- China’s winter restocking continues, but weak steel margins limit buying

- Softer Capesize rates, ample vessel supply drag down freight sentiment

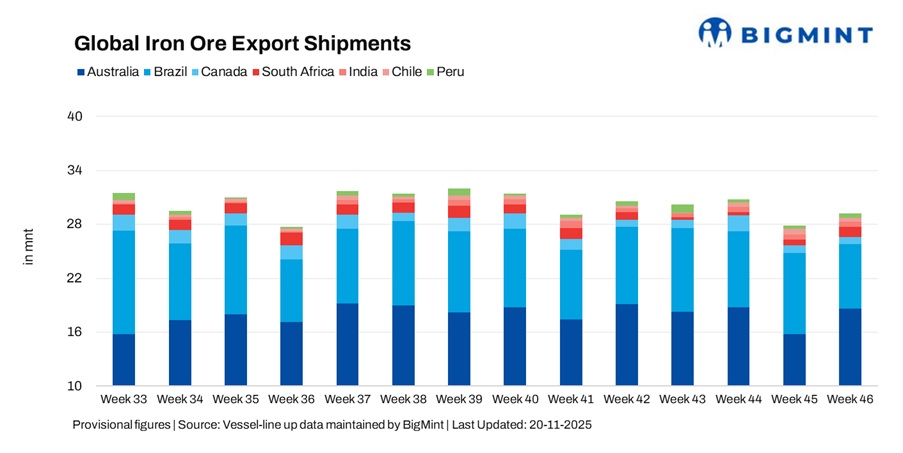

Global iron ore exports increased 5% to 29.27 million tonnes (mnt) in week 46 (08-14 November) from 27.80 mnt a week earlier, supported by a strong rebound in Australian shipments and continued gains from India and South Africa. The recovery helped offset notable declines from Brazil and Chile, where adverse weather and logistical inefficiencies slowed loading activity. Despite improving global volumes, freight sentiment weakened, as softer Chinese demand and improved vessel availability across major basins exerted downward pressure on Capesize rates.

Although winter restocking persisted, muted steel margins and high portside inventories in China kept buying momentum in check. This, coupled with easing congestion in Brazil and Australia, limited chartering activity and diluted freight market strength. Higher voyage costs due to elevated bunker prices further constrained exporters, particularly on long-haul shipments, restricting incremental volumes despite favourable weather conditions in key regions.

Australia’s iron ore shipments rebound strongly

Australia’s iron ore exports surged 18% w-o-w to 18.62 mnt in week 46 from 15.77 mnt in week 45, marking a strong rebound after several muted weeks. Improved vessel turnaround and steadier berthing operations across Pilbara ports drove the increase, with higher throughput from Port Hedland (12.94 mnt), Dampier (3.24 mnt), and Walcott (2.05 mnt) reflecting a clear improvement in loading efficiency. Among major miners, BHP (6.42 mnt), Rio Tinto (5.29 mnt), and FMG (4.67 mnt) collectively dominated outbound volumes as scheduling and port operations normalised.

Shipments to China rose to 17.03 mnt, supported by ongoing winter restocking, although subdued steel mill margins tempered stronger buying interest. Exporters continued to experience mild cost pressures despite easing Capesize rates, as overall market sentiment remained cautious across the Pacific. So far this year, Australia has shipped slightly more iron ore than at the same point in 2024, and while exports are expected to keep growing in the coming years, prices may soften due to new supply from Africa, with Port Hedland remaining a key indicator of nationwide shipment trends.

Brazil’s exports drop on weather disruptions

Brazil’s iron ore shipments fell sharply by 20% w-o-w to 7.19 mnt in week 46 from 8.99 mnt a week earlier, as weather-related disruptions once again curtailed loading performance at key ports. Reduced throughput at Ponta da Madeira (3.28 mnt), Tubarao (1.15 mnt), and Itaguai (1.47 mnt) weighed on weekly volumes, with intermittent rains and slower vessel clearance contributing to operational delays. Miners adjusted dispatch schedules accordingly, leading to lower overall port activity.

