- Drop in European gas prices makes coal unviable

- Asian growth opening demand avenues for low-CV coal

A stark divergence is appearing in the global seaborne thermal coal market, cleaving it into two distinct worlds: one where premium high-calorific value (CV) coal is faltering under weak demand, and another where lower-quality coal is being buoyed by insatiable appetite from price-sensitive buyers in India and Southeast Asia.

High-CV coal: Atlantic weakness infects Asia

The premium end of the market is under clear pressure. In Europe, the benchmark DES ARA (Northwest Europe) coal price has retreated to $95.20/t, as a collapse in natural gas prices below €30/MWh has rendered coal-fired power generation less economical. This Atlantic weakness has flowed through to financial markets, where the Q1 2026 DES ARA contract has slipped to $97.50/t.

The malaise has spread to the Pacific basin’s high-grade suppliers. Australian NEWC 6000 NAR coal, a traditional benchmark, is assessed at $110/t, but market participants report a lack of buying interest and a growing gap between bids and offers. The weakness is even more pronounced in the high-ash segment; Australian 5500 NAR coal is seeing trades as low as $87/t FOB, with bids for January-loading cargoes dipping to $88/t against seller offers above $90.

“The high-CV market is looking for a floor,” said a Singapore-based trader. “With European gas in the doldrums and Chinese buyers resisting high prices, there’s just no catalyst for a rally. We’re seeing the physical market replicate the bearishness in the financial paper.”

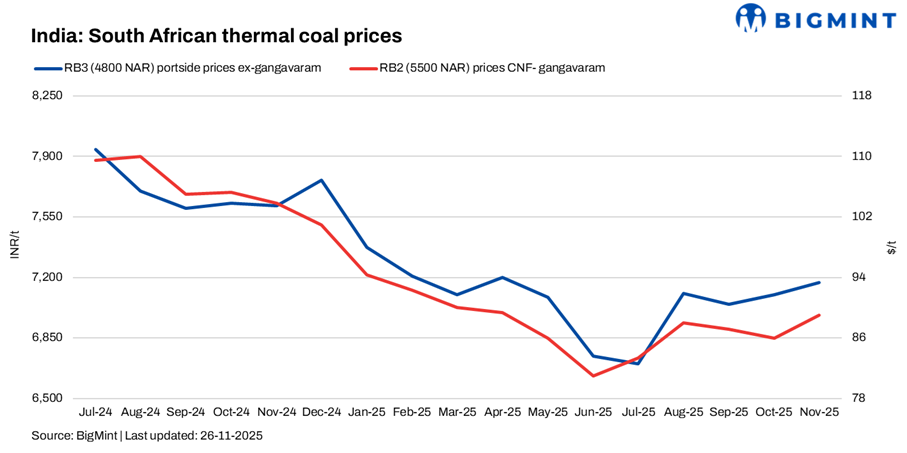

India fuels low/mid-CV demand

In stark contrast, the market for lower-energy coal remains remarkably resilient, thanks almost entirely to steadfast Indian demand. Indonesian 4200 GAR coal, the workhorse fuel for many Indian power plants and industrial users, is holding firm at $51.50-$52.00/t FOB. Despite a slight softening from the previous week, traders report consistent demand that provides a solid price floor.

The reason is simple economics: on a value-in-use basis, Indonesian 4200 GAR remains the most cost-effective origin for Indian buyers, with delivered costs calculated in a stable range of INR 1,440-1,480 per Gcal. This has created a steady, high-volume trade corridor that insulates the segment from volatility elsewhere.

Gcal. This has created a steady, high-volume trade corridor that insulates the segment from volatility elsewhere.

South African coal, a key mid-CV supplier, is also finding support. While the FOB Richards Bay 6000 NAR price is at $86-90/t, the 5500 NAR grade is stable at $74-75/t, supported by tenders from South Korea and Japan, as well as steady Indian offtake.

Notably, Indian portside South African thermal coal prices remained unchanged w-o-w, with RB2 at INR 8,400/t ex-Paradip, INR 8,350/t at Vizag, and INR 8,400/t at Gangavaram. Market sentiment remained stable, supported by firm offers for January-February bookings, which continued to reflect steady interest in South African material.

A market of two halves

This “split personality” underscores a broader realignment in global energy. The energy transition in Europe, accelerated by record wind power generation and cheap gas, is systematically eroding the demand for high-quality thermal coal. Simultaneously, the relentless growth and industrialization of developing Asia, is providing a durable, long-term floor for the lower-quality segments that European utilities no longer desire.

Leave a Reply