- Coal freight trends were mixed, with Pacific easing and Atlantic firm

- Indian demand stayed weak amid ample tonnage and lower bunker costs

Coal freight rates to India softened in the Pacific basin this week, even with a reasonable flow of fixtures, as improving vessel availability and slightly weaker regional sentiment weighed on rates. In contrast, the Atlantic basin rates held firm, supported by stronger export offers and tighter tonnage lists, which kept owners in a more favorable position. Overall, the market showed a split trend, with falling Pacific prices and firm Atlantic prices providing balance to broader sentiment.

“Asia-Pacific Panamax freight rates held largely steady to slightly softer, as FFA levels stayed rangebound through the Asian trading session. Bunker prices also eased marginally on the day, adding to the subdued tone in the market.,” a source said.

Coal freights on the Australia-India route eased this week, giving back the gains made in the previous week. The downturn was largely driven by subdued demand from Indian steel producers, many of whom stayed on the sidelines due to weak domestic steel consumption and ample material availability in the market. With most buyers adopting a wait-and-watch approach, activity thinned out noticeably. SAIL remained the only consistent buyer, providing limited support to an otherwise quiet market, while overall sentiment softened under the weight of muted procurement and comfortable supply conditions.

Freights on the South Africa-India route continued to push higher this week, even with limited fresh fixtures. The upward momentum was supported by stronger export offers, a tighter tonnage list, firm February-March 2026 forward freight levels, and increased Chinese buying interest. However, Indian demand stayed subdued, as a wide bid-offer gap and sluggish sponge iron procurement kept buyers from accepting the higher indications.

Meanwhile, Supramax freights on the Indonesia-India route dropped w-o-w. A ship operator noted, fixing activity on the Indonesia–India coal route remained notably thin, with only a handful of workable cargoes reported in the market. Limited enquiries from Indian buyers and a generally quiet trading environment kept spot activity subdued, leaving owners with few opportunities to conclude fixtures. Overall sentiment stayed muted as both supply and demand appeared balanced but without any signs of an uptick in demand.

Lower bunker costs provide marginal relief to owners: In the meantime, bunker prices have been drifting lower in recent sessions, easing cost pressures for shipowners across key regions. The decline is largely tied to softer crude oil prices, as Brent crude oil futures fell sharply w-o-w by about $1.57/barrel (bbl) to $62.23/bbl on 21 November, and improved availability of marine fuels, which together have pushed prices down marginally. This drop has provided some relief to operating expenses, especially for vessels on longer-haul routes, contributing to a slightly more relaxed sentiment on the cost side of the freight market.

Balanced tonnage keeps freight rates in check: The vessel supply situation for India remains relatively comfortable, with steady tonnage availability across major loading regions keeping a cap on freight upside. Demand from Indian importers – particularly in coal – has been inconsistent, creating periods where vessels outnumber workable cargoes. This imbalance has weakened owners’ negotiating power on several routes, while charterers continue to benefit from competitive rate levels. However, any sudden pickup in Indian procurement or tightening in regional tonnage could quickly shift the balance, making supply dynamics a key factor to watch.

Route-wise updates

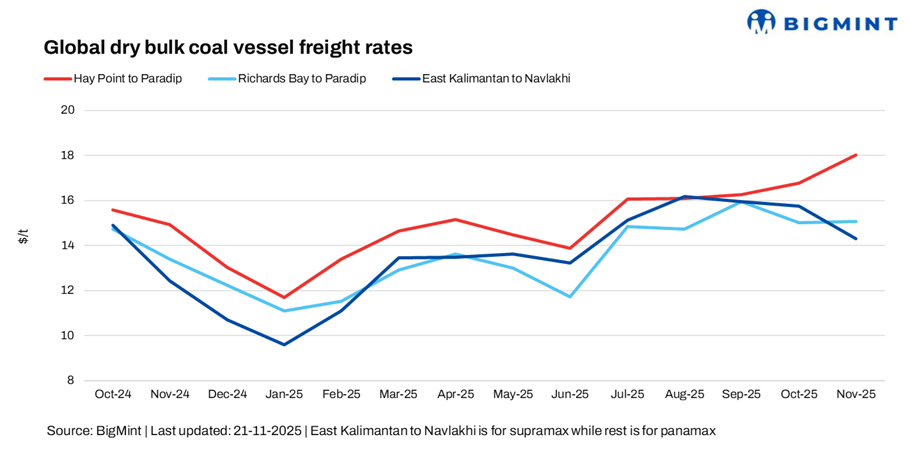

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India fell w-o-w by around 0.14/dry metric tonne (dmt) to $18.25/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route edged up marginally w-o-w by $0.9/dmt to $15.9/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $14.04/dmt, a decrease of $0.68/dmt, w-o-w.

Market highlights:

- Baltic index rises w-o-w: The Baltic Exchange’s dry bulk index for Panamax and Supramax vessels increased this week, with the Panamax index rising 15 points w-o-w to 1,912 and the Supramax index rising 48 points to 1,435. The Panamax and Supramax indices rose this week as improved cargo demand and steady fixing activity across key regions supported rates, while balanced vessel supply helped maintain firmer sentiment.

- Brent crude futures drop w-o-w: Brent crude oil futures fell sharply w-o-w by about $1.57/barrel (bbl) to $62.23/bbl on 21 November 2025 against $63.8/bbl on 14 November. Brent crude declined w-o-w as weaker demand sentiment, soft economic signals, and rising inventories weighed on prices, while steady supply from major producers offered little support.

Outlook

In the near term, coal freight rates to India are expected to remain rangebound to slightly soft, as inconsistent buying interest from Indian importers continues to limit upside momentum. Sponge iron and power sector demand remains muted, while ample coal availability – both domestically and in key exporting regions – has kept procurement subdued. This has resulted in fewer cargoes coming to the market, reducing charterer competition and capping freight gains.

On the supply side, tonnage availability remains comfortable across Indonesia, South Africa, and Australia, further restraining rate increases despite occasional firmer offers from owners. Any meaningful uptick in Indian demand, a tightening of regional vessel supply, or sustained strength in forward freight markets could lend support, but for now, the market is likely to maintain a cautious, slightly pressured tone.

Leave a Reply