- Demand for Japanese scrap remains weak in Vietnam

- US offers firm, as Turkish mills continue procurement

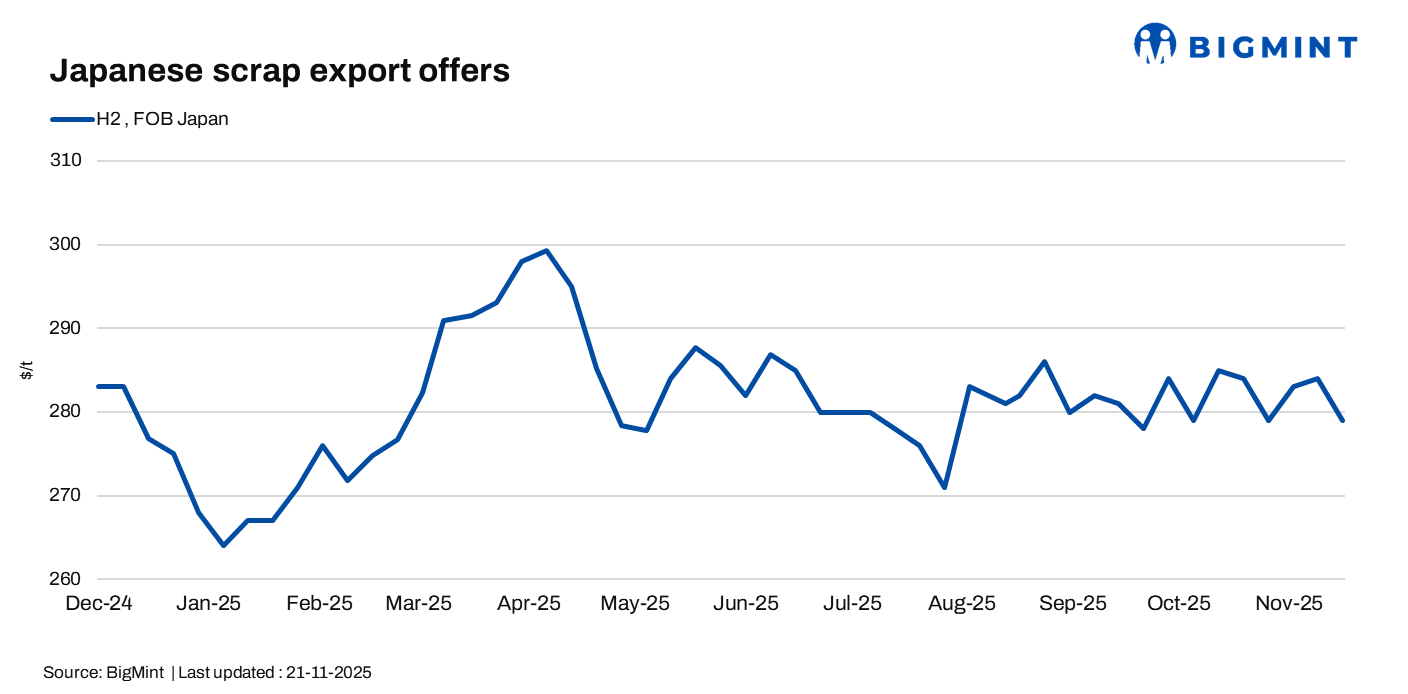

Japanese scrap export offers dipped, while US prices remained steady w-o-w on 21 November. Demand from Asia remained weak, while price corrections for scrap were somewhat offset by tight supply (in the US particularly) and stable rebar offers. Freight constraints and slow inflows could lift Japanese and US export prices towards the year-end.

Japanese scrap export prices edge down

BigMint assessed Japan’s H2 scrap at JPY 43,700/t ($278/t) FOB Tokyo Bay, down JPY 200/t ($1/t) from last week.

A Vietnamese trader noted that rebar demand had slowed down after Typhoon Kalmaegi restricted mills’ ability to raise prices. Japanese scrap remained above buyers’ expectations, who turned to cheaper regional or domestic material.

H2 scrap offers to Vietnam eased to $325-330/t CFR, with bids dropping to $320/t. Tradable levels stayed at $320-325/t.

Domestic mill updates: Tokyo Steel raised H2 scrap prices by JPY 500/t ($3/t), effective 20 November 2025. Post-revision, prices were as follows: Tahara/Okayama/Kyushu/Tokyo Bay: JPY 44,500/t ($282/t), Nagoya/Kansai: JPY 44,000/t ($279/t), Utsunomiya: JPY 43,500/t ($276/t), and Takamatsu: JPY 39,500/t ($251/t).

US scrap export offers remain stable w-o-w

US export prices remained stable, as Turkish mills continued to procure material, with deals closed within a narrow price range. Most HMS 80:20 deals were concluded at $355-356/t CFR and shredded at $375-376/t CFR.

Vessel availability remained tight, with freights at $47/t, and slow scrap inflows at US yards — due to fewer demolition jobs — raised concerns about supply constraints for upcoming orders.

Domestic mill updates: US domestic and imported rebar prices remained firm, as tight supply and limited imports left buyers accepting the recent $30/t mill hike. Demand from infrastructure and data centre projects significantly tightened material availability, leaving buyers facing reduced supply and limited options in the market.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $325/t, stable w-o-w.

- Shredded – $345/t, stable w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – stable w-o-w at $356/t.

- Vietnam – up by $3/t w-o-w at $348/t.

- Bangladesh – up by $2/t w-o-w at $353/t.

Outlook

Japanese scrap export offers are expected to climb up in the near term. Japan-Vietnam freights are expected to climb towards the year-end as vessel availability tightens seasonally. Some Japanese mills have also lifted offers, supported by the weaker JPY.

In the US, exporters are facing slow scrap inflows, raising concerns about possible supply shortages for upcoming shipments. While prices have not moved up yet, exports expect hikes in January as weather and seasonal demand strengthen.

Leave a Reply