- Crude steel production drops 12.1% y-o-y in Oct’25

- Iron ore imports up 0.7% y-o-y on sustained stockpiling

- Real estate growth slumps, auto output up 13% y-o-y

Morning Brief: China, the world’s second-largest economy, is showing signs of a structural transformation and is slowly emerging as a more services- and consumption-led economy in stark contrast to its traditional reliance on infrastructure development and construction oiling the engines of economic growth. Likewise, in manufacturing, priority has shifted to the high-end sectors and tech-driven growth vis-à-vis the conventional dependency on steel and cement.

So, while the Chinese “economy maintained a generally stable momentum with steady progress”, as per the National Bureau of Statistics (NBS) in October, and also till date in CY’25, the structural transformation is evident. Total value added (GVA) in the economy increased by nearly 5% and the manufacturing sector recorded a 4.9% y-o-y growth in October.

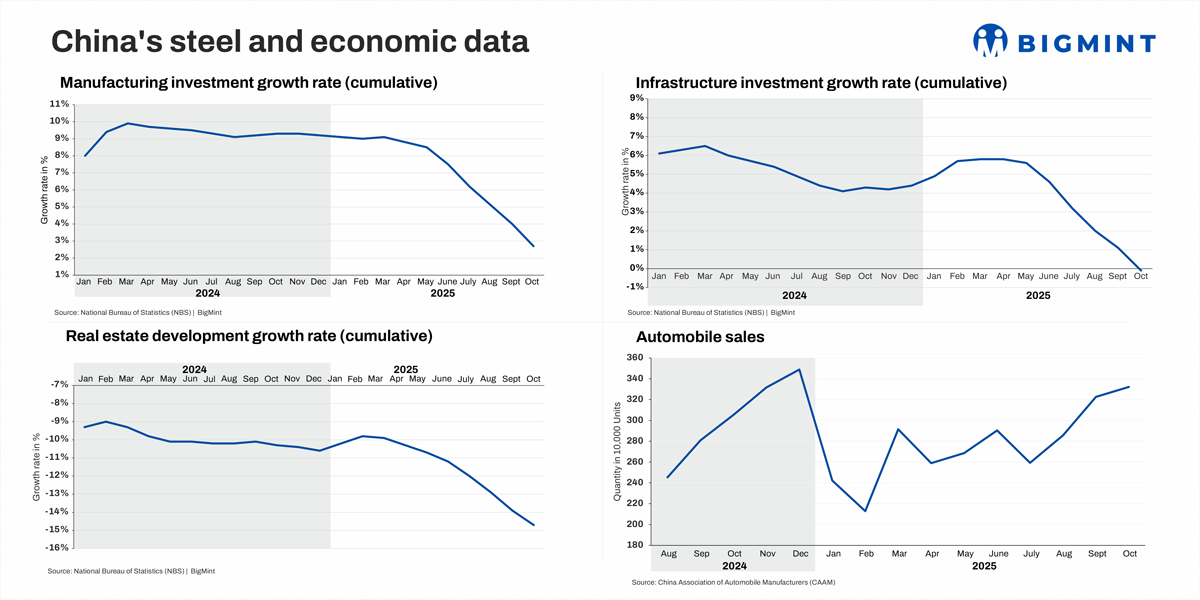

In the first 10 months of this year, investment in fixed assets (excluding rural households) fell by 1.7% y-o-y. Investment in infrastructure declined by 0.1% y-o-y, but manufacturing showed 2.7% growth. Real estate development declined by 14.7%. This shows that the traditional heavy industries such as steel and cement remained under pressure for the entire year.

Steel & key sector highlights in 10MCY’25

Steel production drops: China’s crude steel production in 10MCY’25 dropped nearly 4% y-o-y to around 818 mnt. CY’25 production is expected at around 970-980 mnt, i.e. below 1 bnt for the first time since Covid. At 72 mnt, October steel production was down 12.1% y-o-y. The decline in steel production comes as mills struggle to remain profitable amid higher input costs and muted demand from the key construction sector.

