- Guinea’s Simandou project to add to global iron ore supply

- Demand to wane as China reduces crude steel production

Mysteel Global: Supply of iron ore in the global market has not loosened this year as much as expected after the market shifted from a tight supply-demand balance to loose supply in 2024, Wang Yilin told delegates attending the 2025 16th Ferrous Value-Chain Summit held in Southeast China’s Xiamen on November 19. Wang is deputy general manager of market research at China Mineral Resources Group (CMRG), a state-owned company managing domestic mineral resources.

Nonetheless, global iron ore supply is set to loosen in the coming years, Wang maintained, not only because of new mining projects being launched but also an anticipated weakening of Chinese demand as the central government presses mills to focus on quality steel in future, rather than quantity.

China, the world’s largest steel producer by far, is committed to controlling its crude steel production, yet throughout much of this year, it has nonetheless displayed firm demand for iron ore. During this year’s January-September period, the country’s iron ore consumption gained by 3.4% y-o-y, contributing to the overall 1.5% y-o-y rise seen in global iron ore demand during the same period, CMRG data show.

Though China’s National Bureau of Statistics (NBS) data shows total crude steel output during January-October falling by 3.9% y-o-y to 817.9 million tonnes (mnt), throughout much of this year, steelmakers have struggled to secure sufficient quantities of ferrous scrap — as sources of supply such as demolition scrap have declined, as Mysteel Global has reported — which has lifted demand for iron ore.

In addition, Wang attributed this year’s stronger-than-expected appetite for iron ore to robust Chinese steel exports. The latest data from China’s General Administration of Customs showed that China’s finished steel exports rose 6.6% y-o-y during this year’s first ten months to 97.7 mnt.

The Trump Administration’s campaign to raise US steel import tariffs has so far had only a limited impact on China’s direct steel exports, while anti-dumping measures imposed by other countries targeting Chinese steel products have only affected certain categories, she elaborated. “For example, we saw a significant decline in hot-rolled-coils exports this year, but the total amount of our steel exports continued to grow, with prominent increases seen in billet exports,” she said.

In addition, improved profitability among Chinese steelmakers — thanks to robust exports and lower costs of steelmaking raw materials, including iron ore and metallurgical coke — also prompted them to be active in production, underpinning iron ore demand, she added.

During the first nine months of this year, China’s steel sector earned RMB 97.3 billion ($13.7 billion), in stark contrast to a loss of RMB 34 billion during the same period last year, according to NBS data.

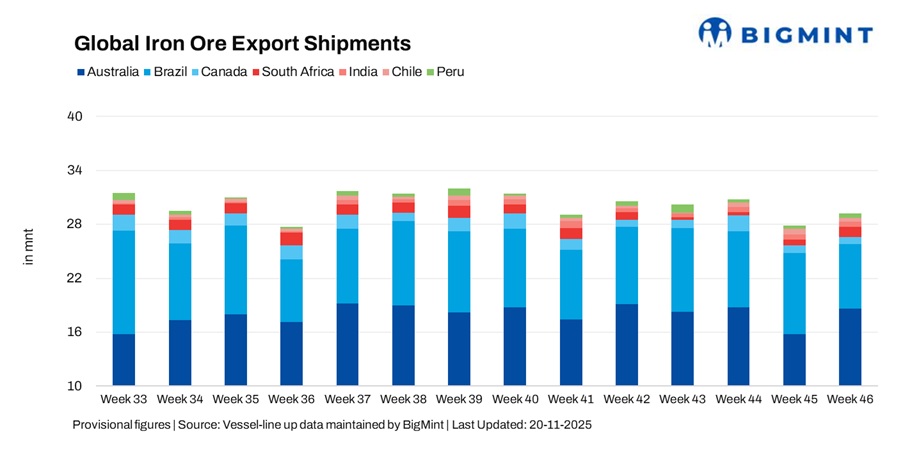

On the supply side, global iron ore shipments increased by 1% on year during the first ten months of this year, GMRG data showed. “But this has underperformed,” Wang said, referring to the severe cyclones that disrupted Australian iron ore shipments during this year’s first quarter. She also pointed out that China’s domestic concentrate supply has tightened this year due to the expiry of mining licences among miners in northern regions.

True, the global iron ore market is still oversupplied, but the supply glut is not intensifying to any great degree due to disrupted shipments from some miners and resilient demand from Chinese steelmakers, according to Wang.

Looking ahead, the general picture is unchanged, Wang noted, arguing that global iron ore supply will resume loosening, particularly with the recent commissioning of the massive Simandou iron ore project in Guinea, West Africa, as Mysteel Global reported.

Simandou will drive up global iron ore output to 2.92 billion tonnes in 2030, up from 2.38 billion tonnes in 2025, said Wang, citing a forecast from London-based commodity research provider Commodity Research Unit. She also estimated that China’s domestic concentrate capacity will reach 352 mnt/year by 2030, a huge improvement from the 300 mnt produced in 2024.

In contrast, global consumption of iron ore is set to decline, despite a slight increase in overall crude steel output. This is because China, the world’s largest iron ore consumer, intends to reduce crude steel production to 895 mnt by 2030, down from 1 billion tonnes last year, Wang forecast. “The growth in iron ore demand from other countries just cannot offset the decline in China’s,” she said.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply