- Winter restocking continues despite weak steel margins

- Freight sentiment improves on tighter tonnage

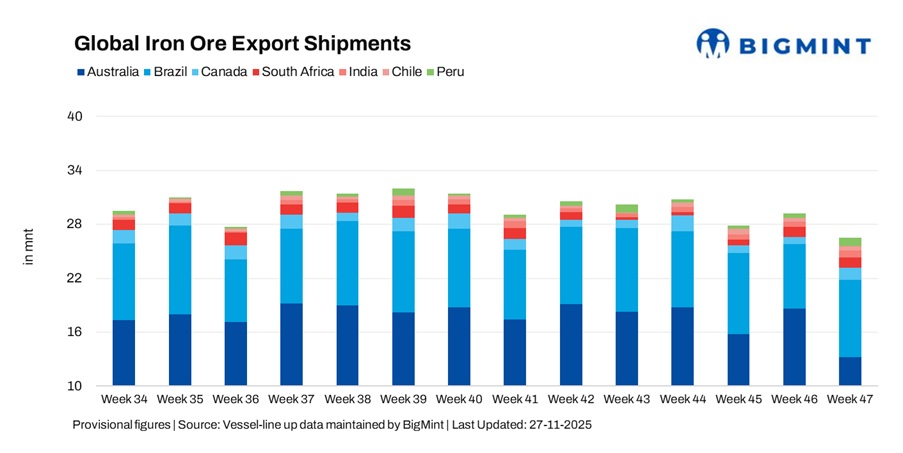

Global iron ore exports declined 10% w-o-w to 26.45 million tonnes (mnt) in week 47 (15-21 November) from 29.27 mnt in week 46, largely due to a significant contraction in Australian shipments. The fall outweighed solid rebounds from Brazil, Peru and Canada, which benefitted from improved weather conditions and smoother miner-to-port dispatches.

Despite lower global volumes, freight sentiment turned bullish as vessel availability tightened, winter restocking improved forward demand visibility and chartering momentum returned across basins, particularly for Capesize vessels.

Chinese buying remained steady but not aggressive, constrained by weak steel margins and high portside inventories. Miners continued to calibrate sailing schedules carefully amid the shifting freight landscape; while recovering freights supported long-haul suppliers with increasing demand signals, shorter-haul exporters such as Australia remained more cautious given reduced throughput and limited near-term loading opportunities.

Australian shipments fall sharply

Australia, the world’s leading iron ore exporter, saw exports decline sharply by 29% w-o-w to 13.18 mnt in week 47 from 18.62 mnt in week 46, marking one of the weakest weekly performances since September. The drop was primarily driven by reduced throughput across Pilbara ports, where slower berthing rotations, lighter scheduling cycles and subdued short-haul procurement from China weighed on loadings. Major ports contributed as follows: Hedland 6.4 mnt, Walcott 3.2 mnt and Dampier 2.9 mnt.

Despite improving freight momentum globally, Australia struggled to capitalise due to muted operational performance. BHP’s production outlook also remains uncertain, with stalled pricing talks with China’s state-owned CMRG raising the risk of product restrictions that could limit future growth. China continued to dominate demand, importing 11.2 mnt during the week. On the supply side, Rio Tinto led shipments with 6.1 mnt, followed by BHP at 4.3 mnt and FMG at 1.8 mnt.

Brazilian exports climb on port efficiency

Brazil’s iron ore exports rose 20% w-o-w to 8.60 mnt from 7.19 mnt, supported by better weather conditions and smoother loading cycles across key ports. The majority of loadings were handled by Ponta da Madeira at 3.6 mnt, while Tubarao and Itaguai shipped 1.8 mnt each. Renewed interest from Chinese buyers for medium to high-grade fines contributed to the momentum, reflecting improving forward procurement appetite as market sentiment strengthened.

Although demand remains sensitive to delivered pricing, Brazil continues to hold a structural advantage in supplying high-grade cargo, positioning the country to benefit from rising freight and improving inquiry levels. Shipments during the week were largely driven by major miners, with Vale exporting 4.3 mnt and CSN 3.6 mnt, underscoring strong operational performance amid recovering buying interest.

