- Stricter monitoring, anti-reselling measures to streamline execution

- Greater flexibility given to utilities for renewable energy consumption

Mysteel Global: China’s National Development and Reform Commission (NDRC), the country’s top economic planning agency, has released its guidance for the signing of medium- and long-term (MLT) thermal coal contracts for 2026, with most requirements broadly consistent with those applied for 2025.

Under the 2026 guideline, contracting parties again include all operating coal enterprises on the supply side and all unified-dispatched public power plants on the demand side, as well as other facilities responsible for ensuring residential power and heating supply. These mirror last year’s arrangements, Mysteel Global notes.

The NDRC also reiterates its encouragement for provinces with centralised heating systems to organise local heating enterprises to join MLT contracts based on their own conditions. This represents a subtle expansion on last year’s focus for this year, which had put emphasis on firms in northern provinces concluding such contracts.

One notable adjustment appears in the contracting method. The NDRC now explicitly bans multi-tiered third-party contracting that artificially increases trading layers and, at the same time, strictly forbids reselling contracted resources for arbitrage. In parallel, the commission reaffirms that parties may contract independently through market-based mechanisms, while placing limits on third-party involvement. This reflects the regulator’s ongoing efforts to streamline trading links and curb price manipulation.

Contract volume requirements remain largely unchanged. Coal mining enterprises must continue to allocate at least 75% of their self-owned resource volume for sale under MLT contracts, unchanged from 2025 but down from the 80% requirement applied during 2024. As before, the NDRC will assign supply tasks to producing provinces and central state-owned enterprises, which will in turn distribute these tasks among all operating mines.

On the demand side, power and heating suppliers must sign MLT contracts covering no less than 80% of their consumption, which is measured based on their demand during the period spanning November 2024-October 2025. Although the proportion is the same as last year, the guideline stresses that contract volumes should be determined after fully accounting for factors such as renewable energy substitution. This update introduces greater flexibility for utilities during periods when renewable output peaks.

Both sides may continue to break annual volumes into monthly quantities, and the practice of “storing during low-demand seasons for use in peak-demand seasons” continues to be encouraged by the NDRC. The monthly allocation for low-demand periods should be no less than 80% of that for peak months, which is consistent with the 2025 rules.

The pricing mechanism is also unchanged. Term contract prices must remain within the “reasonable range” set by the NDRC and its local branches. For example, 5,500 kcal/kg NAR thermal coal at northern ports remains within the range of RMB 550-770/tonne (t) ($77.3-108.2/t), FOB with VAT. The contract price structure still consists of “fixed price + floating price,” with the fixed portion maintained at RMB 675/t (5,500 kcal/kg NAR). The floating portion continues to draw from four indices — namely CECI, CCTD, BSPI, and NCEI — with final prices published monthly by the National Coal Exchange Center.

For 2026, contracts must once again include clear quality specifications and detailed mechanisms for settling deviations, aligning with the principle that “premium coal commands premium prices.” This extends the wording used for 2025.

On contract enforcement, the NDRC reiterates that parties must strictly adhere to agreed quantities, qualities, prices, and other terms. The minimum performance requirement remains 90% for annual and quarterly volumes and no less than 80% for monthly volumes, with even higher fulfilment expected during seasonal peaks such as summer and winter.

A new addition for 2026 requires provincial authorities and relevant central enterprises to strengthen coordination and monitoring of contract performance and to conduct self-assessments every six months, a directive containing more granular oversight expectations than in past years.

Overall, the 2026 guidance underscores the continued importance of medium- and long-term contracts in securing China’s thermal coal supply. The largely unchanged framework suggests that policymakers anticipate that supply and demand will be generally balanced next year — which is broadly similar to that of 2025, Mysteel Global notes.

