- HZL zinc price hike adds some cost pressure

- Auto sector recovery may support demand

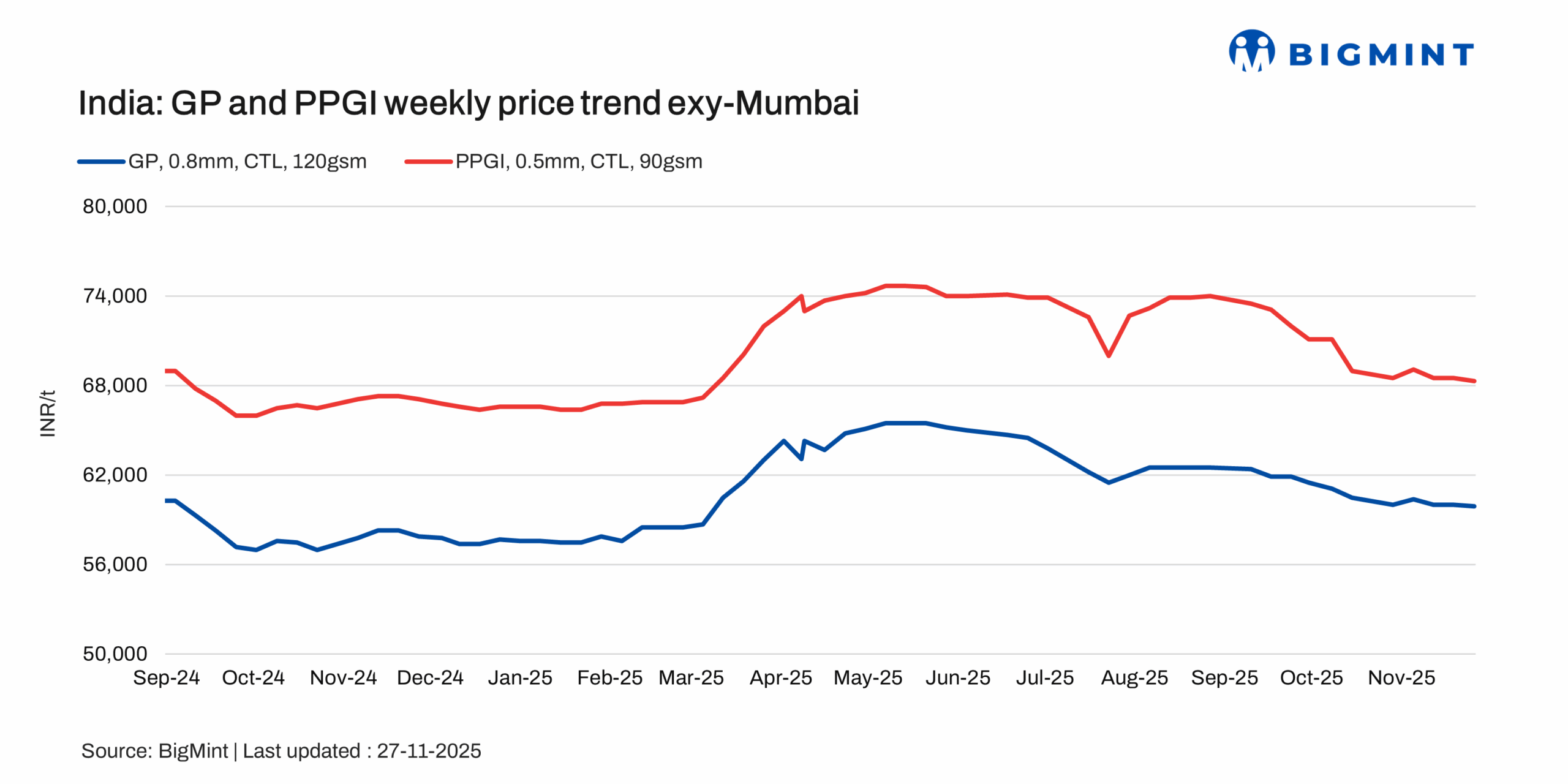

Indian coated flat steel prices declined w-o-w, with galvanised plain (GP), pre-painted galvanised iron (PPGI), and galvalume (BGL) coils all registering declines amid sluggish buying activity. Demand remains weak, and market participants continue to report absence of any concrete recovery signals. Overall sentiment stays dull, with buyers maintaining a wait-and-watch stance. The market is still awaiting clearer indications from mills regarding potential discounts, which has further contributed to the cautious mood and restrained transactions.

As per latest assessment on 27 November, GP coils (0.8 mm/CTL, 120 gsm, IS 277) were at INR 59,900/t ($670/t) ex-Mumbai, down INR 100/t w-o-w, with offers in the INR 59,500-60,500/t ($666-677/t) range.

Galvalume (0.5 mm/CTL, 1220 mm, AZ150, IS 15961) was assessed at INR 74,500/t ($833/t) ex-Mumbai, down INR 1,500/t w-o-w, with offers at INR 74,000-75,000/t ($828-839/t).

Meanwhile, PPGI (0.5 mm/CTL, 90 gsm, IS 14246) was assessed at INR 68,300/t ($764/t) ex-Mumbai, down INR 200/t w-o-w, with offers in the INR 68,000-69,000/t ($760-772/t) range. Prices are exclusive of 18% GST. (USD 1 = INR 0.011187; INR 1 = 89.3898 USD)

Market updates

Coated steel sentiment remained weak across regions, with buyers restricting purchases amid liquidity concerns and no clear pricing signals from mills.

- In the west, the market is expected to stay soft until mid-December, with hopes of stabilisation thereafter, although buyers await discount indications from mills.

- In the north, the market is likely to see improvement only after December, with mills expected to roll over prices and demand staying subdued but not alarming.

- In the south, weak end-user demand and minimal mill support continue to weigh on sentiment, and participants are watching closely to see if any recovery materialises.

Zinc price movement

HZL has raised zinc ingot prices by INR 2,400/t to INR 317,400/t in line with LME trends. However, domestic zinc fundamentals remain weak, with demand subdued and overall sentiment bearish. Import premiums offer only limited support.

Galvanisers, the main consumers of GP and BGL, are buying cautiously, with only a few large players active in the spot market, a Delhi-based distributor informed.

The zinc price hike may add minor cost pressure on coated steel producers, but weak demand means mills are unlikely to pass on the increase immediately, limiting the room for further discounts.

Auto sector impact

India’s improving automobile demand – across PVs, two-wheelers, three-wheelers and tractors – offers a positive medium-term cue for the coated flat steel market. Auto OEMs and ancillaries are key consumers of GP, PPGI and BGL for corrosion-resistant components and structural parts. While current coated steel demand remains weak, the steady rise in retail and wholesale vehicle sales suggests potential ordering support once automakers ramp up Q4–Q1 production. This recovery may help stabilise coated steel sentiment and limit further downside after December.

Outlook

Coated flat steel prices are likely to remain range-bound in the near term due to weak demand, cautious buyers, and limited discount signals from mills. The recent zinc price hike may add minor cost pressure, but soft domestic consumption prevents immediate pass-through. However, improving automobile sales and festive-driven production plans could provide gradual support, potentially stabilising GP, PPGI, and BGL prices after December.

Leave a Reply