Canada sees strong weekly export recovery

Canada’s iron ore shipments surged 68% w-o-w to 1.36 mnt in week 47 from 0.81 mnt the previous week, reflecting a sharp rebound as earlier rail and port congestion eased. The increase was driven by higher cargo allocations to Europe and China, although the rise appears to be more of an operational catch-up than a broad improvement in demand. The Netherlands, China and Bahrain were the leading importers during the week, each taking 0.2 mnt.

Sept-Iles dominated loadings at 1.2 mnt, followed by Port Cartier at 0.1 mnt. On the supply side, Guinea and Nimba mines contributed 0.7 mnt, while IOC accounted for 0.4 mnt of total volumes.

South Africa maintains steady momentum

South Africa’s iron ore exports inched up 2% w-o-w to 1.10 mnt in week 47 from 1.08 mnt, supported by sustained rail-to-port stability and smoother operations at key terminals. Shipments were largely handled through Saldanha Bay at 0.9 mnt, complemented by 0.2 mnt from Richards Bay. The steady improvement aligns with Kumba Iron Ore’s recent rise in quarterly sales volumes, driven by better freight rail performance made possible through collaborative efforts between bulk mineral producers and state-owned logistics firm Transnet to restore the ore export corridor.

Despite the stable performance, lingering uncertainty over long-term infrastructure reliability continues to cap the potential for stronger weekly gains. On the demand front, Slovenia and China emerged as the main importers, each securing 0.2 mnt during the week.

India maintains export momentum

India’s iron ore exports surged 26% w-o-w to 0.78 mnt in week 47, up from 0.62 mnt in week 46. The rise was driven by strong Chinese demand for low-grade fines and smoother loading operations across major ports. Paradip led the shipments with 0.4 mnt, followed by Mormugao at 0.2 mnt, while steady demand for small and mid-sized vessels supported efficient scheduling.

Although high-grade ore availability remained limited, India sustained robust export momentum thanks to consistent interest from cost-sensitive buyers. China continued to dominate as the primary destination, importing 0.3 mnt of Indian iron ore during the week.

Chile, Peru see strong weekly iron ore gains

Chile’s exports rose 24% w-o-w to 0.50 mnt, supported by improved loading cadence and steady demand from the Middle East and China. Totoralillo handled 0.4 mnt and Huasco shipped 0.1 mnt, reflecting stable operations across both terminals. China remained the dominant buyer, importing 0.4 mnt during the week, while consistent inquiries for low- to mid-grade ores kept export momentum firm.

Peru posted one of the strongest recoveries of the week, with exports surging 71% w-o-w to 0.93 mnt, driven by uninterrupted dispatches from Shougang Hierro amid robust Chinese appetite for medium-grade ore. San Nicolás managed 0.9 mnt and Matarani handled 0.1 mnt, marking a sharp rebound in operational efficiency after prior weeks of irregular scheduling. China imported 0.9 mnt, absorbing nearly the entire weekly output and reinforcing its dominant pull-on Peruvian supply.

Tighter tonnage and winter restocking lift iron ore freight

Iron ore freight markets firmed across major dry bulk routes in week 47, supported by improved chartering activity, tighter vessel availability, and stronger cargo inquiry. While Chinese buying remained steady rather than aggressive, restocking ahead of the winter season boosted forward demand visibility and encouraged charterers to return to the market. Rising Baltic index levels and forward freight agreements reflected growing confidence in both the Atlantic and Pacific, while Supramax earnings stayed constructive due to resilient minor bulk activity.

Easing bunker costs also provided relief to shipowners, particularly on long-haul voyages. Strengthening freight trends are expected to support shipments from Brazil, India, and Peru in the coming weeks, though high rates and softer operational activity may continue to limit upside for Australian exporters.

Outlook

Global iron ore exports are expected to stabilise toward late November, supported by the recovery in Brazil, Canada and Peru, along with steady momentum from India and consistent port activity in South Africa. Stronger freight sentiment may encourage miners to speed up shipments, but Australia remains the major swing factor – any rebound in Pilbara loadings will largely determine the overall export trend.

Looking ahead, supply is set to increase as new capacity comes online, including the Simandou project in West Africa and expansions in Australia and Brazil. Sierra Leone and Liberia are also expected to add volumes as their projects progress. However, growth may be slower than expected due to weather risks, geopolitics and rising costs, while China’s shift toward higher-quality steel over higher volumes could gradually reduce demand.

Leave a Reply