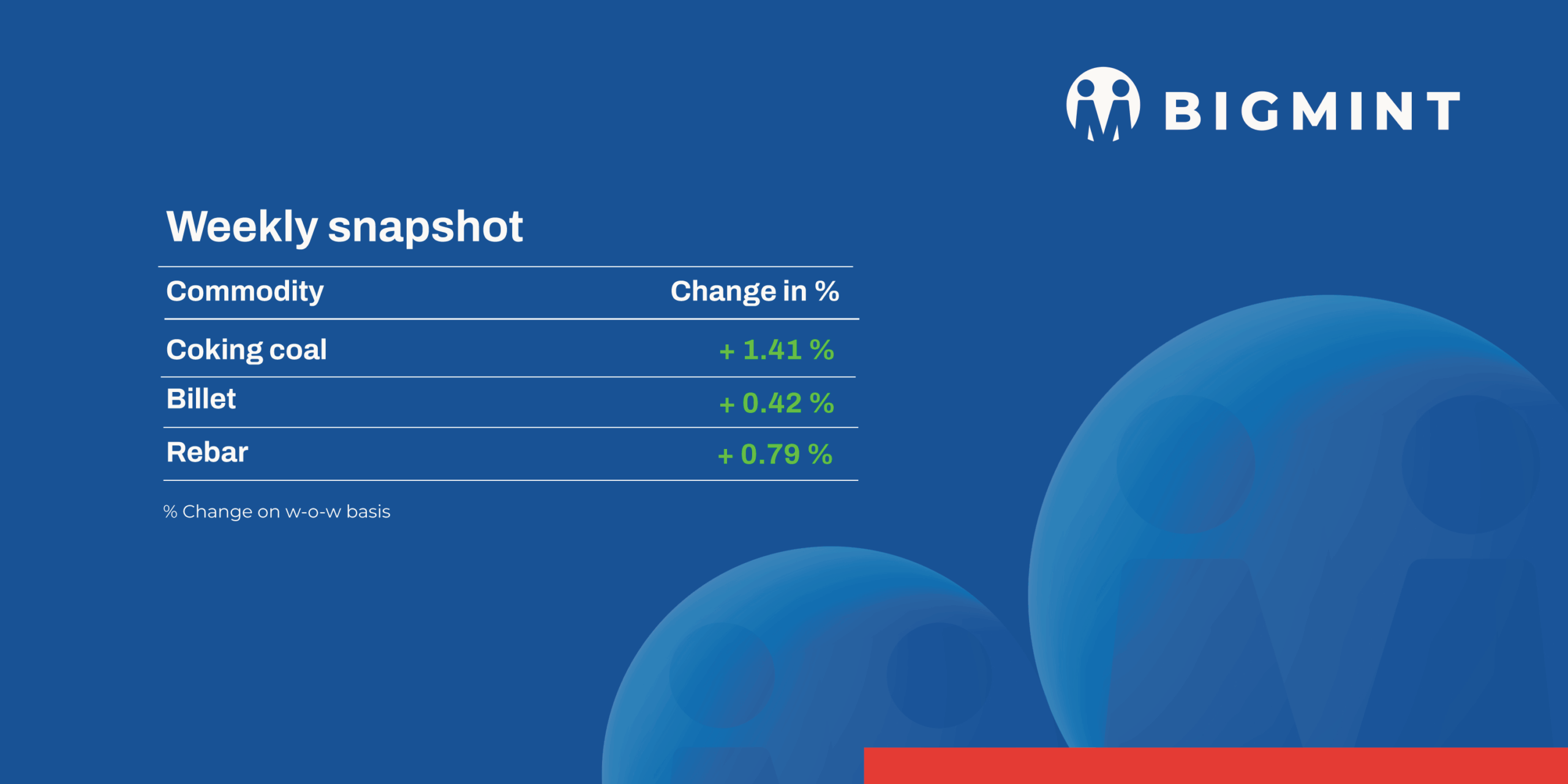

- BigMint’s coking coal index rises $6/t w-o-w

- Domestic billet prices up INR 600-1,000/t across regions

The domestic steel and raw materials market showed mixed movements during week 47 (17–22 November 2025). Iron ore and pellet prices strengthened on strong auction premiums, while scrap softened and flat steel remained weak amid subdued demand. Billet and IF rebar recorded slight gains.

