- DGTR flags dumping of LAM from 6 countries

- Indian pig iron spot prices firm up w-o-w

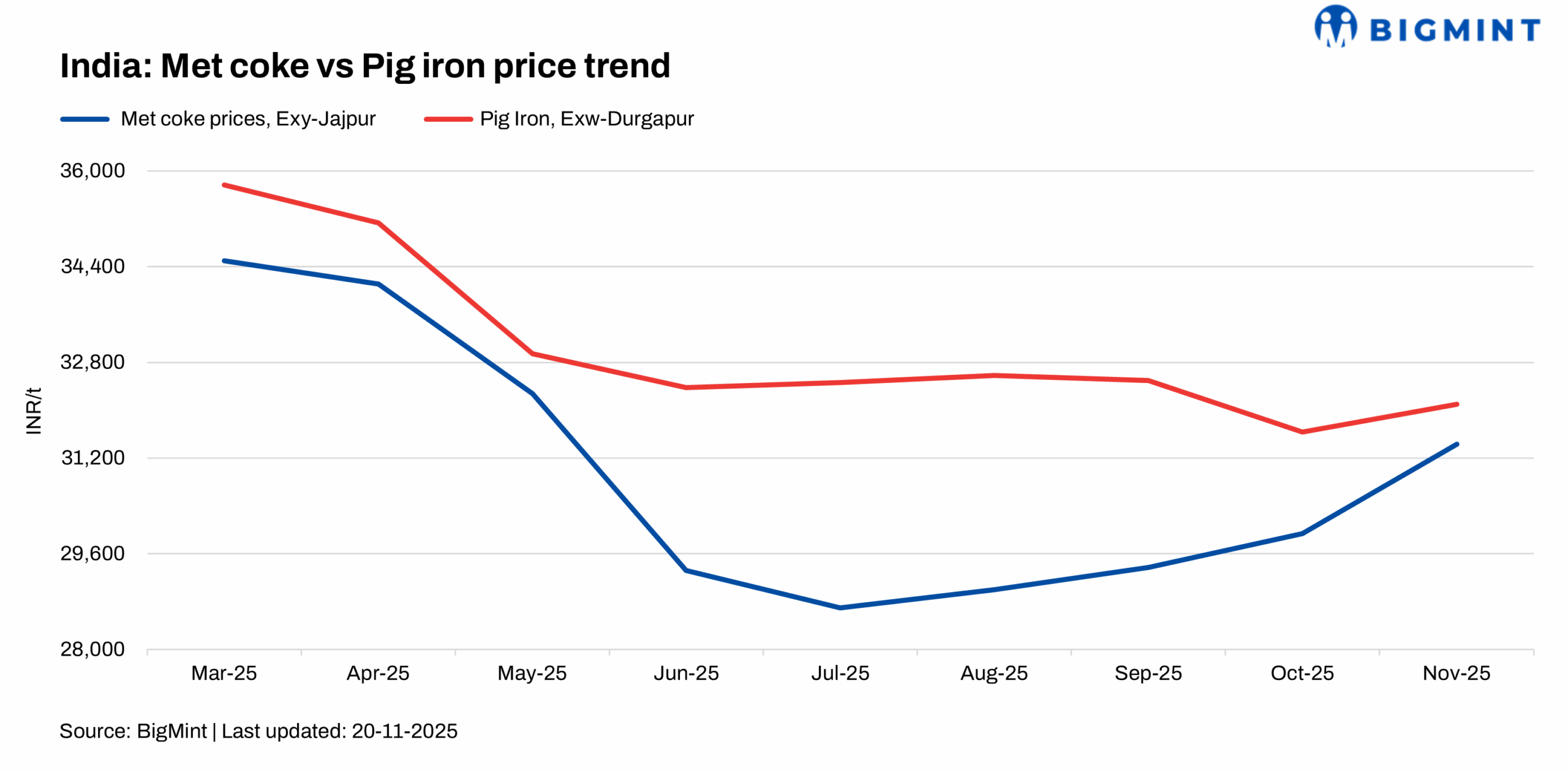

The Indian metallurgical coke (met coke) market witnessed mixed trends in the week ending 20 November 2025, with stable pricing in the west and mild w-o-w gains in the east. Demand was healthy, particularly in eastern markets.

In eastern India, BF-grade (25-90 mm) met coke was assessed at INR 31,800/t ex-Jajpur, marking an INR 300/t increase w-o-w. Meanwhile, prices in western India remained steady at INR 30,000/t ex-Gandhidham, indicating a balanced supply-demand scenario.

Foundry-grade met coke prices also reflected positive momentum, rising INR 300/t w-o-w to INR 36,000/t ex-Rajkot, supported by increasing demand from end-users.

Optimism prevails in market

The market witnessed positive sentiment in eastern regions, with some participants expecting additional price strength in the coming weeks. Despite this, the western market stayed largely stable, with a balanced environment.

Meanwhile, the DGTR has issued preliminary findings in the anti-dumping probe on low-ash metallurgical (LAM) coke imports from Australia, China, Colombia, Indonesia, Japan, and Russia, confirming material injury to the domestic industry.

China’s met coke market holds steady as optimism softens

China’s met coke market remained steady after recent price hikes, supported by firm coking coal costs and cautious steel output. Mills largely operated near breakeven, focusing on controlled procurement and stable furnace operations, while suppliers noted limited room for near-term upside due to restrained downstream steel demand.

Indian coking coal market faces bullish sentiment amid market shifts

While the domestic met coke sector is poised for a recovery, its primary raw material — coking coal — faces a complex price outlook. Trader sentiment points towards a bullish short-to-medium term forecast.

The expected imposition of anti-dumping duties on met coke imports is creating a bullish sentiment among Indian manufacturers of the same. If imports of finished met coke become more expensive, domestic production is expected to ramp up.

This, in turn, will directly increase India’s demand for imported coking coal, as the country lacks sufficient domestic reserves of high-quality coking coal. This internal demand shock will compound the pressure from global markets. As one merchant trader involved in coking coal and met coke stated, there is an expectation that coking coal prices will rise from their current levels in the next few months.

Indian pig iron prices strengthen

Steel-grade pig iron prices strengthened, with Durgapur assessed at INR 32,600/t ex-works, up by INR 500/t w-o-w. SAIL’s Rourkela Steel Plant sold 2,500 t on 14 November 2025 at INR 32,150/t, marking an INR 450/t rise from its previous auction. Similarly, NMDC’s 17 November auction saw all 12,000 t booked at INR 30,000/t, pending final approval.

Outlook

The Indian metallurgical sector is at an inflection point. The DGTR’s intervention is set to revive the domestic met coke industry by shielding it from unfairly priced imports. However, this protection comes with a cost: a likely increase in the prices of its key raw material, coking coal, driven by both global factors and the very recovery of the domestic industry itself. In the coming months, the profitability of Indian met coke players will be a delicate balance between the newfound pricing power for their finished product and their ability to manage the rising cost of their primary input.

Leave a Reply