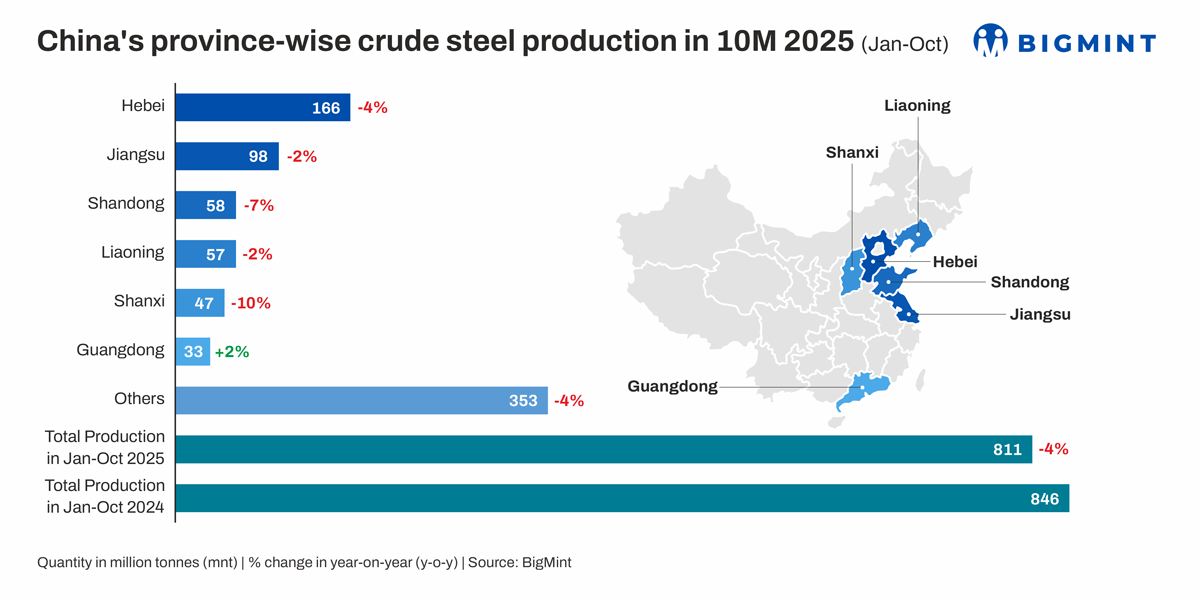

Morning Brief: China’s crude steel output contracted by 4% y-o-y to 811 million tonnes (mnt) in January-October 2025, as the government and domestic mills recalibrated production strategies amid a persistent supply glut and declining steel consumption.

October alone witnessed a 12% y-o-y decrease to 72 mnt. This marks the fifth consecutive month with a decline, driven by shrinking profit margins, increased pollution-driven operational halts, and weak steel demand.

Region-wise production trends

All regions, except for Guangdong, witnessed modest drops in crude steel output in January-October 2025.

Hebei, the leading steel production hub, recorded a 4% drop to 166 mnt. Notably, Hebei’s Tangshan region has been the target of a number of environment-driven production restrictions.

Jiangsu followed, registering a 2% y-o-y decline to 98 mnt. In the third place, Shandong clocked a fall of 7% y-o-y to 58 mnt.

Only Guangdong logged minor growth, of 2% y-o-y to 33 mnt.

Factors influencing China’s crude steel output in Jan-Oct’25

Govt moves to curb “involution” in steel industry: Rumours swirled right from the beginning of the year that the Chinese government intended to mandate production cuts to manage the steel industry’s supply glut.

The prediction finally came true in the middle of the year, when China came out with an anti-involution campaign, aimed at curtailing aggressive, damaging price competition in the domestic steel industry, alongside some allied segments.

This served as a clear directive to steelmakers to maintain production discipline, though no definitive targets were specified.

Later, in September, the government released a steel industry action plan, which sought to halt fresh capacity additions and phase out outdated infrastructure.

Additionally, steelmakers were asked to complete their transition to ultra-low emission technologies by the end of 2025. An annual target of 4% growth in industrial value addition was also laid down, in line with a shift to manufacturing high-end steel products.

Accordingly, Baosteel, China’s largest steelmaker, slashed its production guidance (for its standalone operations) to over 80 mnt from the previous 80-100 mnt. This is applicable for the next five years, during which the focus will be on efficient utilisation of existing resources rather than capacity ramp-ups.

However, notably, while the government has repeatedly expressed an intention to reduce production, it has consistently shied away from providing a target figure.

Environmental concerns prompt production curbs: Local authorities in Hebei’s Tangshan, the major steelmaking hub in north China, have intermittently mandated production halts since August. On the surface, these aim to reduce air pollution in Beijing; however, they are also aligned with the government’s goals of curtailing overproduction, as evidenced by the crackdown taking place parallelly on indiscriminate coal mining.

To illustrate, during 27-31 October, local authorities asked mills to reduce blast furnace (BF) operations by 30%, impacting about 409,500 tonnes (t) of hot metal production, as per MySteel estimates.

Shrinking profit margins weigh on momentum: While more than half of Chinese steelmakers were able to secure healthy profits earlier this year (likely contributing to the government’s reluctance to mandate clear production cuts), the situation reversed by September-October. While raw material costs surged, steel prices remained weak in comparison, due to subdued demand and price resistance.

As such, profitability shrank, with Mysteel observing that by 30 October, only around 45% of the 247 BF-route steelmakers tracked could secure some profits on steel sales. This marked a decrease of 3 percentage points w-o-w and 16 percentage points y-o-y.

In comparison, in May, it was reported that about 56% of mills operated at a profit in April, up 3 percentage points m-o-m.

Property slump pressures steel demand: China’s prolonged real estate crisis continued to weigh on steel demand. Investment in infrastructure and real estate projects continues to wane, stalling upward momentum for construction steel demand.

Consequently, worldsteel projects a 2% decline in steel consumption in China, with the rate expected to decelerate to 1% in 2026 as the housing market bottoms out.

Outlook

2024 is likely to be last year with crude steel production surpassing 1 billion tonnes, with a Reuters report estimating the 2025 total at 970 mnt.

Meanwhile, the government is intensifying efforts to rationalise production capacity and restructure the industry for greater value addition.

For example, the government has advocated for tightening of capacity swap arrangements. It has proposed that older, decommissioned capacity be 1.5 times more than fresh additions.

The new plan also forbids any expansions in total steel capacity in regions such as the Beijing-Tianjin-Hebei area, the Yangtze River Delta, and the Fenwei Plain.

While exports have emerged as a crucial outlet for relieving domestic supply pressure, the momentum is unlikely to sustain for far long, especially beyond 2025. Global trade volatility and tariff tensions have led to frontloading of shipments, so overseas demand may weaken in the coming months. This will again exert pressure on mills production enthusiasm.

Leave a Reply