- OMC auction sees active response

- High-grade ore shortage supports prices

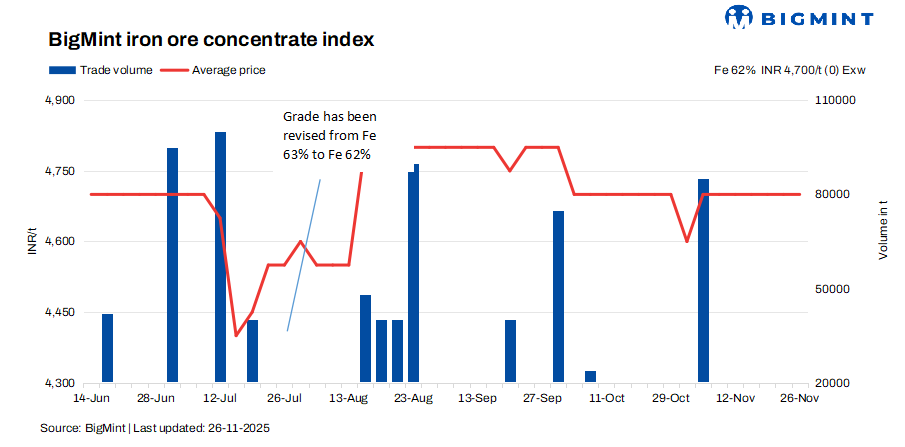

BigMint’s bi-weekly assessment for India’s iron ore concentrate (Fe 62%) remained unchanged at INR 4,700/tonne ($53/t) ex-works Jabalpur on 26 November, mirroring the previous evaluation on 22 November. Market participants noted that trade volumes stayed moderate, as most sellers had already booked sufficient quantities limiting additional offers in the market.

Meanwhile, Fe 63% concentrate was heard quoted at INR 5,000/t ($58/t) exw. A pronounced shortage of high-grade material across regions has further strengthened market sentiment, providing strong support to high-grade concentrate prices. Sellers, backed by tightening availability, are maintaining their offers with increased confidence keeping premiums intact.

A Jabalpur-based seller told BigMint, “Our offers remain exactly where they are. We’ll think about revising them only after the large stack of pending orders is cleared. Demand is comfortably high, so there’s no pressure on us to adjust anything yet.”

Market participants continued to express a supportive outlook anticipating a seasonal upswing in demand as winter approaches a period traditionally known for peak construction activity and the acceleration of major government-backed infrastructure projects. Historically, winter has been the strongest demand phase for steel, and many believe this momentum will once again lift the iron ore market.

However, they also acknowledged that demand this season has not yet reached the robust levels seen in previous years. Despite this slower-than-usual start, sentiment remains firmly optimistic, with traders and buyers expecting a noticeable pickup in consumption in the coming weeks as project execution intensifies and steel requirements begin to escalate.

Rationale

- Zero (0) trade was recorded in this publishing window and was not taken into consideration, receiving a 0% weightage.

- Eight (8) offers and indicative prices were heard, and six (6) were taken into consideration as T2 trades, receiving 100% weightage.

Factors supporting prices

- Pellet prices remain firm in Raipur: PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, inched down by INR 50/t ($1/t) to INR 9,650/t ($109/t) DAP on 25 November 2025 compared to the previous assessment on 21 November. According to market participants, trading activity stayed muted amid weak underlying fundamentals. Persistent pressure on sponge iron and semi-finished steel prices has continued to dampen buyer sentiment, keeping many purchasers on the sidelines. As a result, pellet bookings saw limited traction, with buyers adopting a cautious approach and refraining from aggressive procurement.

- Odisha iron ore prices edge up w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index increased by INR 100/t w-o-w to INR 5,600/t ($63/t) ex-mines on 22 November. Iron ore prices in Odisha strengthened by INR 100-200/t following the latest Odisha Mining Corporation (OMC) auction, driven by strong bidding enthusiasm and tightening availability in the spot market. Despite this upward momentum, most miners have yet to release revised offers for fresh trades. This has kept buyers largely in a wait-and-watch stance, anticipating clearer pricing signals before stepping back into the market.

- OMC bids rise m-o-m: In OMC’s auction on 19 November, 1 mnt of iron ore lumps (Fe 60-65%) were booked at INR 6,000-8,750/t, with premiums of INR 700-1,700/t and select lots touching INR 2,000-2,700/t, pushing weighted average bids up by INR 250/t m-o-m despite an INR 200/t cut in base prices. Similarly, in the fines auction for 1.939 mnt (Fe 51-62%), nearly 99% of the material was booked at INR 2,500-5,900/t, attracting premiums of INR 50-1,000/t and a marginal INR 200/t m-o-m rise in weighted average bids, supported by limited supply and minimal offers from private miners.

Outlook

Iron ore concentrate prices are expected to remain supported in the near term on tight material availability, steady pellet prices, and the seasonal pickup in steel demand. While improving construction and government project activity may lend support, limited spot trades and cautious buying sentiment could cap any sharp increase.

Leave a Reply