- Retail sales improve across all categories

- Stable macro conditions lift buyer confidence

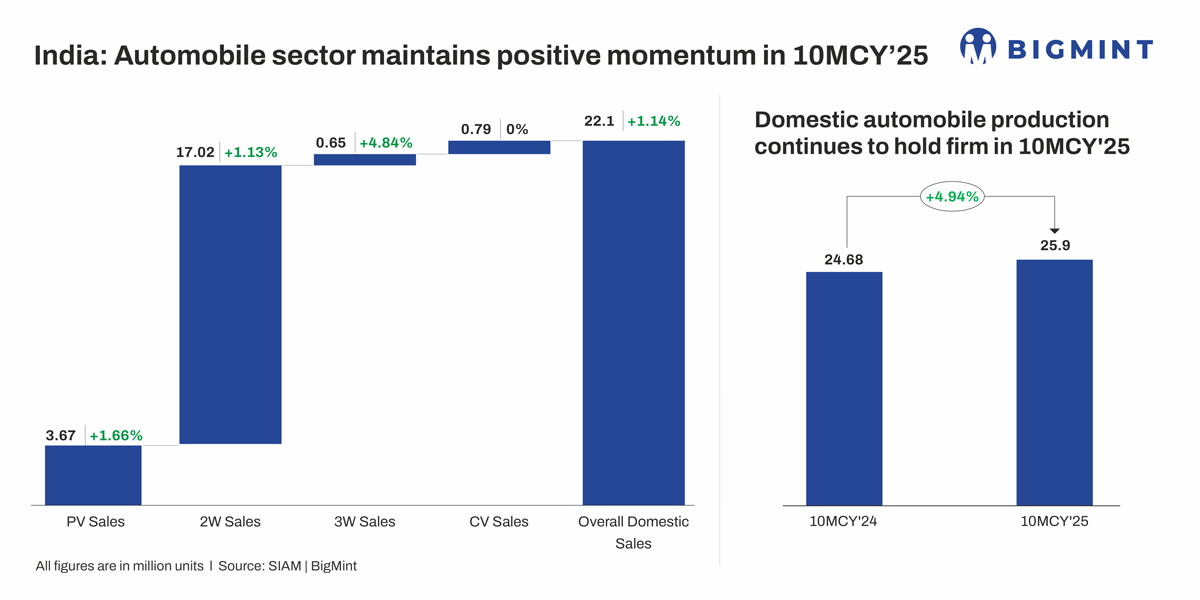

India’s automobile sector showed steady growth in 10MCY’25, as per SIAM OEM data. Passenger vehicle sales rose 1.66% y-o-y to 3.67 million units, while two-wheeler sales increased by 1.13% to 17.02 million units. Three-wheeler sales posted a strong 4.84% jump to 0.65 million units, whereas commercial vehicle (CV) sales remained unchanged at 0.79 million units. Domestic sales improved 1.14% y-o-y to 22.1 million units. Total production saw a healthy rise of 4.94%, reaching 25.9 million units, reflecting continued manufacturing momentum across the sector.

Retail sales improve in 10MCY’25

Meanwhile, FADA’s retail data for 10MCY’25 showed strong consumer momentum across vehicle categories. Passenger vehicle sales rose 6.87% y-o-y to 3.58 million units, while two-wheeler sales increased 8.72% to 16.34 million units. Three-wheeler sales grew 2.94% to 1.05 million units, and CV sales improved 4.76% to 0.88 million units. Tractor demand also strengthened, rising 7.04% to 0.76 million units. Overall retail sales climbed 7.82% y-o-y to 22.6 million units, indicating broad-based demand resilience in the automotive market.

Retail vehicle demand strengthened significantly in 10MCY’25, supported by robust rural and semi-urban buying sentiment. Improved farm incomes and stable rural economic activity boosted two-wheeler, three-wheeler and tractor sales, with these segments responding quickly to better liquidity and mobility needs in smaller towns. Affordability also improved as tax reforms and easier financing conditions encouraged more first-time and replacement buyers, further lifting retail momentum across categories.

At the same time, rising middle-class incomes, a young consumer base and growing mobility requirements contributed to steady interest in passenger vehicles and commercial vehicles. A continuous flow of new model launches — especially in popular commuter and premium categories — helped sustain footfall and conversion. Strong manufacturing and export activity supported overall supply availability, ensuring smoother deliveries and reinforcing buyer confidence. Together, these structural and policy-driven factors explain the broad-based rise in retail sales across all segments, as reflected in FADA’s 10MCY’25 data.

Healthy momentum expected in H2FY’26

India’s automobile sector has entered the second half of FY’26 on a positive note, supported by early and extended festive season demand, improving affordability, and stable macroeconomic conditions. The festive cycle began earlier this year — from 22 September — boosting retail activity towards the end of Q2 and setting a strong base for Q3. The extended festive and wedding season is expected to keep consumer sentiment firm across all categories. Rural vehicle demand continues to hold steady, aided by a broadly healthy kharif harvest and stable rural income trends, despite temporary disruptions caused by regional flooding. Alongside this, ongoing GST 2.0 reforms, earlier interest-rate rationalisation, and recent tax relief measures have collectively strengthened affordability and buyer confidence, supporting sustained growth in two-wheelers, passenger vehicles, three-wheelers and tractors.

At the structural level, the industry continues to benefit from rising household incomes, a young demographic profile, expanding product choices, and a clear shift towards premiumisation — especially in SUVs and feature-rich scooters. Strong domestic manufacturing and export momentum further underpin production growth, helping companies maintain steady supply and build inventory for peak-season demand. Improvements in national highways, logistics networks, and urban mobility infrastructure are supporting higher vehicle utilisation and replacement cycles, bolstering commercial and public-transport segments. While the industry remains attentive to global uncertainties, the combination of festive demand, policy support, rural stability, and robust manufacturing fundamentals positions the sector to close FY’26 on a healthy growth trajectory.

Impact on aluminium ADC12 alloy

India’s ADC12 aluminium alloy market has strengthened notably, driven by a clear revival in the automotive sector. Higher retail and wholesale vehicle sales, supported by GST reforms, improved financing, and strong festive demand, have boosted the need for die-cast components used in passenger vehicles, two-wheelers, EVs, and commercial vehicles. Because ADC12 is a key alloy for engine casings, transmission housings, structural parts, and lightweight automotive components, this surge in automotive production has directly translated into stronger alloy consumption. The widening scrap-to-ADC12 spread also signals tighter availability of quality scrap and increased conversion demand as suppliers gear up for higher OEM requirements.

This improved demand environment triggered a firm price rebound in October 2025. BigMint reported m-o-m increases across major markets, with OEM ADC12 prices rising to INR 231,000/t in Delhi and Pune and INR 232,000/t in Chennai, while spreads widened to INR 39,000-43,000/t. Additional support came from global markets, where rising LME aluminium levels pushed international scrap prices higher, even as domestic scrap corrected due to better supply. Together, stronger automotive demand, improved affordability, and supportive global cues have reinforced a positive outlook for India’s ADC12 alloy market heading into the final quarter of 2025.

Outlook

India’s automobile sector is likely to maintain steady growth in the coming months, supported by strong festive-season sentiment, GST-led affordability improvements, stable rural demand, and firm retail momentum across all major vehicle categories. With manufacturing activity healthy and consumer confidence intact, the industry is positioned to close FY’26 on a positive note. This strength is also expected to keep the ADC12 aluminium alloy market firm, as rising vehicle production — especially in SUVs, two-wheelers, and EV components — continues to drive demand for die-cast parts, supporting stable-to-upward pricing into early FY’27.

Leave a Reply