Iron ore and pellet

In OMC’s auction on 19 November, 1 mnt of iron ore lumps (Fe 60–65%) was booked at INR 6,000–8,750/t, with premiums of INR 700–1,700/t and select lots touching INR 2,000–2,700/t, pushing weighted average bids up by INR 250/t m-o-m despite a INR 200/t cut in base prices. Similarly, in the fines auction for 1.939 mnt (Fe 51–62%), nearly 99% of the material was booked at INR 2,500–5,900/t, attracting premiums of INR 50–1,000/t and a marginal INR 200/t m-o-m rise in weighted average bids, supported by limited supply and minimal offers from private miners.

In NMDC;s Chhattisgarh auction on 20 November, 12,900-t DRCLO (10-40 mm, Fe 67%, base INR 6,300/t) and 4,000-t lumps (10-20 mm, Fe 65.5%, base INR 5,750/t) were sold at 15% and 17.5% premiums, respectively. Of 43,000-t fines (Fe 64%), 8,600 t were sold at base price INR 4,790/t. 21,200-t ROM (10-150 mm, Fe 65.5%) booked at INR 5,500/t. Prices were on FOR basis, including royalty, DMF, & NMEDT.

BigMint’s bi-weekly export index for Indian low-grade iron ore fines (Fe 57%) increased by $1.5/t w-o-w to $69/t FOB east coast on 20 November, supported by around 500,000 t of December-laycan export deals. Prices held largely firm amid improved seaborne trading activity, with buyers showing interest at slightly softer levels.

Coal

South African thermal coal prices at Indian ports remained firm w-o-w, with RB2 at INR 8,400/t ex-Paradip, stable at INR 8,350/t in Vizag and INR 8,400/t in Gangavaram, while RB3 stayed flat across the east coast. Limited availability and firm Asian demand were expected to keep offers elevated through early 2026.

Domestic coal prices remained stable w-o-w, with 5,000 GCV at INR 6,350/t and 4,500 GCV at INR 5,250/t ex-Bilaspur. In the latest SECL auction, 98% of the 1.078 mnt offered was booked, reflecting strong participation as traders continued operating on low inventories. Auction-based offer changes were expected once deliveries began. SECL started releasing larger quantities ahead of winter demand supporting steady market sentiment despite muted industrial offtake.

India’s met coke market showed mixed movement, with eastern prices edging up while western levels stayed steady. BF-grade met coke stood at INR 31,800/t ex-Jajpur, up INR 300/t w-o-w, whereas Gandhidham remained stable at INR 30,000/t. Foundry-grade met coke firmed to INR 36,000/t ex-Rajkot. Market sentiment in the east stayed optimistic, supported by DGTR’s preliminary findings confirming dumping of LAM coke from six countries.

BigMint’s premium hard coking coal (PHCC) index was assessed at $219/tonne (t) CNF Paradip as of 21 November, marking a $6 rise w-o-w. No trades were recorded in India during the week, while deal activity was observed in the Chinese market.

Ferrous scrap

Imported scrap sentiment in India softened through the week despite a brief lift from small deals such as Kuwait PNS at $340/t and West African HMS at $330/t. Weak construction activity and sluggish finished steel sales kept mills cautious, reducing bookings and increasing reliance on domestic scrap while targeting January arrivals.

Shredded scrap lost ground as mills resisted paying premiums above $20/t over HMS. Shredded traded at $340-350/t CFR Nhava Sheva with bids slipping to $340-345/t and offers down to 350-355, while HMS targets fell to $320/t CFR, widening the bid-offer gap.

In the last seven days a total of 8,000-9,000 t of imported scrap was booked into India at $305-353/t CFR, including 5,000-6,000 t of HMS 80:20 at $312-330/t CFR and remaining include PNS, turning and boring, LMS bundles, and NTP.

Ferro alloys

Silico manganese

Indian silico manganese (60-14) prices eased by INR 900/t ($10/t) w-o-w to INR 70,200–70,800/t ($783–790/t) across Durgapur, Raipur, and Vizag. Prices softened amid weak export demand, EU market uncertainties, and rising inventories, while volatility in steel prices added further pressure.

Ferro manganese

Indian ferro manganese (HC 70%) prices inched down by INR 600/t ($7/t) w-o-w to INR 72,100/t ($804/t) exw-Durgapur, while prices in Raipur fell by INR 1,300/t ($15/t) w-o-w to INR 72,400/t ($808/t). The decline was driven by weak buying interest, limited acceptance of higher producer offers,and subdued spot demand pressuring mills to reduce quotations.

Ferro silicon

Indian ferro silicon (Si 70%) prices rose by INR 8,500/t ($95/t) w-o-w to INR 98,500/t ($1,099/t) exw-Guwahati, while Bhutan’s prices increased by INR 6,300/t ($70/t) to INR 97,800/t ($1,091/t). The uptrend was supported by tight supplies in both markets, prompting sellers to raise offers, pushing prices to a 7-month high.