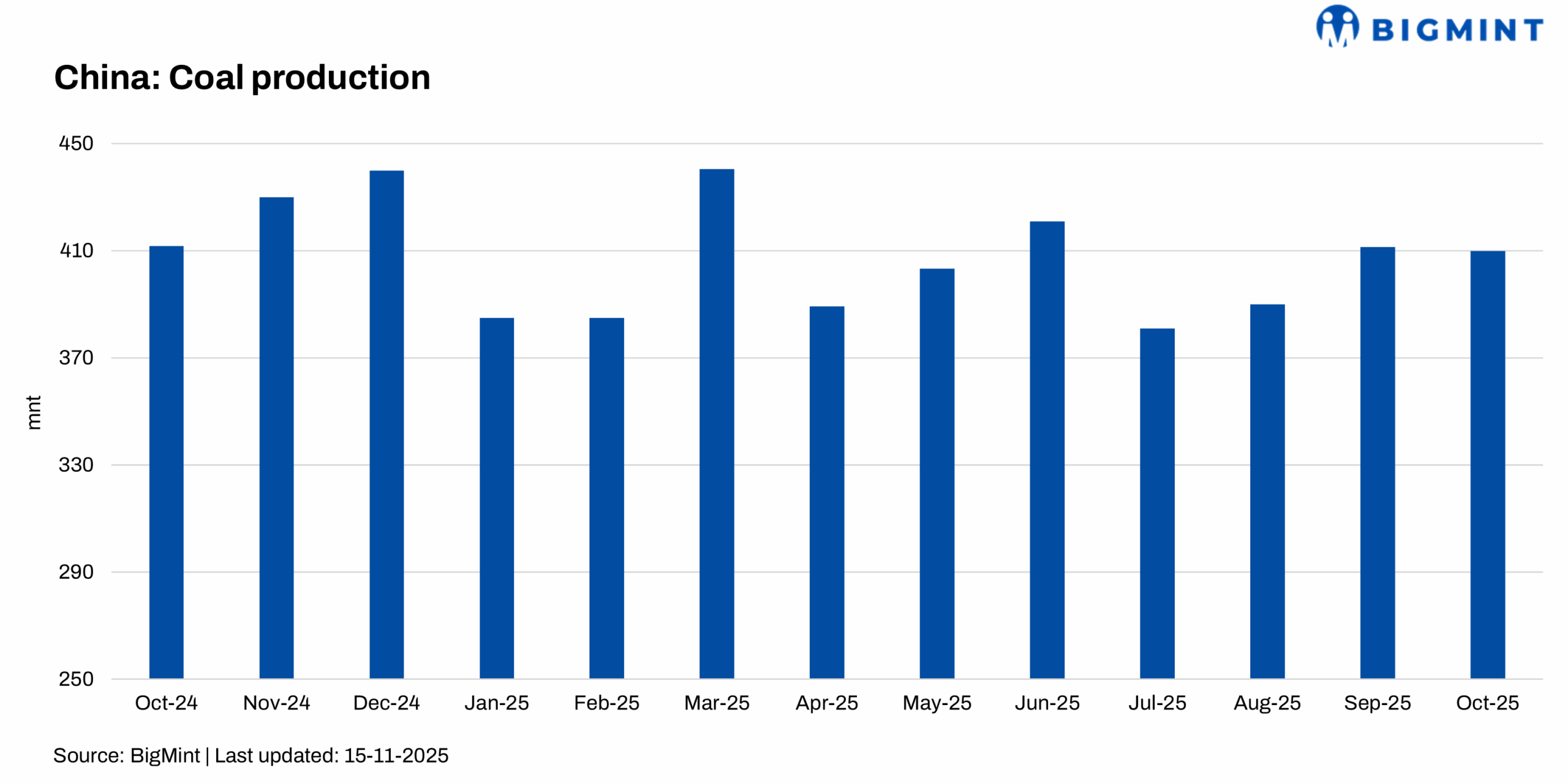

From January to October, China’s raw coal output reached 3.97 billion tonnes, up 1.5% y-o-y, according to official data. The sustained growth has led analysts to expect full-year production to exceed 2024’s 4.76 billion tonnes, which marked a record high for the country’s coal mining sector.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply