- Seaborne prices edge up on supply tightness

- Freights ease further, softening landed costs

Portside prices of Indonesian thermal coal in India remained broadly stable w-o-w on 21 November 2025, underpinned by firmness in global coal benchmarks. Supply constraints in Indonesia and steady demand pushed up export prices.

According to a market participant, “Price movements were limited throughout the week and Chinese buying activity slowed, while reports of Indonesia potentially reducing its 2026 annual production have not yet influenced market sentiment.”

Domestically, traders attempted to raise offer prices; however, a lack of strong procurement interest resulted in limited deals concluded at higher levels.

A trader from Magdalla further noted that “substantial stock availability at ports has reduced the need for additional purchases, with existing inventories expected to suffice until January 2026.”

Key grades show stability

BigMint’s assessments continued to reflect stability across most Indonesian coal grades. The 5000 GAR grade remained unchanged w-o-w at INR 7,200/t at Kandla and INR 7,100/t at Vizag, whereas the 4200 GAR grade held at INR 5,850/t at Kandla and INR 5,750/t at Vizag.

The 3400 GAR grade showed a marginal increase of INR 50/t to INR 4,600/t at Navlakhi. The relative stability across grades indicates a balanced market, where adequate portside supply is meeting the currently muted demand environment.

Freights ease further, softening landed costs

Freights on the Indonesia (East Kalimantan)-India (Navlakhi) Supramax route continued to soften, declining by $0.62/dmt w-o-w to $14.04/dmt. The sustained fall in rates reflects easing vessel tightness and subdued fixture activity. Lower freight costs reduced landed costs but were not sufficient to stimulate meaningful buying interest in the domestic market.

Port inventories strengthen on improved vessel arrivals

India’s portside thermal coal inventories increased by 2.2% w-o-w to 12.84 mnt in week 46 (10-16 November), compared to 12.57 mnt in week 45. The rise was largely driven by enhanced vessel arrivals at key east coast ports. In contrast, west coast ports recorded mixed trends due to selective vessel inflows and steady dispatch rates. The inventory build-up reinforces a comfortable supply position, further reducing urgency among buyers.

Power sector stock levels improve, but localised strains remain

Coal stocks at Indian power plants increased to 52.89 mnt as of 19 November, up from 51.56 mnt a week earlier, providing approximately 17 days of consumption cover. Despite the overall improvement, 13 power plants remain in the critical stock category, with five reliant on domestic coal, six on imported coal, and two on washery rejects. These discrepancies reflect ongoing logistical challenges, uneven mine dispatches, and regional supply distribution imbalances. As winter demand gradually picks up, strengthening supply chain coordination will be vital to avoid localised shortfalls.

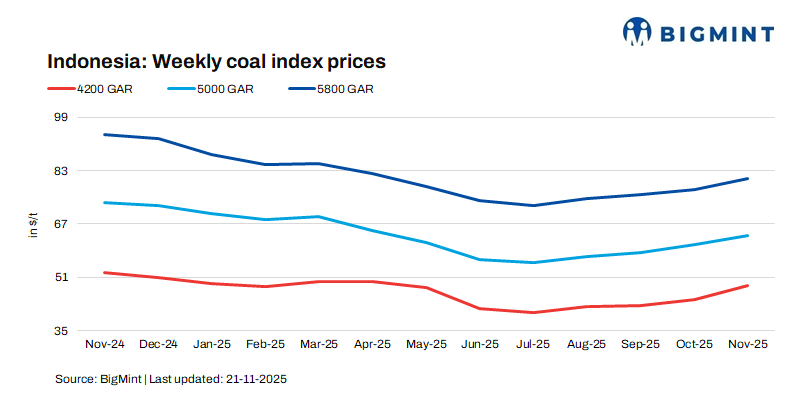

Seaborne prices lift on weather-driven supply tightness

Indonesian seaborne coal prices registered slight increases during the week, supported by moderate Chinese tender activity and emerging supply constraints due to rainfall in Kalimantan. The 5800 GAR grade edged up by $0.77/t, the 4200 GAR grade rose by $0.52/t, and the 3400 GAR grade increased by $0.07/t.

Weather-related disruptions have begun to slow mine output and hinder loading operations, raising expectations of tightened supply through late November. Concurrently, sustained buying interest from South Asian markets is lending additional support to prices.

Outlook

Portside prices are expected to remain steady amid ample stocks and soft demand, while seaborne prices may see slight gains if Indonesian supply tightens. Overall, the market should stay range-bound with limited upside risk.

Leave a Reply