- IF rebar market weakens after strong start early last week

- HRC trade prices continue to decline on high inventories

- Outlook gloomy for Q4CY’25 amid global steel market downtrend

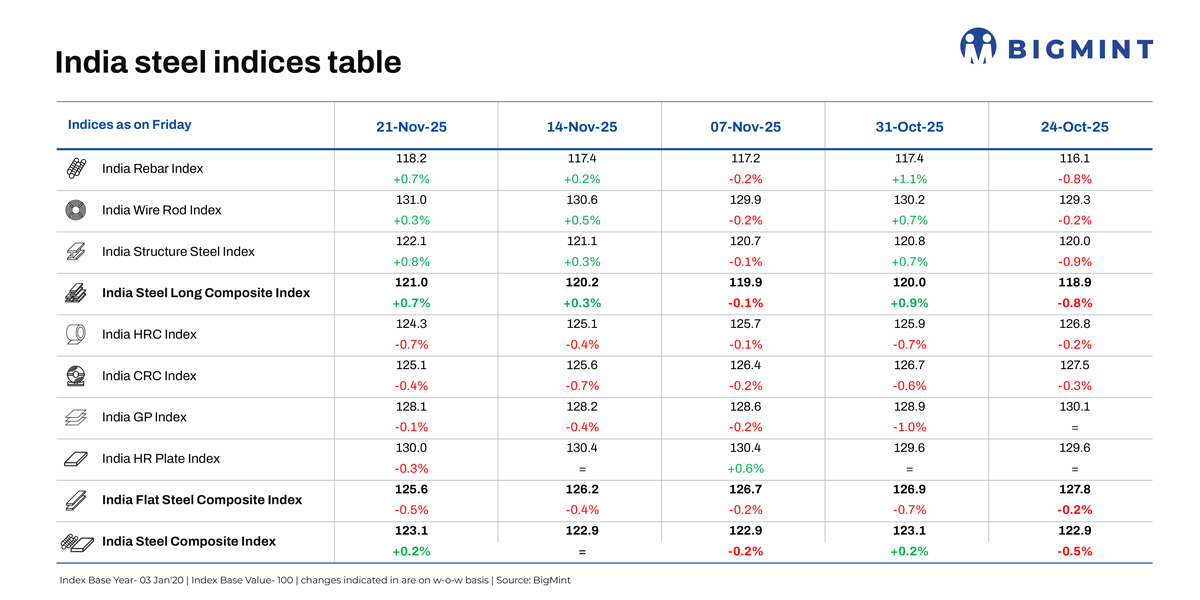

Morning Brief: BigMint’s India steel composite index, a barometer of steel market movements in the country, recorded marginal growth of 0.2% w-o-w, as assessed last on 21 November 2025, although steel prices in different regions of the country remained under pressure.

Any real improvement in market conditions is not yet discernible after an anticipated post-festive improvement in prices failed to materialise and hikes by the primary mills were ill-absorbed by trade market participants. The expected surge in activity in the traditional steel-consuming sectors such as infra and construction after the festive period, and before the January-March peak season, has failed to lift steel market sentiments. Similarly, the impact of landmark policy decisions on the steel market (like GST rationalisation in the auto sector) has been underwhelming thus far.

The longs index edged up by 0.7% w-o-w on improved activity in the IF finished steel segment seen early last week, although the momentum petered out by weekend. The flats index continued to edge lower, shedding 0.5% w-o-w after a 0.4% drop during the week before last as global sentiments continued to remain subdued and higher domestic supplies weighed on prices.

Highlights of price movements

Rebar prices weaken as momentum flags: Induction furnace (IF) rebar prices witnessed an uptick in the range of INR 200-1,200/t across regions, as per BigMint assessment. In the initial days of the week, sellers saw moderate bookings supported by firm sponge iron and billet prices. But, as prices increased, buying activity weakened, with buyers avoiding bulk purchases at higher price levels. Many manufacturers focused on dispatching previous orders, indicating some pressure to clear earlier commitments. Inventory levels across regions remain at around 10-15 days.

BF rebar prices fell w-o-w across markets on 21 November amid subdued demand. Mills offered price support or slashed list prices due to weak market activity. Trade-level BF rebar prices dropped by INR 700/t ($8/t) w-o-w to INR 46,600/t ($525/t) exy-Mumbai.

This new low was reached after list price hikes by some mills were not absorbed by the market. High inventories and production levels, liquidity shortfall, and need-based purchases forced manufacturers to slash list prices or offer price support.

Flats continue weak streak: BigMint’s benchmark bi-weekly assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 500/t ($6/t) w-o-w to INR 46,500/t ($526/t) on 18 November against INR 47,000 ($532/t) on 11 November. CRC (IS513, Gr O, 0.9 mm/CTL) prices decreased by INR 300/t ($3/t) w-o-w to INR 54,800/t ($620/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

The domestic HRC market remained weak on poor demand and higher material availability. A market participant informed: “Mills and distributors are actively pushing sales as inventories are moderate to high, but liquidity constraints are limiting purchases.”

While end-users’ offtake remains moderate, stock levels at distributors and company yards are elevated, keeping market sentiment dull.

Outlook

BigMint’s assessment for Indian HRC (S275) exports to the EU declined by $10/t w-o-w on 18 November, while the HRC (SAE 1006) export index for the Middle East dropped by $5/t w-o-w to $475/t FOB. Wilting global prices and a weak production scenario in China, as well as other major geographies, have had an adverse impact on Indian domestic and export prices of steel. This trend looks likely to continue throughout Q4CY’25.

Moreover, the government’s decision to temporarily suspend BIS norms for imports of a range of key steel products will, doubtless, mitigate any possibility of supply tightness in the downstream segments and consequent price hikes.

However, raw materials prices remain firm: domestic iron ore prices have edged up on positive trends seen in latest domestic auctions. Coking coal prices have increased slightly tracking global supply-demand dynamics. This will impact the margins of the primary producers. Therefore, some form of rationalisation of production in certain segments is to be expected.

Leave a Reply