- Pakistan and Bangladesh remain subdued with limited buying

- Turkiye scrap prices rise on stronger rebar demand

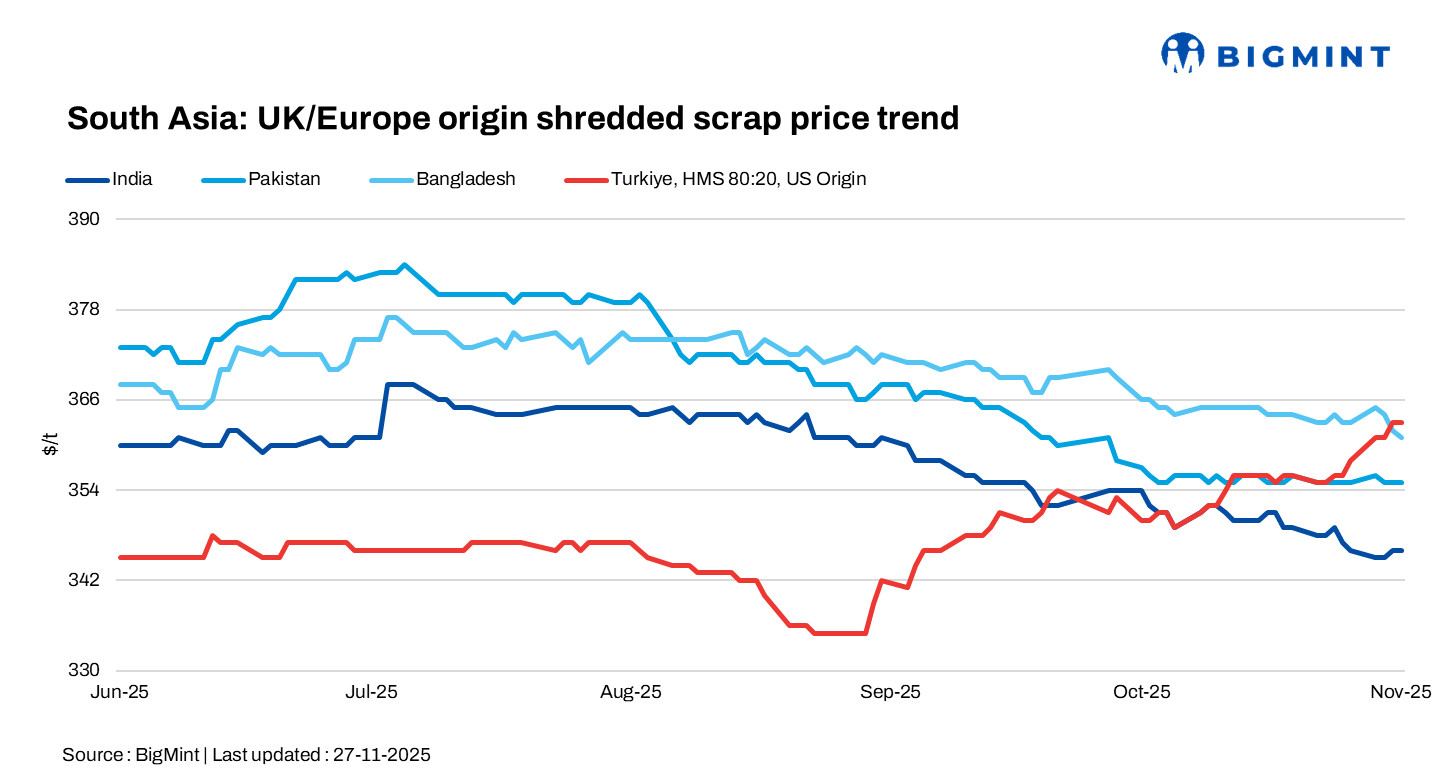

South Asian imported scrap markets stayed mixed on 27 Nov, with India showing mild improvement on steady inquiries, while Pakistan and Bangladesh remained subdued amid weak demand and limited buying interest.

India: Imported ferrous scrap market showed mild improvement d-o-d, supported by steady domestic inquiries and firmer offer levels. UK HMS was offered around 330/t CFR, shredded near 355/t, and busheling at 361/t CFR at western ports. Market sentiment improved after a leading stockist cleared nearly 25,000 t of arriving material in northern India at firm prices, indicating better liquidity and restocking interest.

Price indicators from recent market activity showed Brazil HMS between 325-340/t CFR depending on loading conditions, turning scrap around 302/t, and shredded scrap from New Zealand and Brazil at 347-352/t CFR. Busheling bundles were indicated near 357/t CFR, while HBI interest strengthened with parcels booked near 262/t CFR for next-month arrival. However, Overall momentum capped as strong Turkish buying draws supply, keeping India firm.

Pakistan: Imported scrap markets in Pakistan remained steady, though activity was limited as mill utilisation rates were expected to fall further with the onset of winter. European and UK-origin shredded scrap was assessed at $355/t CFR Qasim, while UAE-origin HMS continued to trade in the $335-340/t CFR range.

Bangladesh: Imported scrap markets in Bangladesh remained subdued as mills faced weak downstream demand and tight liquidity, but price indications continued to edge higher. Bulk offers into Chattogram have moved above $365/t CFR, and a 9,000-t PNS cargo from Singapore and Malaysia was recently concluded at $367/t CFR, reflecting firmer sentiment despite limited buying.

Turkiye: Deepsea import scrap prices remains stable on Nov. 27, supported by stronger downstream rebar demand. US HMS 80:20 traded at $362-364/t CFR, while EU-origin scrap was at $356-358/t. Improved vessel availability after the grain season, combined with firm freight rates, supported steady buying and contributed to higher prices over the past two weeks.

Leave a Reply