- Iranian domestic prices edge up; export deals stay discounted

- Chinese domestic prices hold steady on firm raw material costs

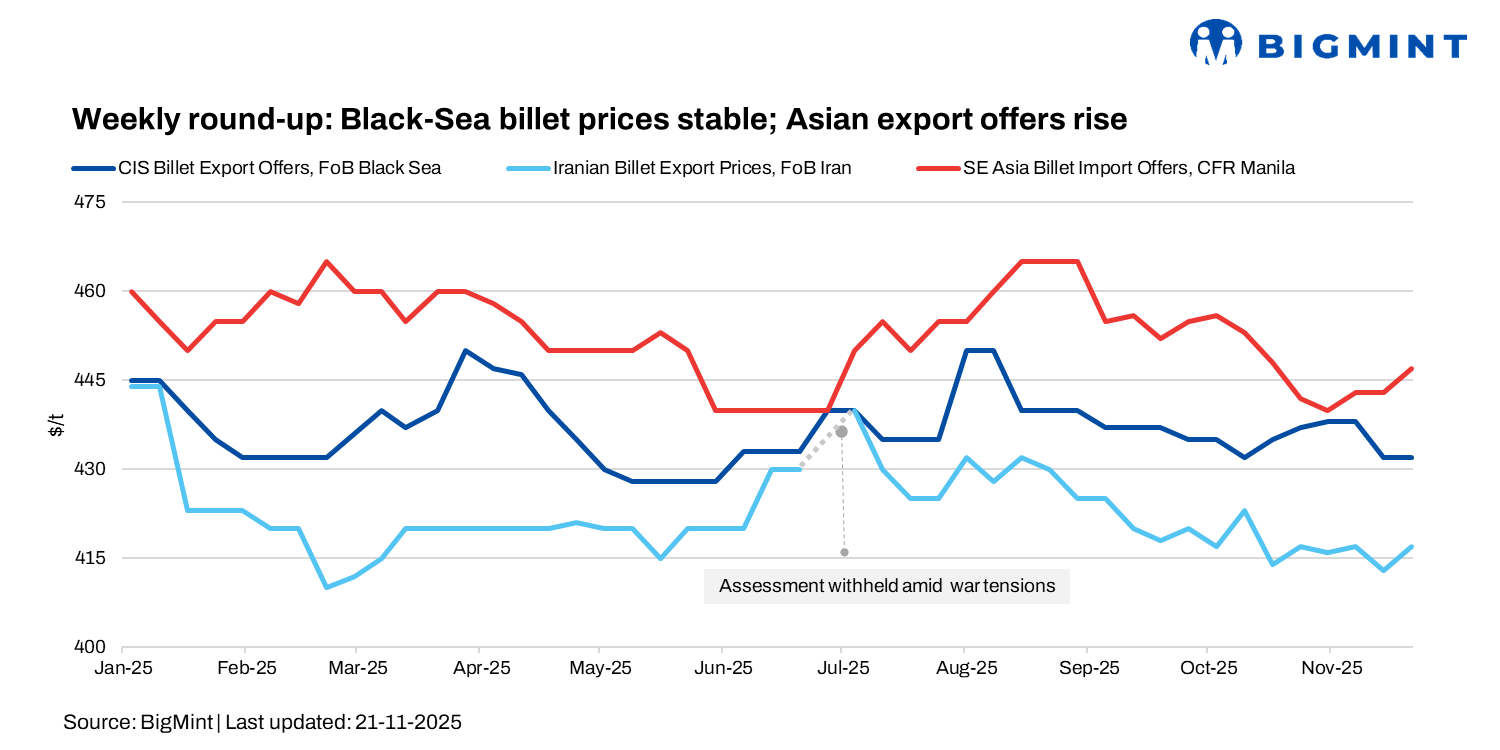

Global billet and scrap markets firmed up in week 47 (17-22 November), led by Asia. Chinese 3sp billet offers rose by $4-5/t to $435-438/t FOB amid production cut expectations, though buyers stayed near $430/t, widening the bid-offer gap. Black Sea billet prices hold steady w-o-w; domestic prices in Iran increased.

