- Codelco lifts CY’26 premiums to $330/t, up 288% y-o-y

- Copper softens w-o-w after mild $150/t correction on LME

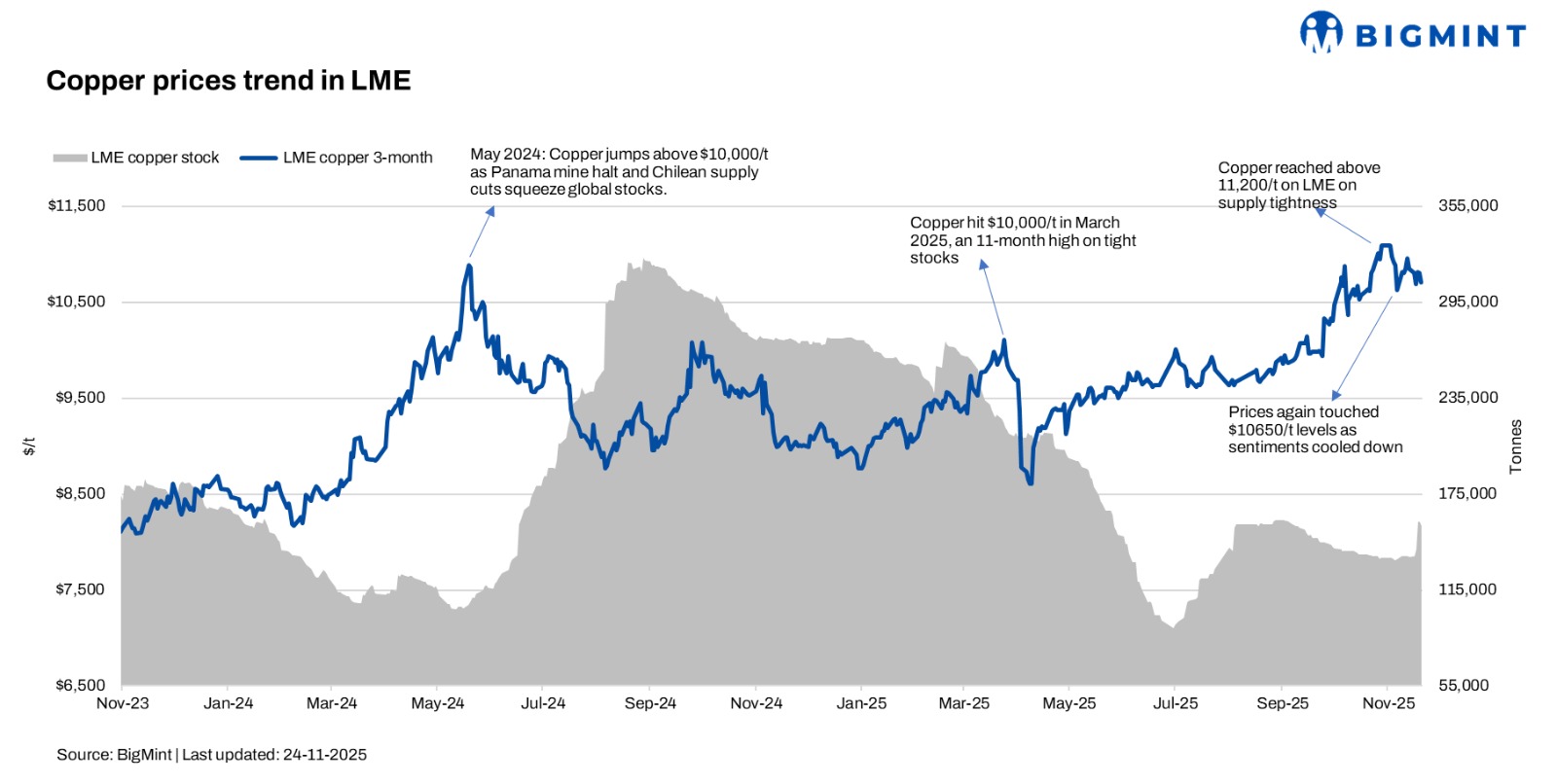

LME copper traded slightly weaker this week as the market responded to softer risk appetite and a visible increase in available inventories. Prices slipped from approximately $10,850/t on 14 November 2025 to nearly $10,700/t on 21 November, marking a mild w-o-w decline. The broader tone remained steady, but market participants leaned towards cautious positioning, reflecting a sentiment shift rather than a structural change.

LME warehouse stocks rose notably through the week, moving from ~135,000 t to about ~155,000 t, signalling better metal availability in the near term. This inventory build was the primary driver behind the week’s mild correction, as traders interpreted the increase as easing tightness in the short-term physical market.

Codelco hikes annual premiums

A major development influencing market sentiment came from the producer side. Codelco, the world’s largest copper miner, announced sharply higher annual premiums for its 2026 contracts. For Korean customers, Codelco set its premium at $330/t, representing a massive +288% increase from last year’s level. This aggressive upward revision demonstrates the miner’s confidence in long-term demand and reflects the company’s strategy to lock in higher margins amid expectations of a tighter refined copper balance ahead. Despite the week’s softer LME prices, such a premium jump signals that structural scarcity concerns continue to shape the physical market outlook.

This news also influenced traders’ sentiment on the forward curve. While spot prices softened due to inventory movements, the strong premium signals from Codelco reignited debates around 2026–2027 tightening, driven by delayed mine expansions, falling ore grades, and increasingly cost-heavy smelting conditions. Physical buyers—especially in Asia—interpreted this as a sign that long-term supply contracts may become significantly more expensive, prompting some to pre-emptively reassess procurement strategies even though immediate demand remains stable.

Looking ahead, the copper market appears firmly positioned, with near-term softness counterbalanced by medium-term structural tightness. Unless another surge in inventories emerges, LME copper is likely to remain range-bound between $10,600/t and $10,900/t in the short term. However, rising premiums and producer behaviour indicate that any deeper dips may increasingly be met with strategic restocking, particularly as the market approaches year-end contracting cycles.

Leave a Reply