Shipments to China eased to 3.13 mnt, while volumes to India softened to 0.38 mnt, with some cargoes diverted to Middle Eastern and European markets, though not enough to offset the broader decline. Vale remained the leading exporter at 3.75 mnt, followed by CSN with 2.62 mnt. Softer Chinese demand for high-grade fines, combined with weaker long-haul freight sentiment, further discouraged aggressive chartering and added to the week’s downward pressure on exports.

Canada’s volumes soften amid logistical bottlenecks

Canada’s iron ore exports slipped 7% w-o-w to 0.81 mnt in week 46 from 0.87 mnt, as minor rail delays and moderate port congestion slowed loading activity. Movements through Sept-Iles (0.60 mnt) and Port Cartier (0.21 mnt) reflected a quieter operational week following the strong rebound witnessed earlier. Tight wagon availability and uneven miner dispatches further limited throughput, keeping export flows subdued.

Demand from key buyers remained muted, particularly from Europe, while marginal declines in freights were insufficient to stimulate additional bookings. The Netherlands (0.18 mnt) and China (0.17 mnt) emerged as the principal importers during the week. Among major shippers, Guinea and Nimba Mines accounted for 0.35 mnt, followed by IOC with 0.26 mnt and ArcelorMittal with 0.21 mnt, collectively shaping the week’s modest export volumes.

South Africa records strong upturn as rail flows stabilise

South Africa’s iron ore exports rose sharply by 77% w-o-w to 1.08 mnt in week 46 from 0.61 mnt, supported by improved rail connectivity and stronger loading productivity at Saldanha Bay. The clearing of earlier backlogs and steadier miner-to-port dispatches significantly boosted weekly throughput, helping South Africa recover from previous operational constraints.

China and European buyers increased their intake to 0.77 mnt and 0.13 mnt, respectively, supported by more consistent availability of medium-grade material. However, despite the weekly rebound, uncertainty around rail reliability and intermittent logistical challenges continues to limit the prospects of sustaining higher export levels in the coming weeks.

India’s exports edge up on steady Chinese buying

India’s iron ore exports rose 7% w-o-w to 0.62 mnt from 0.58 mnt, supported by higher loadings from Paradip (0.28 mnt) and Dhamra (0.11 mnt). Odisha-based miners benefitted from better vessel allocations and steady restocking demand from China, which absorbed 0.23 mnt of the shipments and remained the primary destination for outbound cargoes.

However, rising voyage costs on smaller vessels compressed exporter margins, restricting stronger growth in weekly shipments. Additionally, the limited availability of higher-grade fines and concentrates capped the upside, keeping overall export momentum moderate despite improved port activity.

Divergent week for Chile, Peru’s iron ore shipments

Chile’s iron ore exports fell 26% w-o-w to 0.41 mnt as adverse weather and slower loading cycles at Huasco (0.37 mnt) and Tocopilla (0.03 mnt) hindered shipment activity. Chinese buyers remained the top destination with 0.20 mnt, followed by Bahrain at 0.17 mnt, but constrained supply availability and operational delays curbed overall export momentum during the week.

In Contrast, Peru’s exports rose 25% w-o-w to 0.54 mnt from 0.43 mnt, supported by smoother port operations at San Nicolas (0.51 mnt) and Matarani (0.04 mnt). Consistent dispatches from major miner Shougang Hierro, which shipped 0.51 mnt, underpinned the weekly increase. China continued to dominate the intake, importing the full 0.54 mnt amid firm demand for low- to medium-grade cargoes.

Freight sentiment softens as Capesize market weakens

Freight market sentiment weakened this week, driven by softer Chinese demand, improved vessel availability across major loading regions, and a decline in chartering momentum that placed downward pressure on Capesize rates. While winter restocking continued, it was not strong enough to offset the impact of subdued steel margins and weak fixture activity, leading to reduced long-haul freight levels.

Smaller vessels remained better supported due to steady minor bulk movements, but rising bunker prices kept voyage costs elevated for exporters, mildly constraining shipment expansion despite operational improvements at several ports.

Outlook

Global iron ore shipments are expected to remain stable heading into late November, with Australia and South Africa likely to support overall volumes, while Brazil may continue to face intermittent weather-related pressures. However, subdued Chinese demand, soft Capesize rates, and improved vessel supply could limit further upside in exports. Minor port disruptions and seasonal factors will play a key role in shaping weekly flows, while freight softness may encourage cautious scheduling from miners in the near term.

Leave a Reply