Turkiye’s deep-sea scrap market also strengthened, with US-origin HMS 80:20 trading around $360/t CFR and late-week offers exceeding $362/t CFR as rebar gained traction.

Around 8-10 cargoes were booked at $354-361/t, keeping the scrap-rebar spread steady at $200-205/t. Higher winter collection costs provided support, while Turkish rebar offers firmed to $555-560/t FOB.

Black Sea market

Russian mills kept offers for December-January shipment at $435-440/t FOB Black Sea, stable as compared to the last week. Russian producers reduced their exports of square billets in October. The decline affected the Asian and Middle Eastern markets.

Asian billet market

Asian billet prices have firmed since early November, supported by expectations of production cuts in China. Buyers in Southeast Asia remained cautious due to weak long steel demand and competitive Iranian offers.

China

Chinese billet and rebar prices were largely stable over the week, with domestic billet at RMB 2,950/t ($415/t) and SHFE January 2026 rebar at RMB 3,057/t ($430/t). Early-week gains were supported by firm iron ore and coke costs and tighter hot metal output. Mid-week, sentiment softened amid weak winter demand, environmental inspections, and limited policy support. By the weekend, prices remained steady, with export rates easing $1‑2/t on competitive pressures, while mill margins stayed near one-year lows, reflecting a market balancing cost-driven support against subdued buying.

Chinese 3sp semis were offered at $435-438/t FOB for December-January shipments, up from $430-432/t a week ago, amid anticipated winter production restrictions from environmental inspections in Beijing, Tianjin, and Hebei. Traders tried selling Chinese 3sp billets to Sutheast Asia at $450/t CFR, but bids lagged at $435-440/t, creating a $10-15/t gap.

SE Asia

Indonesian buyers sought Iranian 5sp semis at $430/t CFR, with offers at $444-448/t CFR, citing limited rebar demand and projects still in planning. In the Philippines, the Chinese 3sp billet offers stood at $450/t CFR, with bids near $440/t, while previous deals were heard at $445/t CFR for Iranian and $440/t CFR for Chinese 3sp billets.

Middle East

Saudi Arabia: In Saudi Arabia, rebar prices remained flexible as mills focused on clearing inventories and maintaining cash flow. Buyers responded to adjusted offers, while improved finished steel activity lifted sentiment and supported scrap price increases.

Rebar offers were clustered between SAR 1,900-2,080/t ($507-556/t) across Saudi mills. First-tier mills offered material at SAR 2,040-2,080/t, second-tier at around SAR 2,000/t, and smaller mills at SAR 1,900-1,920/t. To keep volumes moving, many mills trimmed prices by SAR 20-40/t ($5-10/t).

Despite a slightly better offtake, mills stated that revenue gains remained limited due to tight liquidity and intense competition. Scrap prices strengthened by SAR 10-15/t ($3-4/t) to SAR 1,400-1,410/t ($373-376/t) in Jeddah, Riyadh, and Dammam, with supply remaining adequate.

Iran: Domestic billet prices inched up from 356,000 rial/kg ($846/t) on 12 November to 364,500 rial/kg ($866/t) on 19 November, while rebar rose from 422,000 rial/kg ($1,003/t) to 430,000 rial/kg ($1,022/t). Early-week gains were driven by strong domestic demand and limited supply, though later in the week, soft global prices and cash-only sales tempered further increases. Mills remained cautious, balancing tighter allocations, currency uncertainty, and emerging gas shortages, with some volumes being redirected to the domestic market.

On the export side, the market felt the pinch of regulatory changes. Semis offers remained wide, with key mills targeting $415-420/t FOB, yet most deals were closed at $405-410/t, while smaller domestic channels transacted at $390-395/t.

A major Iranian mill sold billets at $417/t, considered high by many, while others were in the process of closing tenders for 30,000 t each later this month, with shipments scheduled for early January and end-December, respectively.

Industry participants are closely watching how export restrictions, licensing challenges, and global demand will shape near-term pricing, making cautious buying and selling the prevailing sentiment.

Leave a Reply