Ferro chrome

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices declined by INR 800/t ($9/t) w-o-w to INR 114,700/t ($1,294/t) exw-Jajpur. The drop was driven by persistent bid-offer mismatches and subdued trading activity in the market, as most buyers waited for the outcome of the Odisha Mining Corporation’s (OMC) chrome ore auction. Meanwhile, at OMC’s chrome ore auction on 19 November, 88,400 t were sold out of the 93,800 t offered. Bids declined by 2-21% (INR 461–7,635/t) m-o-m across most grades, while bids for below 40% grades remained unchanged.

Semi-finished steel

India’s semi-finished steel market witnessed mild fluctuations this week, according to BigMint’s assessment. Domestic billet prices across major regions rose by INR 600-1,000/t ($6-11/t) on a week-on-week (w-o-w) basis, with the Hyderabad market recorded the sharpest increase of INR 1,000/t ($11/t). Buying activity remained moderate overall, while a slight improvement in finished-steel bookings done earlier lent additional support to billet prices.

In contrast, the sponge iron market remained largely range-bound. Raipur registered a marginal decline of INR 150/t ($1.6/t) w-o-w, whereas most other key regions reported small gains of INR 50-500/t ($0.5-5/t). Southern markets stood out, with prices rising more firmly in the range of INR 400-500/t ($4.5-5/t). The weekly price variations were due to regional differences in buying behaviour, reflecting uneven demand recovery across the major regions.

NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for 12,000 t on 17 November, of which the entire quantity were booked at an average price of INR 30,000/t (by rake). However, management approval is still pending. In the previous approved auction, held on 16 September for 32,000 t, 12,000 t quantity was booked at an average price of INR 30,400/t (by rake).

Indian DRI (Direct Reduced Iron) export offers softened further this week, declining by $4-5/t. Offers were reported at $310/t CPT Raxaul and $321/t CPT Benapole. The downward adjustment was due to weak demand from key importing countries and muted enquiries throughout the week.

Finished long steel

IF-rebar: India’s Induction Furnace (IF) route rebar prices moved upward w-o-w. In the initial days of the week, sellers saw moderate bookings supported by firm sponge iron and billet prices. However, as prices increased, buying activity weakened, with buyers avoiding large purchases at elevated levels. Many manufacturers focused on dispatching previously booked orders, indicating some pressure to clear earlier commitments. Inventory levels across regions remain around 10–15 days. As per current scenario, prices are expected to stay range-bound in the near term.

On a weekly basis, prices in rebar steel witnessed uptick in the range of INR 200-1,200/t across the regions, as per BigMint assessment. The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 38,200-38,600/t exw Raipur, INR 42,200-42,800/t exw Jalna.

Trade reference prices of heavy structural steel for base size 150mm channel stands at INR 40,000-40,500/t exw Raipur. Trade reference prices of wire rod hovering at INR 38,900-39,400/t ex Raipur.

BF-rebar: India’s trade-level blast furnace (BF) rebar prices fell w-o-w across major markets amid subdued domestic demand. Mills offered price support or slashed list prices due to weak market activities.

Trade-level BF rebar prices dropped by INR 700/t w-o-w to INR 46,600/t exy-Mumbai on 21 November. In the projects segment, prices hovered between INR 45,500-46,500/t FOR Mumbai. Buying inquiries from end-users were less amid decline in prices.

Flat steel

Trade-level prices of hot-rolled coils (HRCs) in India showed mixed trends in the week ended 18 November. Prices declined in some markets, while other regions witnessed range-bound trends. HRC prices stood at INR 46,500-48,100/tonne (t) ($526-544/t) across regions. Cold-rolled coil (CRC) prices ranged between INR 51,500-56,300/t ($582-637/t).

The domestic HRC market remained weak amid poor demand and abundant material availability. A market participant informed BigMint, “Mills and distributors are actively pushing sales as inventories stay moderate to high, but liquidity constraints are limiting purchases.”

India’s bulk imports of HRCs touched 110,480 t as of 15 November, based on vessel line-up data. Around 126,618 t of additional cargoes are expected by the end of November.

India’s bulk exports of HRCs touched 116,219 t as of 15 November 2025, and around 87,605 t of additional cargo are in transit.

BigMint’s Indian hot-rolled coil (HRC, S275) export index for the European Union (EU) region declined by $10/tonne (t) w-o-w to $520/t FOB main port on 18 November, with a deal heard concluded at around this level for December 2025 shipment. Additionally, the HRC (SAE 1006) export index for the Middle East dropped by $5/t w-o-w to $475/t FOB.

Leave a Reply