Heavy rain and flooding in the Northern provinces forced several blast furnaces to reduce production. Furthermore, the National Day holiday (from 1-8 October), weaker domestic demand and falling export sales weighed on production in October.

Notably, pig iron production slowed at a far lethargic pace compared with crude steel – by 1.8% y-o-y in 10MCY’25. This reveals that operating conditions and costs of the BF-based producers were healthier than the EAF-based producers.

Export growth slows down, imports decline: Steel exports at over 97.3 mnt in 10 months increased 6.6% y-o-y, slowing down from the 9.2% growth recorded in January-September. Exports dropped in October due to weakening global deman and increasing international trade protectionism. Key Southeast Asian and Latin American countries have implemented stricter anti-dumping policies, compelling Chinese mills to reduce their reliance on foreign sales. Also, fewer working days in October contributed to the decline in volumes.

Steel imports, on the other hand, declined by 12% y-o-y in January-October revealing a sustained downturn in domestic demand.

Iron ore imports rise slightly: The marginal 0.7% y-o-y growth in iron ore imports is a sign basically of a sentiment-driven market hinging its hopes on much-awaited stimulus as well as an amicable settlement of the trade dispute with the US. China has been rebuilding stockpiles, with port inventories monitored by SteelHome rising for an eighth week to 139.6 mnt in the seven days to 14 November.

According to a Reuters report, inventories are now up 7.3% from the 18-month low of 130.1 mnt in early August, but they are still short of the 150.7 mnt from November last year. This implies that there is still scope for stockpiles to rise in coming weeks, especially if prices remain relatively steady.

Coal production surges, imports dip: Chinese coal production in the first 10 months of this year reached nearly 4 bnt, an increase of 1.5% y-o-y. China’s domestic coal production strategy is geared toward mitigating energy shortage and price volatility. However, with higher production weighing on prices and profitability of coal producers, China has placed curbs on production which are likely to curb output in the remainder of CY’25.

Higher domestic production has naturally offset a share of import demand, with coal imports declining 11% on the year in 10MCY’25. Weakness in steel production has weighed on coking coal imports; however, imports of coking coal declined at a much slower pace of well below 5% y-o-y.

Cement output drops on real estate slump: China’s cement production fell by 6.7% y-o-y in 10MCY’25. However, the pace of decline slowed somewhat compared with the 9.8% y-o-y drop in CY’24. Capacity utilisation in the industry had dropped by 50% in CY’24.

As per NBS, real estate development declined by 14.7% during the review period. The floor space of newly-built commercial buildings sold was 719.82 million square metres, down by 6.8% y-o-y. Total sales of newly-built commercial buildings were RMB 6,901.7 billion, down by 9.6%. This was the key reason for the decline in cement production.

Auto production rises by 13% y-o-y: At over 29.6 million units, China’s automobile production rose by 13.2% y-o-y during the review period, mainly supported by the surge in NEV production. While auto sales in general increased by 3% from CY’24, NEV sales surged 20% on the year. This reflects strong consumer demand, especially for high-tech, low emissions products.

Notably, the surge in auto sales has failed to lift steel market sentiments, with cold-rolled, galvanised markets showing drooping sentiments despite an upbeat auto sector. However, electrical steel demand seems to be on the rise, thanks to the rapid growth of NEVs.

Outlook

Crude steel production is estimated to remain between 970 and 980 mnt in CY’25. After dropping to 72 mnt in October, monthly production is expected to remain at around 75 mnt in November and December. However, for reasons indicated above, iron ore imports may defy the general trend of de-growth in steel production.

Steel exports by China are expected to remain high on account on weak domestic demand but global trade barriers will make the going tough for mills. Domestic demand growth of 1% forecasted for CY’26 after a 2% de-growth in CY’25 will hinge on growth in NEVs and auto in general, new energy sectors, high-tech manufacturing and shipbuilding and, crucially, steel exports.

Leave a Reply