- Short-term volatility persists in Nigeria and Togo

- Seasonal harvest inflows continue to ease regional prices

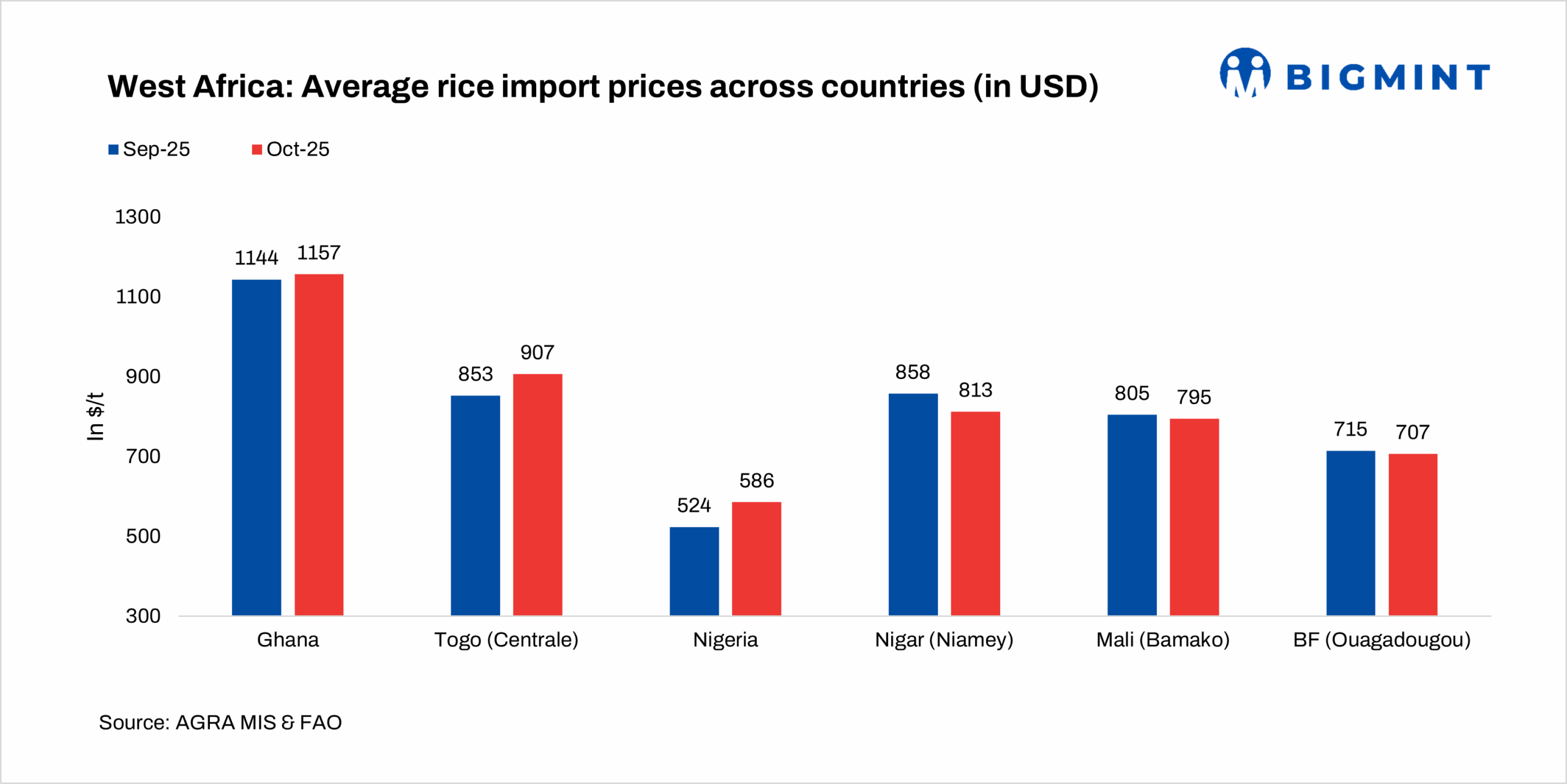

Rice markets across West Africa moved unevenly between September and October, with short-term volatility offset by broader seasonal softening. Ghana registered the region’s highest wholesale prices, rising 3.9% to $1,157/t as of October 2025 as local quotations were boosed by appreciation of the Ghanaian cedi. Prices in Togo’s Centrale market also firmed, gaining 6.3% to $907/t on localised supply constraints.

Nigeria registered the steepest increase, up 11.8% to $586/t, underscoring persistent structural shortages despite government interventions and strong consumer demand. Meanwhile, prices eased across the Sahel. Prices in Niger’s Niamey dropped 5.2% to $813/t, while prices at Bamako in Mali slipped 1.2%. Prices at Ouagadougou in Burkina Faso fell from $715/t to $707/t as early harvest inflows improved availability.

Short-term fluctuations set against broader declines

Despite scattered monthly swings, three- and six-month trends show clear softening across most markets. Burkina Faso remained steady month-on-month but recorded medium-term declines of up to 19.6%, with Bobo Dioulasso still slightly above last year’s levels at over 1.19%.

Ghana saw an 8.85% monthly drop to GHS 12,546.88/t, driven by improved domestic supply and buffer-stock releases. Mali’s markets remained broadly stable, with only marginal monthly adjustments Mopti rose 2.08% but continued to show sharp long-term declines, including -25.29% year-on-year.

Divergent national trends underline uneven market conditions

Niger’s markets showed mixed monthly movements, led by a 7.69% decline in Niamey, though all major markets posted annual drops of up to 25.81%. Nigeria stood out with a 15.43% monthly surge to NGN 848.97/kg, even as longer-term comparisons continued to soften, suggesting recent policy changes have yet to filter fully through supply chains.

Togo recorded the most pronounced volatility, with Centrale up 8.37%, Maritime jumping 19.20%, and Savanes rising 16.81%. These spikes contrasted with quarterly and annual declines of up to 35.14%, reflecting temporary disruptions amid ongoing harvest flows.

Outlook

Long-term trends point to continued easing supported by harvest arrivals and improved domestic supply, though Nigeria and Togo highlight pockets of short-term pressure. Market analysts expect further moderation as more paddy enters the pipeline, though the adjustment will remain uneven across national markets.

Leave a Reply